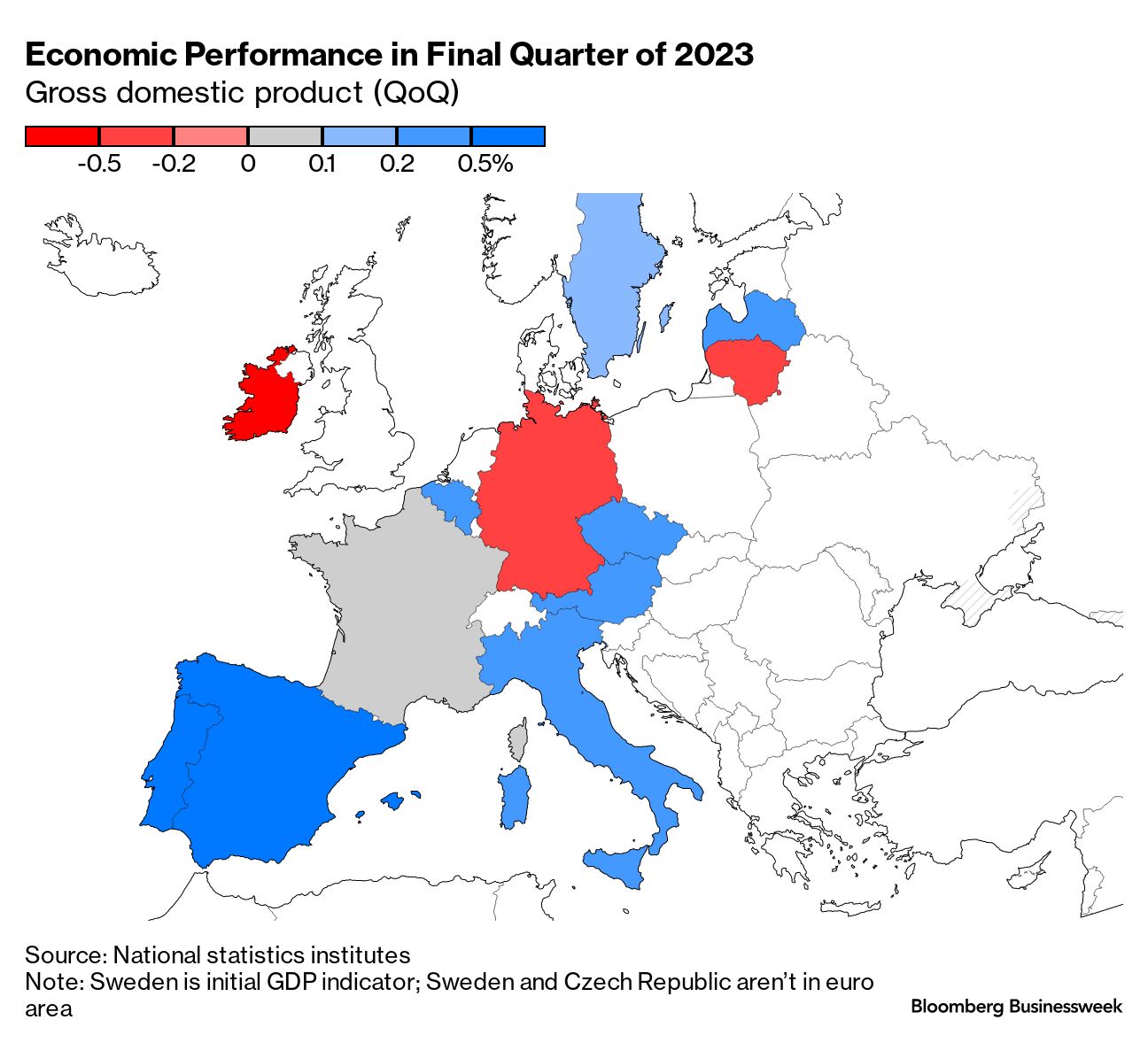

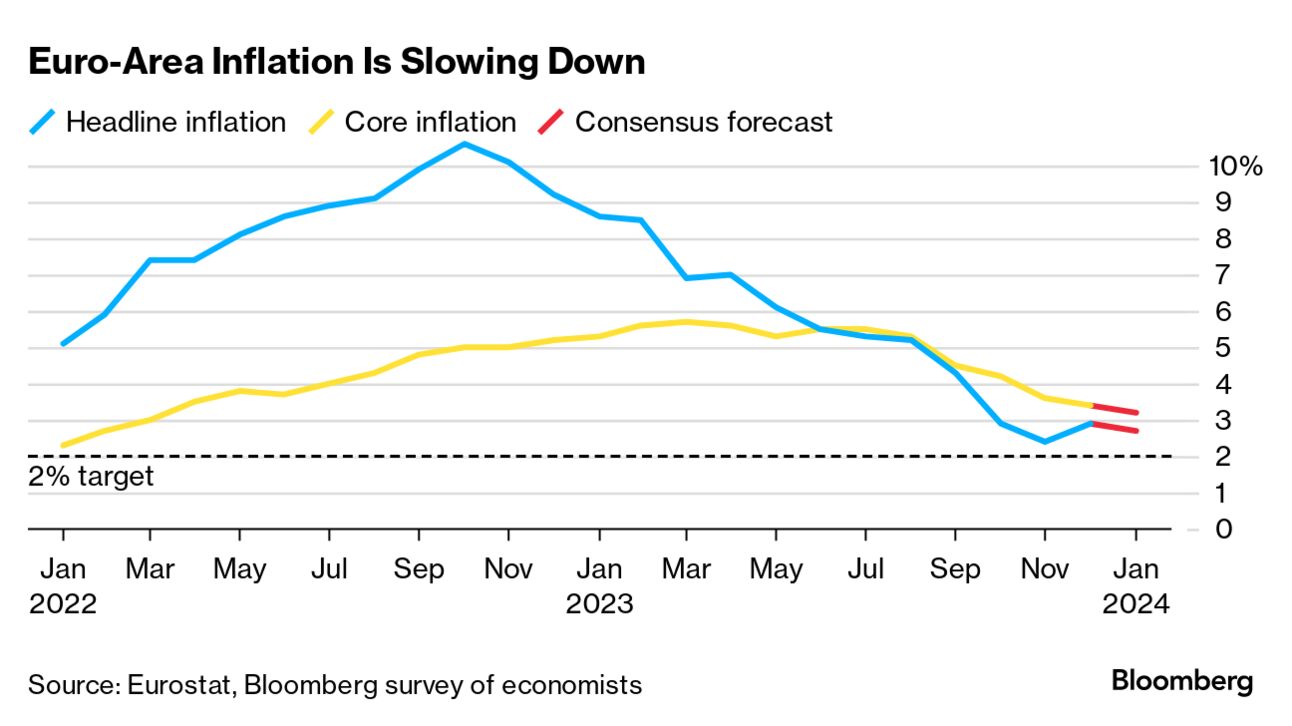

| I'm Craig Stirling, a senior editor in Frankfurt. Today we're looking at whether the Federal Reserve or the European Central Bank will cut interest rates first. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X via @economics. And if you aren't yet signed up to receive this newsletter, you can do so here. By the end of this week, the Federal Reserve will have delivered its first interest-rate decision of the year, and a raft of data will have cast light on the US jobs market and the euro-zone economy. That flurry of news may well allow investors to make a firmer call on the timing of US monetary policy easing — with some already betting on a reduction as soon as March, and others wagering on May. Along with that, they can also take a view on whether officials in Washington or Frankfurt will move first. "A lot hinges" on whether the Fed or European Central Bank makes the initial cut, "as far as the volatility we've seen in rates markets," according to Ray Attrill, head of FX strategy at National Australia Bank Ltd. Euro-region gross domestic product numbers out on Tuesday have already given financial markets something to chew on. They showed what seems ostensibly like a more resilient economy than expected — stagnation rather than a contraction — but still not too much to be happy about. The fourth-quarter releases revealed that Italy and Spain outperformed economist forecasts, while France flatlined, and Germany shrank by 0.3%. Overall, the currency zone just avoided the mild recession that observers had anticipated. By contrast, according to Bloomberg Economics calculations, the US economy probably enjoyed growth in the region of 0.8% when measured on the same basis. "The data is still so resilient," Marilyn Watson, head of global fundamental fixed income strategy at BlackRock, told Bloomberg Television. "The labor market is still pretty strong. Inflation is coming down on some levels but it's stickier on some other measures." Just like in the US though, the euro-zone employment picture is tight too, and consumer prices remain a concern there as well. We'll get new data on Thursday, but an early taste of it came today in Spain, where inflation unexpectedly accelerated to 3.5% — half a percentage point more than expected. Given that backdrop, who goes first? Dominic Bunning, head of European FX research at HSBC, reckons the ECB might wait longer and deliver a reduction in June, but that the timing between them will be "fairly close." More significantly though, he reckons that once easing starts, it will turn out rather differently on each side of the Atlantic. "What you're going to start to see is the market pricing maybe a deeper cutting cycle for the ECB," he told Bloomberg Television. "Taking a view of the whole of 2024, the bigger challenge is much more in Europe — and ultimately they may need to cut rates further." - Japan's labor market showed further signs of tightness in December, driven by a manpower shortage across a swath of sectors.

- Slowing UK store inflation and mortgage approvals at a six-month high will inform Bank of England officials before Thursday's rate decision.

- The US Treasury reduced its estimate for federal borrowing for the current quarter.

- President Javier Milei is further watering down his sweeping reform bill in an attempt to get it through Argentina's congress.

- An Egyptian billionaire criticized delays in enacting a long-awaited currency devaluation. Nigeria has just moved to do so a second time.

While central bankers might well achieve a soft landing in the economy, that won't return things to the previous status quo, according to Dario Perkins at TS Lombard. He highlighted in a recent note his view that a number of trends already present before Covid but amped up in recent years are likely to impart gradual shifts in the prevailing tendencies of inflation and interest rates: - Structural labor shortages (to get worse with demographics)

- Widening geopolitical fractures

- Supply chain reconfiguration

- More extreme weather patterns

- More expansionary fiscal policy

Inflation is likely to be more volatile, with 2% as a floor, "moderately" higher real economic growth, a rising share of wages in aggregate income, and an acceleration in productivity thanks in part to technological diffusion. Bottom line: "There will be no return to the economy — or markets — of the 2010s." A stellar US recovery: Read more reactions on X |

No comments:

Post a Comment