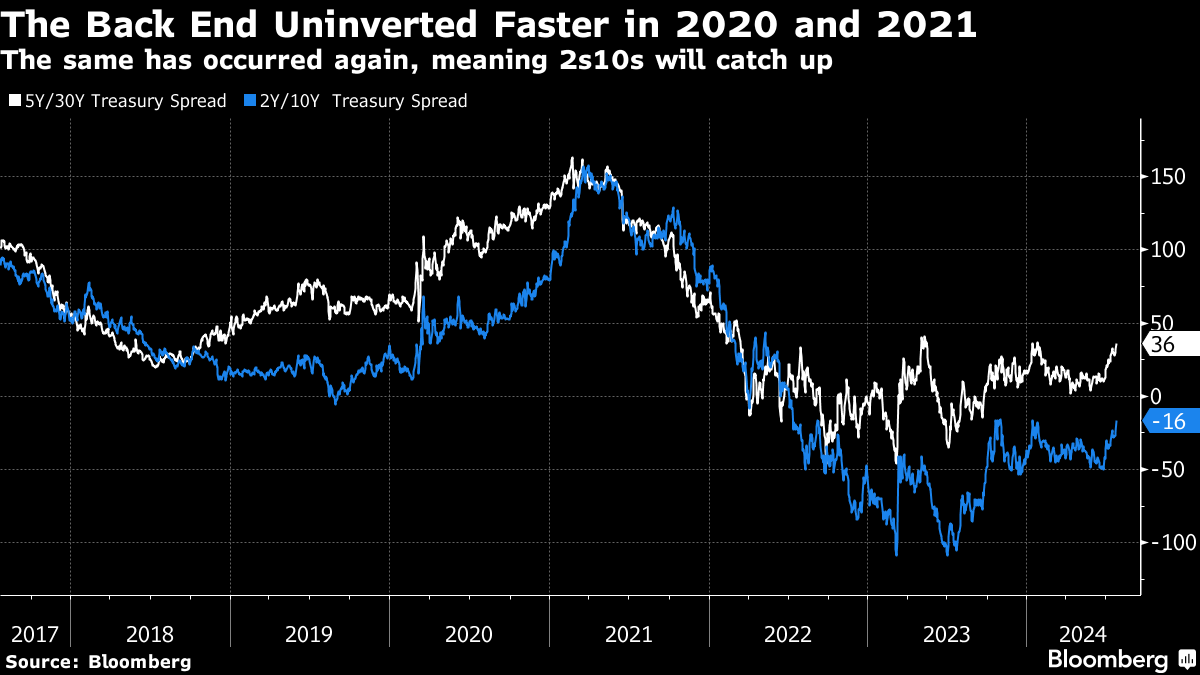

| I don't think equities get hit yet. How robust they are will tell us how close we are to recession, though, as weakening profit growth would presage job cuts. And so far, this quarter is just fine. We have a long way to go in reports but the financial sector is a good bellwether here. Sector leader JPMorgan Chase, for example, saw revenue up 20% in Q2. "JPMorgan earned $18.1 billion in net income in the second quarter, up 25% from the previous record a year earlier and ahead of analysts' expectations." Investment banking fees were up 46% and equity trading was up 21%, signs of a return of M&A and of potentially more equity market optimism to come. Arguably Charles Schwab's result show us why the Fed needs to cut, though. The company is promising to shrink its banking operation. As I detailed with colleague Annie Massa in the Spring of 2023 — when the regional bank crisis was hot and heavy — Schwab is the poster child for the strategy of loading up on long-term safe assets that got the regional banks in trouble. The issue is two-fold. One, Schwab has a ton of low-yielding assets on its books that are worth a lot less after the Fed jacked up interest rates. Treasuries and mortgage-backed securities sporting pandemic-era yields aren't worth nearly as much in a world where the upper bound of the fed funds rate is 5.5%. And you can't get these assets off your books either, because selling them would crystallize loses. That's exactly what caused the panic over a year ago after Silicon Valley Bank sold some of its dud assets. That means you have to accept lower income for months and years to come. The second problem is on the liability side of the balance sheet. Schwab gets a lot more money from net interest income in this zero-commission world than you might think. That's because the brokerage business model depends a lot more on management fees and the "free interest income" on idle cash after commissions went to zero. Every dollar in your brokerage account that's not invested, and sitting around as cash, is money that the broker can use to invest. It's much the way banks take the money in your savings account to invest and earn a spread between what they give you on your savings and what their investments earn. The income they earn, usually from bonds and other fixed-income products, is a lot greater than what you're asking from them in interest. Trouble is, getting pennies in interest is only fine when the fed funds rate is zero. It's not so great when fed funds is 5.5%. So people have been either yanking their funds or demanding higher interest products from regional banks (and Schwab). And that's even while a huge portion of those institutions' assets are earning low pandemic-era returns. Schwab's earnings report showed us this problem is persistent, and perhaps intensifying. The stock plummeted after it reported. In conjunction with the rising unemployment rate and the squeeze on private markets, this is why the Fed should be thinking about cuts. How would I wrap this big picture up into a conclusion then? I'd start with the quarterly earnings reports first. They're good enough so far. JPMorgan Chase and Alphabet are decent proxies for how well the best companies are performing. At the same time, the Schwab miss tells you we should be worried not just about economic deceleration, but also about the negative impact on the health of US financial institutions. Tesla is a second kind of bellwether in all this. It's the weakest of the Manificent Seven stocks in my view. Here's a company whose business model has taken on water since the beginning of 2023. And while we were led to believe that it had weathered the downturn in electric vehicle adoption growth because of massive discounting, we now see that Tesla's reprieve was an artifact of the bullish market mindset that the boom in artificial intelligence seeded. Tesla's revenue is actually declining now, not growing. But the stock still has a trailing price-earnings ratio of 100 times — as if it will reassert massive growth in due course. So even though the stock is down more 10% on the day after earnings alone, it's well off of 2024 lows, suggesting the bullish upward market isn't over quite yet. So look at the recent US equity market pullback as indicative of a market biased to the upside that had run too far too fast. We're still in what I've called a summer "drift" phase, but with a slight upward bias. That leaves bonds as the asset class to watch. About two weeks ago, in a piece geared toward bond market professionals, I wrote that the curve steepener, where long-term bonds underperform their short-dated counterparts, was the trade to watch. My exact words were: Treasuries in the one- to two-year space should rally most, while longer-term bonds will remain anchored by large supply from deficit spending and an increasing term premium. The faster the rate cuts come, the more aggressively 2s10s should play catch-up. Right now, we're working with a 2s10s curve that is almost 60 extra basis points flatter than the 5s30s. In pretty much all scenarios, we should expect that gap to close.

Let me break that down a little further for those of you who aren't bond traders. As I've been saying, the Mosler argument about deficits suggests more inflation, some offset in more hawkish policy from the Fed, and thus higher long-term interest rates. We've seen that play out to the point now where at the very longest maturity end of the spectrum, 30-year Treasuries are close to yielding the most relative to 5-year bonds since the Fed started hiking. I'd say then that this move is mostly done. It's the difference between the interest-sensitive 2-year and the whole curve's benchmark, the 10-year, that will now play catch up. When I wrote the piece two weeks ago, the 2s10s, the difference in the 2-year yield and the 10-year, was almost -30 bps - meaning you were paying the Federal government less to take on interest rate and inflation risk for 10 years than 2. That gap is now under 20. And I think it will close entirely soon. If we avoid a recession — which seems likely to me at this juncture — then it will be a so-called bear steepening that gets us to "uninvert" the curve, as people finally believe in this recovery and ask to be compensated for taking on the risk of holding long-term debt as deficits balloon. But even if the economy falls into a recession, those long-term yields will be held higher by the deficits and inflation they bring, also making two-year notes more attractive when the Fed cuts to alleviate the pain. We won't know which way the economy goes definitively until the fall. I don't think the Fed cuts next week. I think they cut in September. And between then and the October earnings, we'll know where the economy is by election time in November. Given the bump in polls after President Joe Biden dropped out and the likely bump to come from a vice presidential pick and the Democratic Convention, this race is going to be wide open. Whether the economy holds up will, therefore, be hugely important politically and for markets. But wait until October to give the election any consideration. Until then it's all about the economy. |

No comments:

Post a Comment