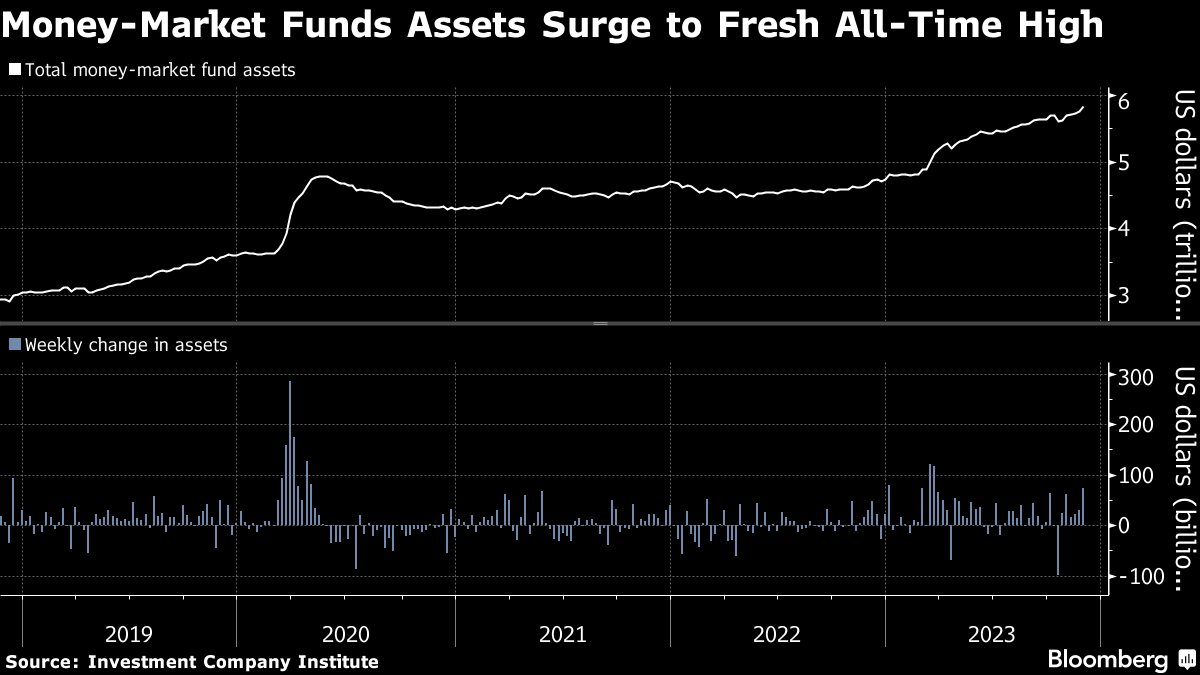

| Welcome to the Weekly Fix, the newsletter with a process you can respect and understand. I'm cross-asset reporter Katie Greifeld. It's that time of year when everyone pokes fun at Wall Street strategists for their year-ahead targets that never came to fruition. There's plenty of material to make hay with this time around: recall that heading into 2023, the average forecast called for the S&P 500 to decline, the first negative prediction since at least 1999. So naturally, the S&P 500 is sitting on 19% year-to-date gains. But an interesting wrinkle is that the root cause of some of the most bearish fantasies was generally correct: the Federal Reserve was more aggressive than widely expected, and yields soared to eye-watering heights as a result. However, it was the follow-through from those higher rates that has yet to materialize: the widely heralded recession never came, corporate profits didn't exactly crater and US consumers are still spending. There's a few potential reasons why. One, the US economy is less rate-sensitive compared to past cycles — a dynamic that Fed chair Jerome Powell acknowledged just last month. That's resulted in longer and more variable lags. Second, it turns out that the S&P 500's heaviest hitters — the megacap technology companies — don't necessarily have an adversarial relationship with higher rates. Rather, the tech companies that have powered index-level gains in the stock market this year are generally better equipped to deal with interest expenses and refinancing risks than their smaller brethren. Additionally, companies such as Alphabet Inc. and Tesla Inc. have actually profited from their massive cash hoards in recent quarters. In sum, the 2023 Wall Street forecasting experience raises a question that this newsletter has asked before: even if you knew, what would you do? Having the proper information and starting point in hand is useful, but markets are under no obligation to behave. It's a fun thought exercise. "I think it's fashionable to make fun of strategists when they're wrong, but at the end of the day, if you have a process you can respect and understand what drove them to that decision, they can still be valuable," Adam Parker, CEO of Trivariate Research and former Morgan Stanley chief US equity strategist, told Bloomberg's Alexandra Semenova. A defining feature of 2022 was cash's outperformance in a year when everything went wrong. In 2023, demand intensified further. Heading into 2024, that momentum is still building. Assets in money-market funds soared to yet another record high of $5.8 trillion in the week through Nov. 29, according to Investment Company Institute data. A $73 billion inflow pushed it to those fresh heights — the largest weekly haul since March, when tremors in the US financial system drove depositors out of banks. All told, more than a trillion dollars have been added to money-market funds so far in 2023. Lofty yields on the shortest-dated paper means that cash is attractive beyond its traditional role as a safe-haven asset. Meanwhile, depositors — rattled by March's events, and frustrated by banks not passing on higher rates quickly enough — have flocked to money-market funds as well. In the eyes of Federated Hermes' Deborah Cunningham, another trillion dollars is in the offing. Next year should be "another banner year" for money-market funds, she said, given that the massive inflows thus far have primarily been from retail investors. "What hasn't really started in earnest yet is the institutional movers," Cunningham, the firm's chief investment officer for global liquidity markets, said in a Bloomberg Television interview. "Those institutional movers generally wait until interest rates have peaked or plateaued, and then they really start to come into the product once rates start to go back down again." A bond exchange-traded fund crossed $100 billion for the first time since such products launched over two decades ago. Assets in the Vanguard Total Bond Market ETF (ticker BND) pushed above $100 billion for the first time ever, data compiled by Bloomberg show. BND has absorbed $15.6 billion so far this year. The milestone marries two of 2023's biggest trends: the highest yields in years have made fixed-income more appealing, while relatively low-cost, tax-efficient ETFs have consistently stolen market share from their more expensive mutual fund brethren. "There's likely a large portion of flows coming from mutual funds too, as a source of growth," said Todd Sohn, ETF and technical strategist at Strategas Securities, adding that since the interest-rate liftoff in March 2022 through last month, fixed-income mutual funds have lost $500 billion. BND's $100 billion breakthrough comes amid a turbulent year for fixed income. Stubborn inflation and the Fed's campaign to cool it unleashed volatility across asset classes, sending Treasury yields soaring to decade-plus highs. Growing conviction that the central bank has reached the end of its tightening cycle ignited a fierce bond rally over the past month. All the while, BND — which charges 0.03% per year — has steadily taken in cash over the course of 2023. "It's not surprising when you offer up 18,000 bonds for three basis points that's going to get weatherproof flows," said Bloomberg Intelligence senior ETF analyst Eric Balchunas. "That's money coming in rain or shine, because it's that good of a deal." BND, which tracks everything from Treasuries to corporate credit to securitized assets, has fared better. The fund has gained about 2% on a total return basis so far in 2023, and hasn't posted a monthly outflow since May 2022. |

No comments:

Post a Comment