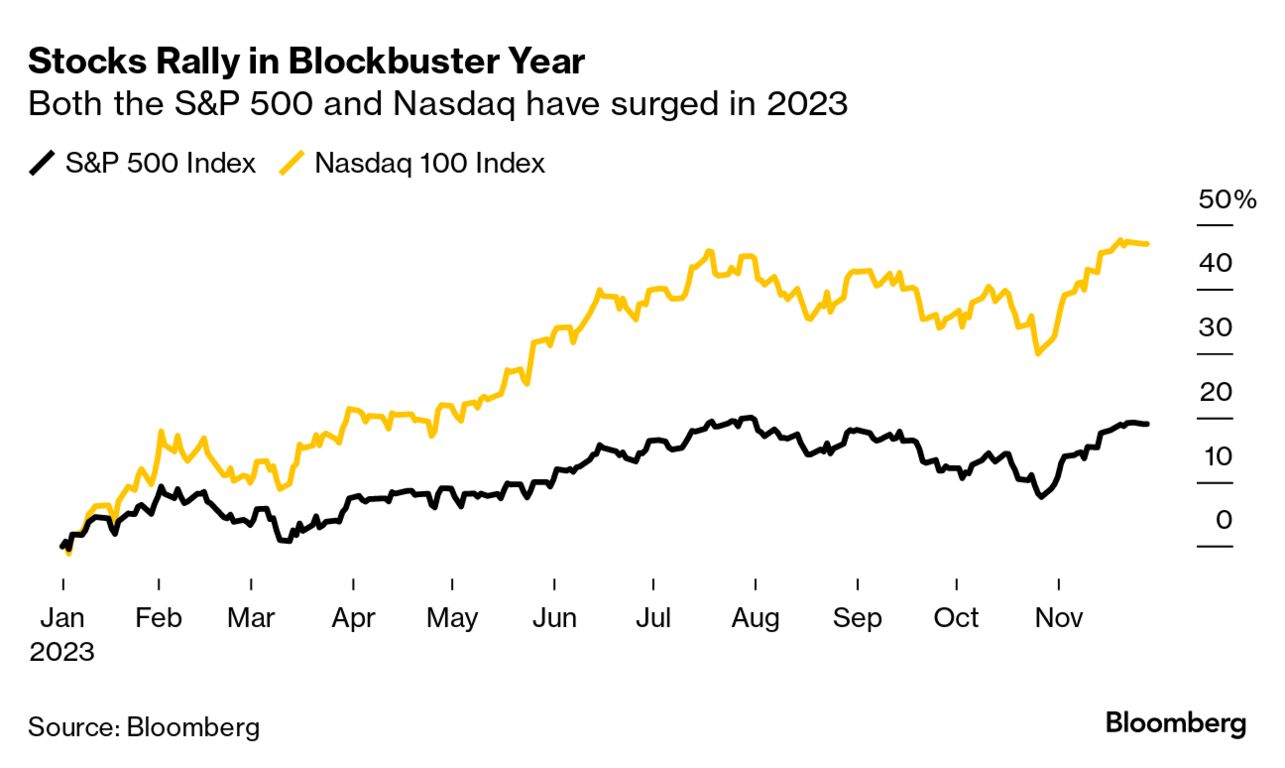

| It's beginning to look a lot like a lucrative time to sell stock. The S&P 500 is up almost 19% since the start of the year. The Nasdaq 100 has gained even more at 46%. Mega-cap tech stocks from Apple, Meta and Tesla are a huge part of this lift, and as our story this week points out, it's prompting many retail investors to exit tech for cash. Should you follow? Before we get to that though… Three things to know: …now back to that question about selling stock. It's the sort of quandary Jack Heintzelman, a financial planner at Boston Wealth Strategies, says he often gets from clients at two points: when markets are up and when the year is almost over. Gains excite investors, and a new year looming makes them reflective. Heintzelman says the decision to sell comes down to an individual's circumstances, how diversified they are, and what their time horizon is. That said, he notes a major case for selling is if you need to "rebalance" a portfolio that has become overweight a certain sector and drifted from your original allocation plans. "When you rebalance, you sell out of some of your winners and you go buy — maybe they're not losers — but they're up less than what your winners have done," he says. The goal is to maintain a more diversified portfolio with holdings that won't be all up or all down at the same time. Those who decide to sell should beware of the tax implications, however, warns Anora Gaudiano, assistant vice president at Wealthspire in New York. Taxes on capital gains are levied on profitable investments, and how long you held the stock determines how much you'll owe. "Long-term capital gains have a preferential tax treatment," notes Guadiano. "They're treated at a lower tax bracket, and short-term capital gains are treated as ordinary income." Similarly, advisers recommend that investors looking to sell consider how they can take advantage of tax-loss harvesting. It's a popular strategy allowed by the US tax code that lets investors sell poor-performing stocks and use those investment losses to offset capital gains from sales of better-performing assets, including stocks, bonds, a home or business. Alternatively, some investors may find the opposite strategy, tax-gain harvesting, might help reduce their IRS obligations. In years when investors have lower incomes but investments with profits they'd like to lock in, it could be good time to sell because their tax brackets may be lower, says Derek Thompson Williams, a wealth adviser at Veratis Advisors in Cary, North Carolina. Still, advisers generally caution against selling in an up market if it's not part of a predetermined plan. The risk is always that the market continues to go up, and your money sits on the sidelines as you wait for a good time to re-enter. And you don't have time for that. — Charlie Wells Send us questions about your own financial dilemmas to bbgwealth@bloomberg.net. How should I prepare financially if I want to quit my job this year? Sarah Behr, founder of Simplify Financial in San Francisco, writes: Before you embark on a work hiatus or sabbatical, review your cash flow and seek to gain an honest understanding of your cost of living. On a month-to-month basis, how much do you spend? Break it down by fixed expenses such as housing, utilities and insurance and variable expenses such as food, entertainment, shopping, travel and transportation. Don't skimp and be honest with yourself. Once you have a ballpark figure of your monthly expenses, make sure you have at least six months of cash reserve to float you during your time away from work. Preferably you're using a high-yield savings account earning 4.5% interest at a minimum. Plan for out-of-pocket health-insurance costs to increase while you're unemployed. Get all your preventative care appointments out of the way before you leave your job (dental cleaning, annual physical). If you intend to travel or take classes that may increase your expenses; build this into your cash reserves. If you think you may be unemployed for over six months, consider increasing the cash reserve to 12 months to be on the safe side.

Miriam Adelson Photographer: Andrew Harrer/Bloomberg |

No comments:

Post a Comment