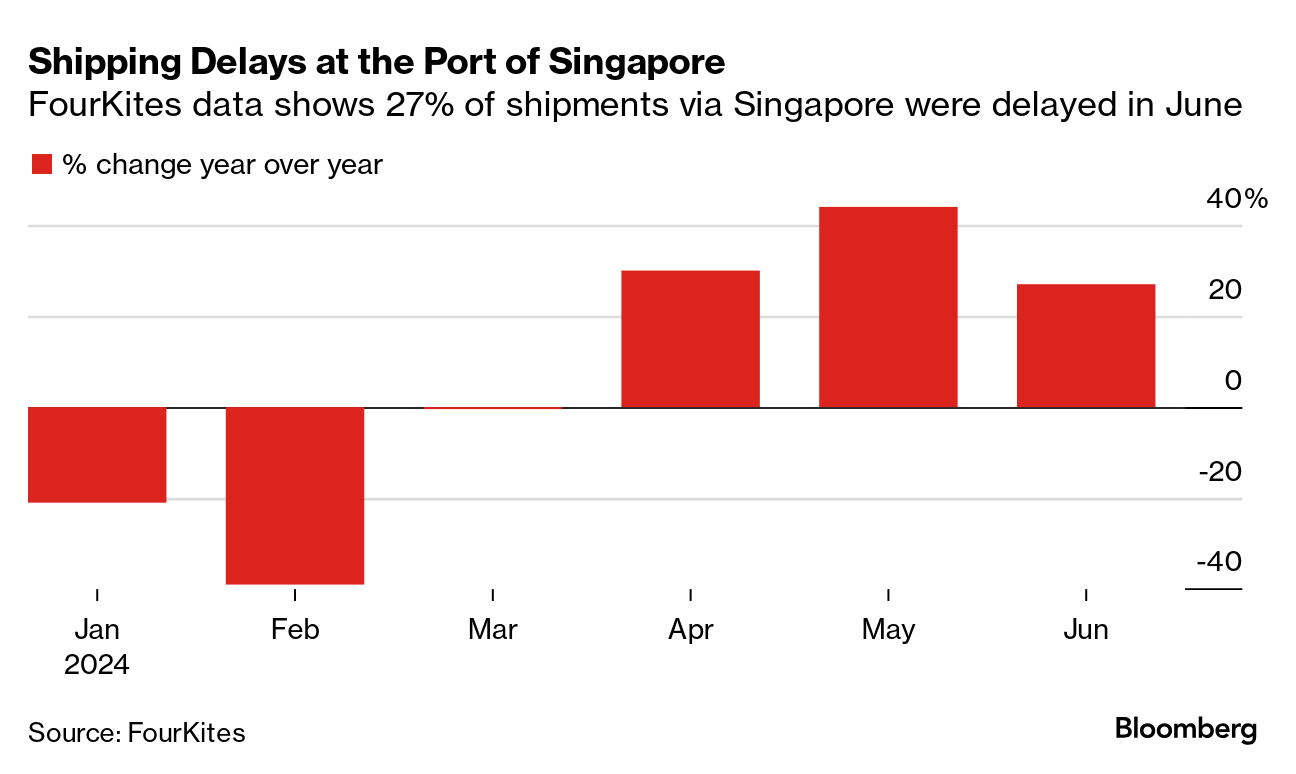

| Container shipping and the web of global transport services linked to it are entering the usual peak season for demand, but the scenario planning this year includes just as many questions about supply. Red Sea vessel diversions and port congestion have absorbed whatever excess capacity the industry offered at the end of 2023, when the Houthi attacks intensified regular occurrences. Spot container rates have doubled since early May. In Singapore, home of the world's second-busiest port and a key transfer hub for cargo between Asia and the West, delayed shipments jumped 44% in May from a year earlier, and through June 25th were up 27% year-over-year, according to data from FourKites, a supply chain visibility platform. "The lack of available empty shipping containers in key export markets is an ongoing concern," said Mike DeAngelis, head of international ocean solutions at FourKites. "Containers are getting caught up in a global mix of delays." Adding to the bottlenecks is a demand reflex honed during the pandemic: the fear of missing out. Looming US tariffs on Chinese imports and a possible late-summer strike at East and Gulf coast ports are boosting orders sooner than usual. Read More: Global Sea Transport Leaps Most Since 2010 After Red Sea Attacks Judah Levine, head of research at cargo-booking platform Freightos, says it would be wise to plan for another couple of months of strains. He says spot container rates to Europe and the US from Asia might reach $10,000 per 40-foot equivalent unit in the months ahead from their current level of $7,000 to $8,000. It will take a confluence of other disruptive worst-case factors for rates to return to pandemic highs of $15,000 to $20,000, but it's not impossible, he said. Bloomberg Trade Tracker: Revival Gathers Speed Except in Europe "To me, the most likely scenario is that we're going to see a couple months where there's a lot of pressure," Levine said. "We may even get to those levels of $15,000 per container, but over the pandemic we had months and months of that. This time I think we could have some months but not many." Three Scenarios Here's a rundown of Levine's scenarios for the second half of the year: - Worst Case: Under this scenario, ships continue avoiding the Red Sea, the early peak-season demand stays solid and port congestion lingers for months — extending the global disruptions past Chinese Lunar New Year starting in late-January. Add on top of that a strike by dockworkers on the US East and Gulf coast and container rates would reach the record highs set during the pandemic.

- Best Case: This scenario hinges on an end to Houthi attacks in the Red Sea, which would allow carriers to return to their optimal sailing schedules. After a few months of adjustments, cargo rates would drop sharply as supply outpaces demand. Newly built ships coming into service would help push the cost for a 40-foot container back to pre-pandemic levels around $1,000 between Asia and the US and Europe.

- Most Likely Case: For this to play out, the current strength in demand softens, indicating that early orders were pulled forward from the third and fourth quarters because of either looming US tariffs on Chinese imports, Red Sea delays, port strike worries — or a mix of all three. Spot rates still might peak around $10,000 per 40-foot container this month and next, but they would come back down later in the year.

—Brendan Murray in London Click here for more of Bloomberg.com's most-read stories about trade, supply chains and shipping. |

No comments:

Post a Comment