| Now, let's turn to equities. Nvidia won't report for a few weeks but I am expecting big things. The logic I outlined three months ago still holds: Everyone and his sister is pouring money into artificial intelligence. Any company that's leveraged to that space has a tailwind on growth for quarters to come. And we need look no further than Amazon to see this. Amazon Web Services (AWS), which is the Amazon business most leveraged to AI, beat on the top line and had the largest profit margin, nearly 40%. That's an insane margin for any business. And since both margin and revenue are growing, earnings from AWS are growing even faster. Contrast this to Meta Platforms, which gets the bulk of its revenue from ads on Facebook and Instagram. There the company beat estimates but shares tumbled. Why? This quote sums it up: "The disappointment on the revenue side is overshadowing any optimism about AI," said Jack Ablin, chief investment officer at Cresset Wealth Advisors. "It's hard to tell what the benefit will be to users, and while AI could ultimately mean some cost savings down the line, that isn't visible yet."

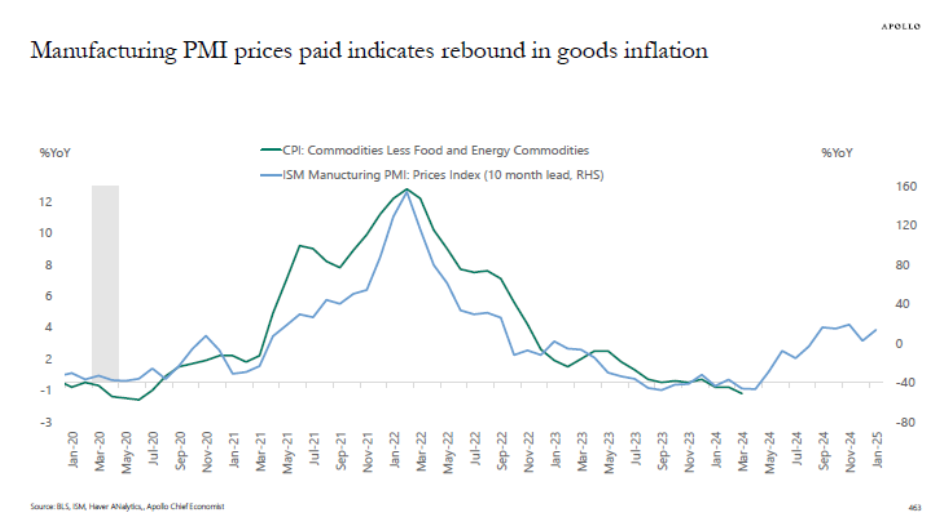

Meta beat the street because of "old school" revenue, not from AI. So I guess it's a has-been? That's the message from investors at least. For companies, it underscores how much AI is driving the current rally and incentivizes them to make proper investments in the technology, lest they receive the treatment Facebook co-founder Mark Zuckerberg did. This, of course, only helps propel companies like Amazon or Nvidia, which are genuinely leveraged to AI, to new heights. With a lot of Big Tech and banks having reported, the sense I get is that the engines of growth from innovation and credit are still intact enough to maintain the bull market. With yields going up, future cash flows are worth less in today's dollars. But the prospect for those cash flows to be greater more than overrides that impact, at least for the companies with future-oriented earnings reports. This is why stocks overall actually do well in an environment in which yields are increasing, especially high-beta companies with backloaded earnings profiles. What's the wrinkle? It's two-fold. First, there's the high rates piece. And then there's the related but separate issue of consumer fatigue. On rates, I've been an advocate of the sometimes-derided view that higher rates can be stimulative. The case is pretty simple really. If monetary policy is to be restrictive by making borrowing more onerous, then the more onerous borrowing by debtors has to override the more favorable interest income from savers and lenders. And in an environment where the Congressional Budget Office says "the deficit amounts to 5.6% in 2024, grows to 6.1% in 2025," you're not going to see that. There is simply too large a net transfer of financial assets to the private sector from the federal deficit to think borrower pain will outweigh creditor joy. Even so, debtor distress is real. For example, the percentage of credit-card bills past due in Q4 2023 was already higher than at any point since 2012. In the last GDP report, the imputed personal savings rate was just 3.2%. These are telltale signs of simmering financial stress. At some point, without rate relief, this will spill over into consumer fatigue and act as a brake on growth. Given the huge pick-me-up from federal deficits, the question is when. But since we're talking about consumer fatigue emanating from debt interest payments, we should also discuss the pernicious impact of resurgent inflation too. The headline of Wednesday morning's ISM Manufacturing Survey was the sluggishness revealed by only 49.2% of businesses reporting growth. The highlight, however, was the nearly 61% of businesses reporting higher prices paid. Recent commentary from Apollo Global Management's Torsten Slok suggests we could see goods inflation re-accelerate, adding to a sticky services inflation that will stretch the paycheck of average wage earners even further. That is inflation that will feed through to consumers to act as a second source of stress on family budgets. The US economy is still growing above trend but with cracks that can't be ignored. We're still in a no-landing world that demands the indefinite hold strategy the Fed is now delivering. In fact, the central bank's forward guidance since December probably contributed to some of the loosening of financial conditions and overheating we've now seen. So, the Fed's latest guidance will help the economy find a level more consistent with slower inflation, and is a much-needed course adjustment. Overall, that's a decent backdrop for bonds and equities. Recent firming in data out of Europe only add to the upside prospect for companies with global ambitions. On the bond side, it's the fact that inflation would need to go to 4% or 5% before we got hikes that limit downside risk. With the fed funds rate at 5.33%, that means 5.25% is a likely hard upper bound across the curve. The closer we get to 5% at the back end of the curve, the more incentive investors will have to lock in yield — a major reason we haven't seen long rates catch up to shorter-term ones yet. On the equities side, as long as the economy keeps going, we should expect companies with the most backloaded earnings prospects to continue to lead the charge. Those that falter because of poor execution or a lack of earnings leveraged to future trends will be punished ruthlessly by investors. But I would caution that this is exactly the scenario that will mean a heavy sector performance rotation when a recession hits. When everyone has piled into growth as far as the eye can see and the economy turns down, the whiplash will be extraordinary. Sorry to end my upbeat views on a sour note about sector rotation whiplash. But the reality is that risk-taking has become severe. So, quick question here. Short-dated options are presented as a tool to hedge or speculate on event risks, such as this week's Fed decision, though some are worried about their side effects. What's your opinion of ODTE? Would you support expanding their use to individual shares to allow traders to make more targeted bets on developments such as corporate earnings? Share your views in Bloomberg's MLIV Pulse survey. |

No comments:

Post a Comment