Ticker Reports for September 5th

Institutions Are Snapping Up These 2 Financial Stocks—Should You?

Individual investors are always looking for hints as to where stocks are heading next. Some use fundamental analysis to look for strong earnings growth, reasonable valuations, and manageable debt loads. Others use technical analysis to spot trend reversals or gauge the strength of momentum in a particular security.

However, it’s difficult for individual investors to perform fundamental and technical due diligence on an entire portfolio of stocks, let alone entire sectors or markets. Institutional investors, on the other hand, have vast resources for market research and the expertise to separate the signals from the noise.

That’s why many investors consider institutional buying and selling to be another form of research itself, as institutions are often ahead of analysts, financial media, and retail investors.

Recently, institutional investors have been eyeing a couple of particular finance stocks, which is notable considering the expected interest rate reductions coming later this year. Should you follow the “smart money” into these companies as well?

Institutional Investors Are Often Ahead of the Market Curve

If you can’t beat ‘em, join ‘em. It worked for Kevin Durant with the Golden State Warriors, and it can also work with retail investors and institutions. Now, you likely won’t be able to access their research, but you can track their positions and follow their lead when it comes to buying and selling stocks.

Institutional investors include hedge, mutual, pension, and other asset managers. These companies hire the best and brightest stock investors and provide them with sophisticated analysis tools and substantial capital to manage.

Because of these factors, institutions are viewed as the “smart money,” and when institutional money flows into a stock, it’s often a bullish signal for retail investors.

Institutional investment is a slow process. Unlike retail investors, institutional investors are not looking to profit from short-term price fluctuations by buying 100 shares. These companies often invest through large block trades and scale into positions over a period of weeks or months.

Scaling into large positions can be tedious, but it also pumps substantial liquidity into the market of a particular security. That’s why retail investors often play ‘follow the leader’ with institutions; not only do they use the most sophisticated and complete research methods, but they also provide price stability by injecting huge sums of capital into a stock's float.

Institutional investors can and do make mistakes, so tracking ‘smart money’ ownership isn’t an infallible strategy. However, when institutional ownership increases across the board, shrewd investors take notice.

Institutions Are Buying These Financial Stocks

Other than tech, the financial sector has been one of 2025’s biggest winners. However, the high-interest-rate environment is expected to end this year as the Federal Reserve begins easing. Why would institutions buy financial stocks with interest rate headwinds on the horizon?

These companies can navigate rate reductions without serious hits to their profits.

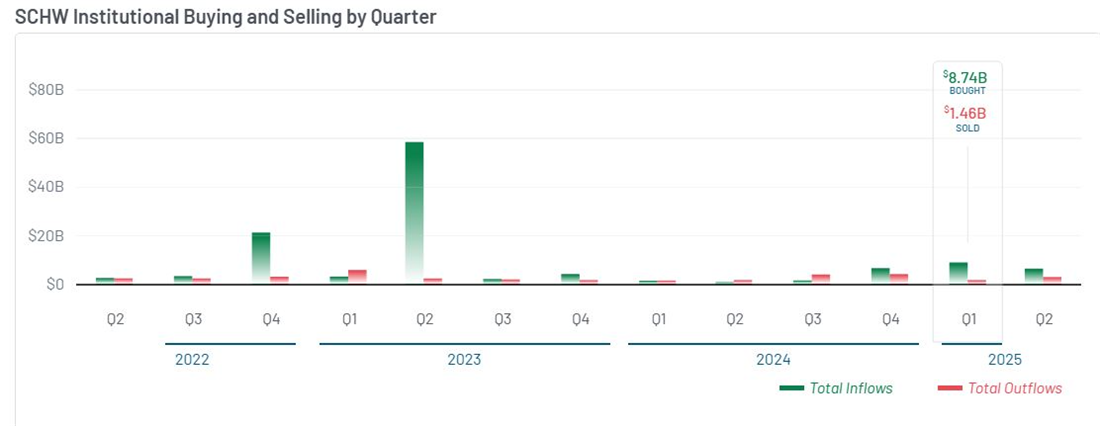

Charles Schwab: A Bet on Size and Stability

At this juncture, an investment in The Charles Schwab Corp. (NYSE: SCHW) is a bet that the firm’s asset management and trading desks will make up for any lost interest income from rate reductions.

Schwab has a massive client base, topping 37 million following the TD Ameritrade acquisition, and total client assets total well over $10 trillion.

The firm posted strong earnings numbers in Q1 and Q2 this year, and institutional buying is starting to pick up.

Institutions have bought more than $22.7 billion in SCHW shares over the last 12 months, compared to outflows of $12 billion. This buying frenzy has picked up substantially over the previous three quarters, including inflows of $8.7 billion in Q1.

Institutional investors are wagering that Schwab’s business model can withstand lower interest margins through trading and asset management fees boosts.

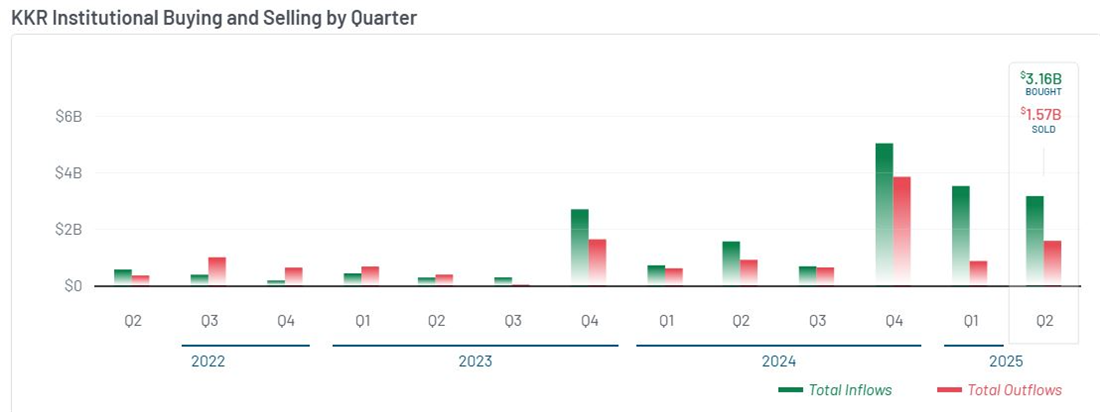

KKR: Public Exposure to Private Markets

KKR and Co. Inc. (NYSE: KKR) specializes in alternative asset management and was a major player in the 1980s leveraged buyout craze. The company’s focus is more diversified through private equity, private credit, real estate, and insurance.

However, its focus on private markets has intrigued institutional investors, thanks to soft markets in IPOs and M&A.

KKR has positioned itself as a leader in the private credit markets, providing liquidity to companies and investments that can’t access funding from traditional banks.

KKR recently raised more than $6.5 billion for a new private credit fund using an “asset-based finance” strategy, and continues to provide access to private markets for qualified investors through its hybrid private/public funds.

Private market returns are often uncorrelated to public markets, offering a hedge against traditional stock investments. Institutions are embracing this value proposition, as over $12 billion in institutional capital has flowed into KKR shares over the last 12 months, including $11 billion in the previous three quarters alone (versus $6.3 billion in outflows). In fact, institutions have put more capital in KKR in the last three quarters than in the previous three years combined; now that’s a bullish signal.

Buffett, Gates and Bezos Quietly Dumping Stocks—Here's Why

Buffett, Gates and Bezos Quietly Dumping Stocks—Here's Why

Salesforce Stumbles, But Investors Eye a Major Comeback

Salesforce’s (NYSE: CRM) Q3 and full-year revenue guidance were underwhelming, sparking a significant pullback in the share price that technology investors will want to take advantage of. Underwhelming is a relative term; in this case, it means that the guidance was as expected: sustained double-digit growth, margin strength, and robust cash flow drove its capital return.

The capital return is among the reasons why long-term tech investors will be interested, and the stock price outlook is strong. The bad news is that the underwhelming guidance and impact on analyst sentiment may keep the stock price under pressure until later in the year.

Salesforce pays a token dividend that annualizes to less than 0.7% with the stock trading near long-term lows. The more significant portion of the return is share buybacks, which amount to more than five times as much on a dollar basis.

The critical takeaways from Q2 are that the buybacks reduced the count by more than 1.1% on average for the quarter and 1.35% year-to-date, and they are expected to continue at a similar pace—if not increase—in the near future. The company’s growth outlook, cash flow, and new board authorization worth $20 billion may increase that pace. The latter lifted the remaining allotment to $50 billion, sufficient to sustain the Q2 rate for the next five years.

Salesforce Q2 Strength Overshadowed by Cautious Guidance

Salesforce had a solid quarter in Q2 with revenue growing by 9.8% as reported and 9% on a constant currency basis (CC). The top-line exceeded MarketBeat’s reported consensus by approximately 100 basis points, with strength seen in Data Cloud and AI segments. Subscriptions and Support, the primary category, grew by 11% and 9% CC, while Data Cloud and AI, the growth pillars, advanced by 120%.

Margin is another area of strength that investors should focus on. The company is growing profitably and widening its gross and operating margins. The net result is a 30 basis point increase in net income to 18% of revenue and outperformance on the bottom line.

The adjusted EPS of $2.91 is more than a dime above forecasts, and strength is expected to continue through the year’s end. Although the revenue guidance was tepid, coming in as expected, the earnings guidance was improved to a range above consensus, with strength anticipated in Q4.

Among the critical details is a forecast for 12% free cash flow growth at the midpoint of the target range.

Salesforce’s balance sheet underscores the business strength and reliability of the capital return. At the end of Q2, the highlights include fortress-quality leverage ratios, a net cash position relative to long-term debt, and rising equity despite the aggressive buybacks.

Equity is up incrementally, while treasury shares increased by 25% to over $24 billion.

Salesforce Analysts Trim Targets: Range Narrows Around the Consensus

Salesforce analyst are lowering their price targets following the Q2 release and guidance update, but don’t read too much into the movements. The reductions narrow the range around the consensus price target, which forecasts a 35% upside from critical support targets.

Likewise, the institutional activity is robust this year and suggests solid support near September trading levels and the low-end of the analysts' target range.

CRM’s price action pulled back following the update, but is unlikely to extend the move this month. The stock price is near the low end of the analysts' target range and support targets that have been confirmed numerous times, setting this market up to rebound.

The most significant risk is that CRM’s stock price will wallow near current levels indefinitely. However, that is not expected due to the growth and capital return outlook. The question is how long the stock will linger near its lows before analyst sentiment is reinvigorated and the rebound begins.

The most likely catalyst is the Q3 earnings results, which aren’t due until early December.

Newegg (NEGG) Earns BULLISH Rating – Up 934%

Newegg (NEGG) Earns BULLISH Rating – Up 934%

Lockheed Martin: Is the Market Overlooking This Defensive Giant?

For investors tracking Lockheed Martin (NYSE: LMT), the past year has been a test of patience.

The stock has underperformed the broader market, creating a disconnect between the defense sector giant’s strategic importance and its recent market performance. The most recent catalyst for this downward pressure was the company's second-quarter 2025 earnings report, released in late July, which revealed $1.6 billion in pre-tax losses associated with a handful of complex programs. This led management to cut its full-year earnings-per-share (EPS) forecast, raising questions and doubts among investors.

However, sentiment around the stock is actively shifting. And in the current environment, Lockheed presents a critical question: Does this short-term operational turbulence signal a fundamental flaw, or does it signal a compelling entry point for investors focused on long-term value?

Lockheed’s Twin Engines of Long-Term Value

The long-term bull case for Lockheed Martin is built on two interconnected pillars: a nearly impenetrable strategic moat and the massive financial backlog that results from it. For Lockheed, this advantage comes from a portfolio of high-tech, mission-critical systems that, due to immense research costs and decades-long development cycles, are exceptionally difficult for competitors to replicate.

This moat is evident across its business segments, which translate directly into massive revenue streams. In its aeronautics division, which posted $7.4 billion in sales in the second quarter of 2025, the F-35 Lightning II is the undisputed cornerstone of 5th-generation air power for the United States and more than a dozen of its allies.

Meanwhile, the Missiles and Fire Control segment saw sales grow an impressive 11% year-over-year, driven by high demand for tactical weapons like the Patriot Advanced Capability-3 (PAC-3) and HIMARS rocket systems. These are not discretionary purchases for governments; they are essential tools for national security.

This strategic importance translates directly into financial stability through the company’s immense order backlog. As of the second quarter of 2025, Lockheed Martin reported a total backlog of $166.5 billion. This figure represents the total value of all signed and funded contracts for future work.

For investors, this multi-year order book provides exceptional visibility into future revenue, making financial forecasting more reliable and accurate. This high degree of predictability helps insulate the company from the volatility of short-term economic cycles, a key characteristic of a top-tier defensive stock.

Shareholder Returns and Cash Generation Remain a Focus

No investment is without risk, and investors must consider the significant headwinds that the company has recently faced. The $1.6 billion charge taken in the second quarter is a material event, and the subsequent reduction in the full-year EPS guidance to a range of $21.70 - $22.00 reflects a real impact on profitability. However, the company's underlying financial health appears to be strong, particularly in terms of its ability to generate cash.

In a move that should provide confidence to long-term investors, management reaffirmed its robust 2025 free cash flow guidance of $6.6 billion to $6.8 billion. Free cash flow is a critical metric because it represents the cash a company generates after accounting for the capital expenditures needed to maintain its operations. It is the lifeblood that funds growth and, most importantly for many investors, direct returns to shareholders.

The company has a long and consistent history of rewarding its investors. Lockheed Martin’s dividend profile is a key part of the investment thesis, offering a current yield of approximately 2.94%. Critically, that dividend has been increased for 22 consecutive years. While its dividend represents about 74% of its earnings (a figure that might seem high), it accounts for a more sustainable 38% of its cash flow, indicating a healthy capacity to continue making payments.

This is supplemented by a substantial share repurchase program. In the second quarter alone, the company returned $1.3 billion to shareholders. These buybacks have a tangible effect, reducing the number of weighted average diluted shares outstanding from 239.6 million in Q2 2024 to 234.3 million in Q2 2025. Fewer shares on the market means that future profits are divided among a smaller number of owners, which tends to increase earnings per share over time.

This combination of headwinds and strong cash generation has created what appears to be an attractive valuation. The consensus 12-month price target from Lockheed Martin’s analyst community stands at $494.00, suggesting meaningful 10% upside from its current trading level.

Lockheed Martin’s Position of Enduring Strength

While near-term headlines have created stock price volatility, a deeper look reveals a company with its fundamental strengths firmly intact. The powerful combination of a strategically essential product line, a predictable multi-billion-dollar backlog, and a steadfast commitment to shareholder returns through dividends and buybacks solidifies Lockheed Martin's status as a core holding for any long-term, defense-oriented portfolio.

Warren Buffett Issues Cryptic Warning on U.S. Dollar

Warren Buffett Issues Cryptic Warning on U.S. Dollar

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

No comments:

Post a Comment