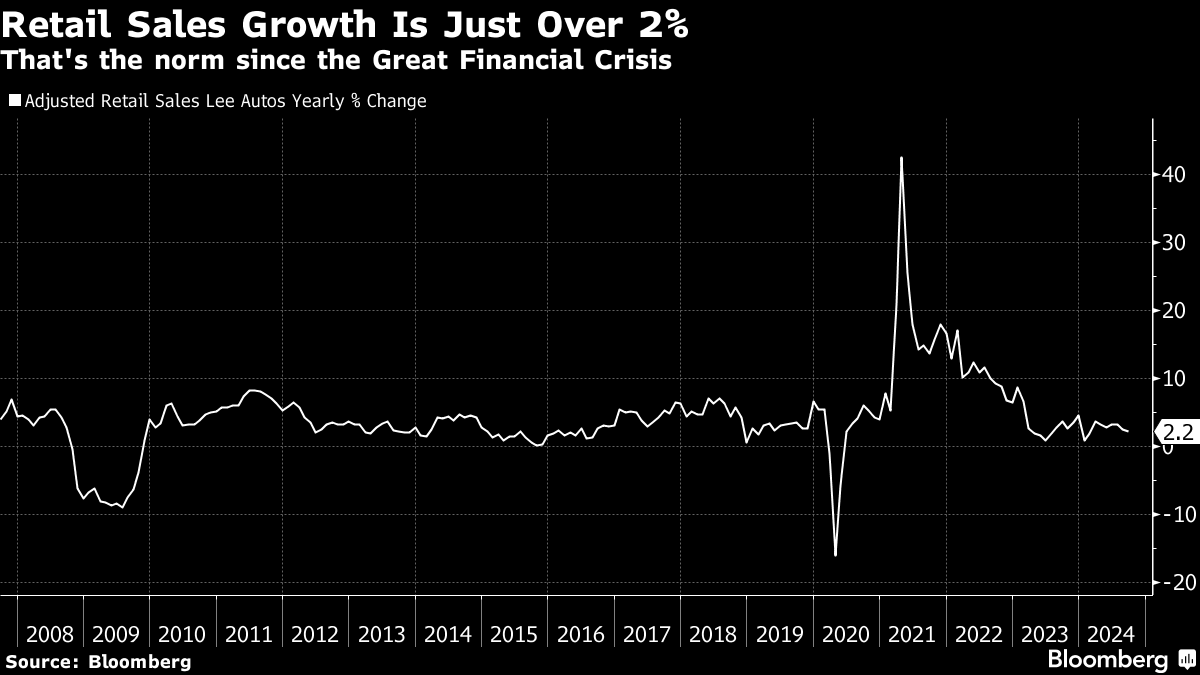

| What about households? The beginning paragraph in this recent Bloomberg article says everything: US households' inflation-adjusted incomes rose last year for the first time since 2019, yet they still have not fully recovered to pre-pandemic levels.

And remember, this is in a world in which the stock market is at new highs, interest income is through the roof for people with savings and house prices are going up. It tells you that, while some people have benefited from those trends, the average household is only just getting back to normal. Let me show you why the composite no-landing picture obscures this inequality using General Motors as an example of how this plays out in corporate earnings. Here's a summation of the Bloomberg reporting on their recent quarterly profit: General Motors signaled solid US demand for its highest-margin vehicles even as the broader market softens, posting better-than-expected results for the latest quarter and raising the low end of its full-year profit forecast

Translation: even though the broader market for GM's cars is pretty soft, the high-end stuff is doing so well that GM was able to post better-than-expected profits and raise guidance on future profits. If you break down why this is happening, it's because lower-income households are being squeezed. The official inflation numbers aren't going to tell you that. "Property taxes, tips and interest charges from credit cards to auto loans aren't factored into the Bureau of Labor Statistics' consumer price index." So the higher auto-loan and credit-card payments due to the Fed's rate policy are not factored into inflation statistics. And these are costs borne disproportionately by lower-income households. Fewer high-income households carry a credit balance from month to month or have a car loan. Instead, they are more likely to benefit from higher rates through interest income, having locked in a low fixed-rate mortgage before the pandemic ended. In short, it's getting harder to break into the middle class for a bunch of reasons that higher interest rates have exacerbated. That explains the discontent in the US electorate as much as partisanship or even inflation. But because the upper middle class and the wealthy have generally locked in their debt costs, they have been insulated from higher rates, making the US economy as a whole also more insulated against those higher rates. The GM earnings results are representative of what you'll find across corporate America. With the upper quintiles who represent a disproportionate share of consumption continuing to spend, corporate earnings should continue to do well. With the big tech companies yet to report, we have seen a better-than-expected earnings season so far. And corporate guidance remains upbeat as well. The fact that this economic resilience has surprised analysts, who have low-balled their expectations, only adds to further upside gains for large-cap shares. Upside economic data surprises have been outstripping negative ones for three months now. The Atlanta Fed's GDPNow tracker even says we could have 3.4% growth for the quarter just ended, higher than in the three months ended in June. In bond land, it's a different story. Corporate bonds benefit from the economy just like stocks. But Treasury yields are increasing. Two weeks ago, I wrote to investors on the Bloomberg Terminal that "market pricing is predicated on Fed rate cuts that are designed to remove policy restrictiveness by reducing real interest rates. But to the degree that inflation proves sticky, those cuts will not be forthcoming, rate volatility will continue and the whole curve will move above 4%." Two weeks later, we've arrived there, with the three-year US note, the lowest-yielding maturity over 4% on Wednesday. A couple of weeks ago, I wrote another piece on the Terminal about the combination of the good corporate earnings and a no-landing scenario as generally positive for investors, especially given that the downside risk for Treasuries was limited by future Fed rate cuts. And while the positive scenario for equities remains in place, the downside risk for Treasuries has increased. Ten-year Treasury yields, having just surpassed the 200-day moving average on Tuesday, are now vulnerable to re-testing year-to-date highs close to 4.70%. A no-landing scenario, coupled with a rise in inflation and larger than expected deficits (say from a re-upping of the Trump tax cuts) would draw an offsetting reaction from the Fed. This would prevent the central bank from cutting its policy rate to 3% and potentially cause it to pause cutting indefinitely. After the US presidential election and inauguration, the fiscal picture will become clearer, as will the potential for no landing and higher inflation for longer. Until then, 4.70% certainly remains a target. And that is just one inflation shock away from 5%. The enduring contours of the post-pandemic US economy are still not clear. Data that normally point to recession — like an inverted yield curve or rising unemployment — have sent false signals time and again. There's therefore an increased probability of sustained high growth, underpinning corporate earnings and equities. It also indicates a greater chance of inflation reviving, spurring future rate-cut pauses by the Fed, hurting Treasury investors. A budget-busting tax-cut package will only make this divergent outcome for stocks and bonds all the more extreme. |

No comments:

Post a Comment