| Is Dr. Strangelove really back with us? The attack in Jordan that left three US soldiers dead, apparently perpetrated by Iran-backed forces, has ratcheted global fears to a new level. Retired Adm. James Stavridis's column for Bloomberg Opinion makes clear that a US response of some kind is now unavoidable. Former President Donald Trump has proclaimed on social media that "we are on the brink of World War III." While that assessment is a tad exaggerated, a search of Bloomberg News Trends, which counts all news stories appearing on the terminal including from third-party sources, suggests that it has some currency. Stories about World War III are their highest in 16 months. Outside of the heated presidential campaign of 2016, the Ukraine invasion, and the assassination of Iranian military commander Qassim Soleimani in January 2020, talk of another global conflagration is at its highest in a decade: Scary stuff. And yet, as Isabelle Lee recounts below, US stock markets rallied to end the day at another all-time high. There were reasons that we'll come to, and markets have shrugged off other Third World War scares in recent years. But the fact remains that it's unwise to buy up equities in this way if you think there's a chance of an imminent apocalypse. So why the comfort level? Part of the issue is the gradual desensitization to bad news that means each fresh shock needs to be greater than the preceding one to have the same impact. After a series of atrocities, they begin to lose their ability to shake us. The last few years have had enough geopolitical surprises that arrived completely out of left field that this latest event doesn't add to the fear in trading rooms. Further, suggests Tina Fordham of Fordham Global Foresight, traders' calm can be attributed to a reading of US politics and the incentives facing President Joe Biden. "The average trader tends to rely on things like, 'The US wouldn't go into a war in an election year.' But is this time different? And why?" With Republicans led by Donald Trump goading him into action, Biden has no choice but to retaliate. As he tries to fight both Iran and Trump, it grows hard to see exactly who is Dr. Strangelove in this scenario. The task is to find a retaliation that shows strength without further expanding the conflict. "The US has to retaliate. It has to go up a level," says Fordham. "But I bet that if the US only retaliates on targets inside Iraq, I don't think the markets would blink."  George C. Scott as Gen. Buck Turgidson, before promotion to "Patton." Photographer: Columbia Pictures/Moviepix via Getty Images Finding the precise measured response to convey strength and deter Iran without provoking more escalation is not going to be easy. (See: War Room absurdity in Dr. Strangelove, or How I Learned to Stop Worrying and Love the Bomb.) The decision will rest on the shoulders of Biden himself, even if the entire US government apparatus is there to advise him. Calibrating it just wrong could provoke disaster. But for markets, the question concerning the Middle East is always whether it will push up the oil price. Another reason for calm in Wall Street is that its traders sub-contract the job of risk assessment to the oil market. If the oil price doesn't spike, then the risk can't be that great, so it's safe to stay on the stocks bandwagon. And this is how the spot price of Brent crude has moved so far this year, as a series of events have broadened the conflict: Oil swiftly fell once trading resumed after the weekend's news, reassuring traders in other markets that the risks weren't severe. They are also, arguably, skewed against disaster. If Biden's response isn't strong enough, then the US will look bad but the oil will keep flowing. Jean Ergas, chief economist of Tigress Financial Partners in New York, points out that oil is almost a binary market, and that the biggest supertankers don't go through the Red Sea and the Suez Canal in any case. "Either the oil is there or it isn't. As it is, it's dangerous, it's risky, but it's on its way." He adds that more signs of a China slowdown (implying reduced oil demand), and strong production from non-OPEC countries also helped keep the crude price down. The effects of shipping delays on the oil price could be significant, but not on the scale to drive another inflationary spiral. If the conflict were to expand to Iranian territory and stop significant amounts of oil production (possible but still not the most likely scenario at present), then the situation grows much more severe. That is the risk to monitor, and the oil price suggests it's still not that great. However, concentrating on oil may not capture the dangers to inflation. This is how the price of Shanghai containerized shipping (including routes through both the Panama and Suez canals) has moved recently. Questions over both choke points for global shipping have had their effect: Tom Holland of Gavekal Economics estimates the costs of rerouting around Africa for those tankers that could have used the Red Sea as adding at least 6,000 kilometers and 10 days to voyages. With daily charter costs for tankers doubling in the last six months, he thinks that this should add "more than $1 to the cost of each barrel of oil, on top of the heightened general risk premium." That is less than catastrophic, but threatens to raise prices even without further major escalation. Another risk comes from the fog of war. Attacks on Houthi infrastructure impede their ability to launch well-targeted attacks. That might add to the case for ships to head for the tip of Africa. According to Holland: Until recently, Yemen's Houthis have said they will not target Russian (or Chinese) shipping. But the more the Houthi targeting ability is degraded by US air strikes, the greater the risk of indiscriminate attacks against neutral vessels, and the bigger the incentive for shippers to reroute vessels to avoid the Gulf of Aden and the Red Sea.

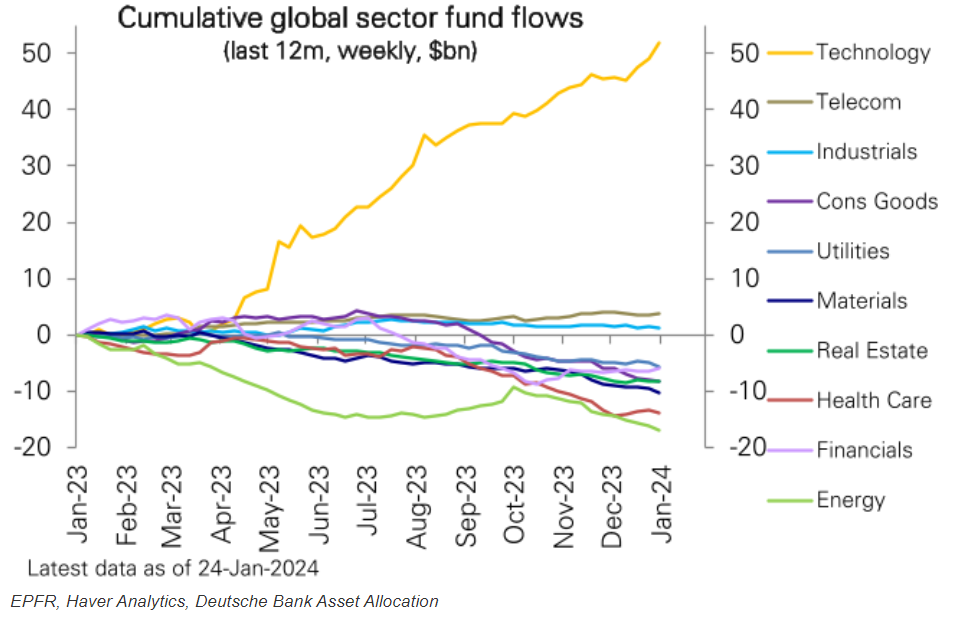

This affects monetary policy by creating another inflation supply shock, even if a broad all-out war is avoided. Ed Yardeni suggests even that the risks of major delays "also increases the risks of a second bout of inflation similar to what happened during the two energy crises in the 1970s." That is never a comfortable comparison. Now to look at what else drove markets on a day of bleak news. Possibly the most consequential week of this earnings season is underway. Five megacaps with a combined market value of more than $10 trillion are slated to report. Between Tuesday and Thursday, they include Microsoft Corp., Alphabet Inc., Meta Platforms Inc., Amazon.com Inc. and Apple Inc.. For the full week, 108 S&P 500 companies — around 39% of the benchmark's market cap — report. "Technology companies may determine success or failure for the S&P 500 earnings season as well as index earnings in 2024," wrote Bloomberg Intelligence's Gina Martin Adams and Gillian Wolff. As it stands, Wall Street expects roughly 16% year-over-year earnings growth from the sector. Only six months ago, it was braced for an outright contraction of 2%. This is almost a mirror image of expectations for the rest of the S&P — analysts now expect a 2% contraction, down from expectations of nearly 6% growth just three months ago. So a lot is resting on tech; it would be nice if the consensus were right. As it stands, the big tech groups are regarded almost as a bulwark against Middle Eastern conflagration. It's the consensus for a reason. Megacap tech shares have driven most of the gains of the market. Data from Deutsche Bank Research show that positioning in tech is the only one notably above historical average, at the 73rd percentile. Inflows into tech ETFs and mutual funds, which were already strong, accelerated to the highest in five months at $2.8 billion. Over the last 12 months, the sector has swamped all others to a remarkable extent: The leviathans' earnings announcements will be interrupted in midweek by the Federal Reserve and the Treasury. It would be astonishing if the central bank did not hold rates steady on Wednesday afternoon, but much depends on Chair Jerome Powell's willingness to trail a rate cut for the next meeting in March. "The Fed will try to douse hopes of any early easing in policy," wrote David Kelly, chief global strategist at JPMorgan Asset Management. "This is, in part, because they are genuinely uncertain about how sticky inflation might be in an economy experiencing above trend economic growth and a still very tight labor market." Optimism about an economic soft landing has pushed stocks to price in an "immaculate everything" scenario, said Chris Senyek of Wolfe Research, in which "the Fed cuts deeply and the US economy (at worst) glides down… While we're still not believers, our sense is that the Fed and economy are now 'show me' stories." Monday's key development came at 3 p.m., when the Treasury made its quarterly refunding announcement and the market dodged another bullet. With federal debt at historically high levels, the minutiae of how much the government borrows and on what terms grow far more important. Senyek had suggested that the greatest risk of a "definitive downside catalyst" could have been an announcement of increased borrowing. Instead, borrowing for this quarter will be lower than previously advised, and then much lower in the second quarter. At least for one day's trading, that proved to be a definitive up-side catalyst:  Possibly even more important will be the announcement Wednesday, before US markets open, of how the Treasury intends to apportion its borrowing. It decided earlier this year to raise far more from short-term bills than usual; whether that continues, and the size of the auctions Uncle Sam wants the market to swallow, remain hugely important questions. If we look at how stocks and bonds have done (in the customary 60/40 portfolio) over the last 12 months, we can see that the last two quarterly refunding announcements both marked big turning points. The need to raise more funding scared the markets in August, and the measures to cushion the blow announced in November were critical to the end-of-year rally that followed: After the Treasury and the Fed, nobody can slope off for a long weekend. The usual raft of first-day-of-the-month economic numbers from around the world is due on Thursday, followed by Payrolls Friday. Enjoy. — Isabelle Lee  Slim Pickens taking global apocalypse less than seriously. Photograph: Sunset Boulevard/Corbis Historical The apocalypse is no laughing matter. However, for attempts to make a little light out of it, try The End of the World from Beyond the Fringe, featuring a youthful Peter Cook, Dudley Moore, Alan Bennett and Jonathan Miller; Whoops Apocalypse, a darkly brilliant British sitcom from the 1980s, the extremely dark video that Ariana Grande made for One Last Time, the nightmarish piece of synthpop from OMD called The Misunderstanding, or a certain song by REM. And then there's the utter genius and pitch-black comedy of Stanley Kubrick's masterpiece from 1964. After all, it ends with uproarious laughter. Any more suggestions? And cheer up, it may never happen.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment