| It's been a while. I went on vacation last week, having just penned a piece about Nvidia's vertiginous rise and how it demonstrates we've hit mania territory. As it happens, Nvidia sold off by more than 20% just after that. So I got the timing right. But what comes next? There are so many unknowns — from the US Presidential race to the Fed's tightening to the softening of the US economy to Iran talking about backing Hezbollah in a war with Israel. So let's walk through three issues that I think will most define the coming six months for markets. I'll start with the market mood, beginning with Nvidia and then we can discuss the economy and the Fed's reaction to it, followed by the US election. The US stock market has consistently outperformed for years. And global investors are still pouring money into stock markets. That combination says that it almost doesn't matter what happens to the US economy. There is still an upward bias to US share prices because of money inflows. So, while Nvidia has seen a sharp correction in its share price since I wrote negatively about it two weeks ago, there is nothing that leaps out suggesting this is anything other than a reduction in the riskiest bets. In some ways, it's almost heartening to see Nvidia's recent price action because it takes the edge off enough to prevent a full-fledged bubble. It could also presage selling pressure for the US market overall, too, despite the current bullish tone. Bloomberg Intelligence Strategists Gina Martin Adams and Gillian Wolff recently wrote that "global stocks setting new all-time highs are flashing some more warning signals: the lack of breadth and correlation risk. Less than half of the major markets rose as the share of stocks trading above their 200-day moving average fell in June." They further note that earnings revisions are ticking up everywhere except in the US, as a slowing American economy passes the growth baton to other countries. So I would continue to characterize this as a market that is "drifting" as we await fall fireworks, but with a slight upward bias. Following from above, here are two signposts that represent both the current bullish bias and the vulnerability of a US stock market that lacks breadth. The first is Tesla. The stock was up more than 10% on Tuesday and the Bloomberg headline was "Tesla Beats Estimates With Less-Drastic Drop in EV Sales." That headline perfectly encapsulates the situation: namely, that Tesla's sales are falling, not rising, even if they fell less than expected. And the stock is up 10% on the news of a less-severe decline? That's one heck of a relief rally. Which gets me to the news of JPMorgan strategist Marko Kolanovic leaving the firm and "exploring other opportunities" after 19 years there. This paragraph sums up why his departure is significant: The move comes following a disastrous two-year stretch of stock-market calls by Kolanovic. He was steadfastly bullish in much of 2022 as the S&P 500 Index sank 19% and strategists across Wall Street lowered their expectations for equities. Then he turned bearish just as the market bottomed, missing last year's 24% surge in the S&P 500 as well as the 14% gain in the first half of this year.

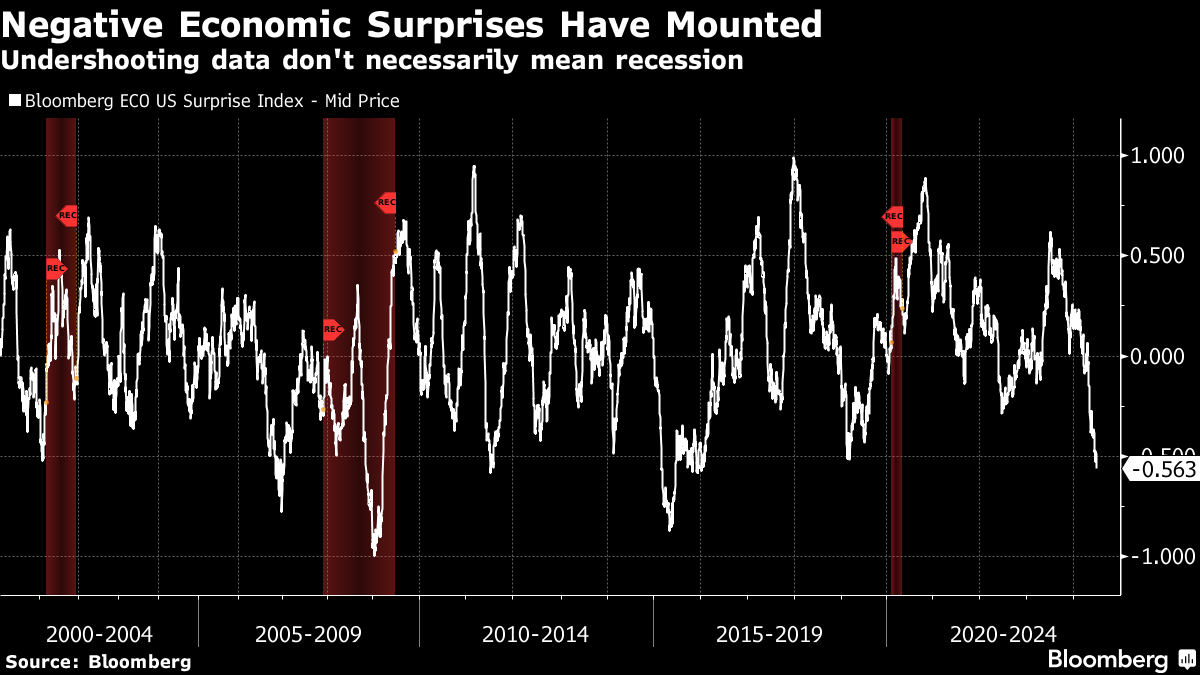

So, here's a guy who was bullish, remained so for too long and switched to bearish at just the wrong time. And so after nearly two decades of fine work, he leaves his firm, remembered for being wrong, "the last bear on Wall Street." That sounds a lot like a contrarian indicator to me — "peak bullishness," if you will. There's literally no one left at the major Wall Street firms who is bearish on stocks. Everyone is bullish now. That makes me very uncomfortable. Along with Tesla's relief rally on declining sales, the fact that everyone is bullish speaks both to the bullish bias of the overall market and the vulnerability of that market to the decelerating US economy. In terms of the direction of the economy, I have long felt that the weekly US jobless claims figures are some of the best real-time data points. Not only do they come out every week, giving us a high-frequency and real-time gauge of the labor market's health, they have also been very prescient in helping identify recessions and recoveries. The fact that continuing claims are at a three-year high suggests that the labor market is slowing, perhaps enough to warrant a cautionary rate cut from the Federal Reserve in September. Priya Misra at JP Morgan Asset Management thinks comments from Fed Chair Jerome Powell show the US central bank is getting worried. But the Fed is keeping its options open. So a September cut isn't fully priced in. If you look at what's been expected versus what has been delivered by the US economy over the past few months, this is the worst underperformance in almost a decade. Only once in the last 25-odd years, during the shale-oil bust a decade ago, have we seen the data undershoot expectations this much without a recession. So we are getting to a point that if the data continue to come in lower than expected, it would warrant a rate cut. Still, the Fed, burned by near double-digit inflation after the US economy re-opened, has had more hawkish rhetoric than I would have anticipated. The combination of a market lacking breadth and peak bullishness are, therefore, potentially on a collision course with a hawkish Fed dismissing the very stark and visible signs of a slowing US economy. |

No comments:

Post a Comment