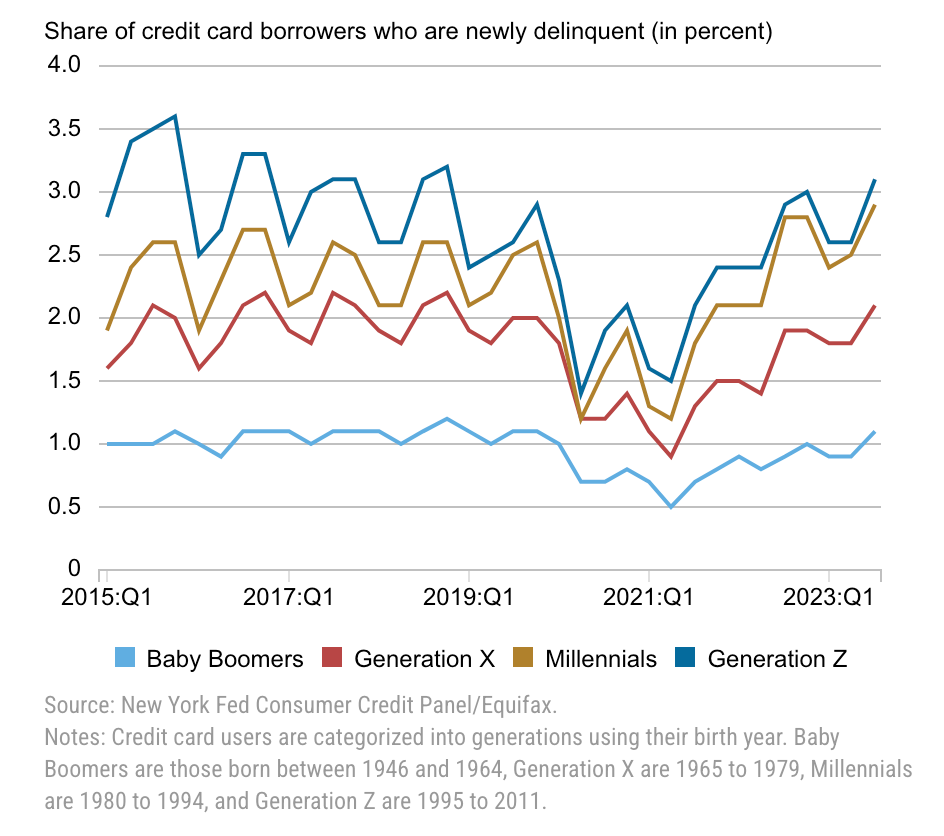

| Just yesterday, the New York Fed broke down its Q3 Quarterly Report on Household Debt and Credit, pointing out that the rise in credit-card delinquencies and overall credit distress in the US has been concentrated with Millennials and poorer households. This tells you the debt stress has already begun but is being masked by the financial wherewithal of wealthier households and older generational cohorts. Here are a couple of highlights from the part on credit cards: - Credit card distress for Millennials: "The series shows that 2 percent of credit card users moved from current status in the second quarter of 2023 to thirty or more days past due on at least one account in the third quarter. This is up from roughly 1.7 percent in the first and second quarters of 2023, and higher than the third quarter average between 2015-19 of 1.7 percent."

-

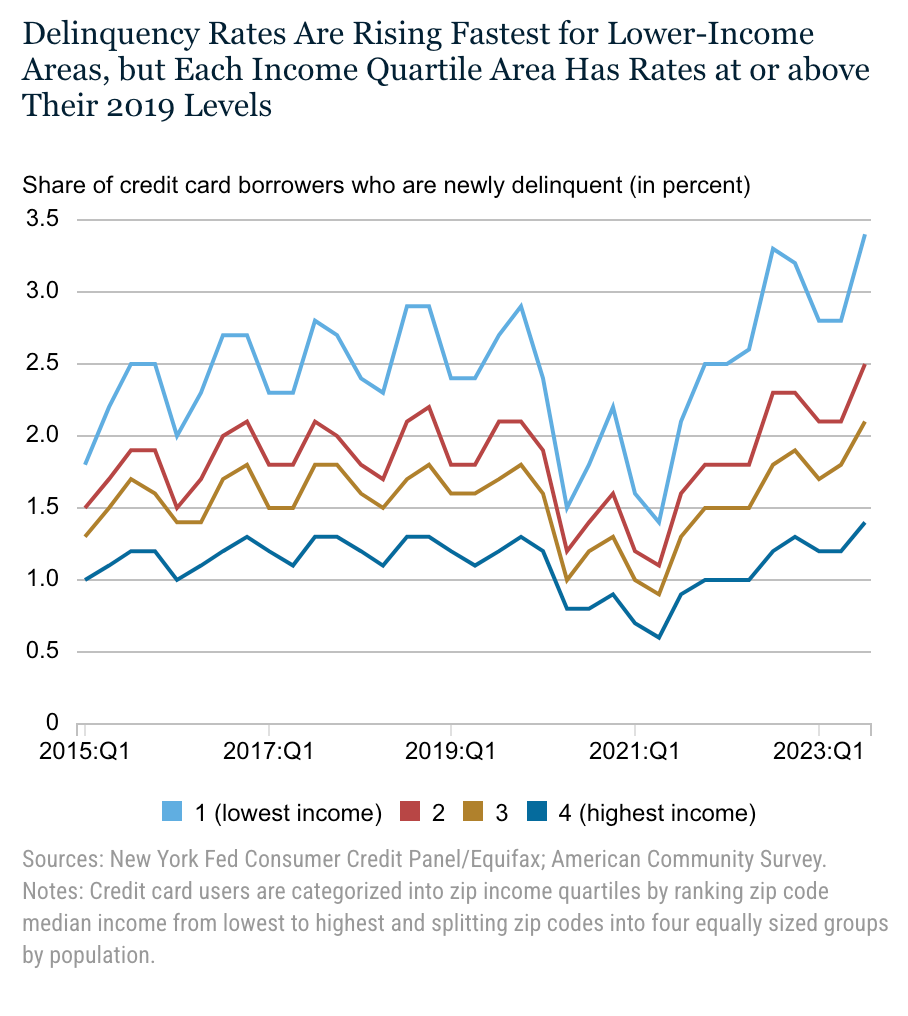

Credit card distress for lower-income households: "The chart below shows how credit card delinquencies have evolved by zip median income. We categorize all zip codes into four groups ranked by area income with the first quartile representing the lowest and the fourth quartile representing the highest income. The lowest-income areas persistently have the highest delinquency rates, but all four quartiles are now above their pre-pandemic levels." You see the same patterns in auto loan and student debt as well. The NY Fed concludes: Even though the increase in delinquency appears to be broad based across income groups and regions, it is disproportionately driven by Millennials, those with auto or student loans, and those with relatively higher credit card balances.

I've lamented before how the Fed's interest-rate medicine isn't very targeted. In effect, what you're seeing here is an economy divided into higher-rate haves and have-nots based on household income and the age of the borrowers. Rates during the pandemic were epically low. And those who could, took advantage of that to lock in the lowest borrowing costs of a lifetime. Insulated from rate shock on loans, they like rising rates because it bolsters their interest income. Those who couldn't get low borrowing rates — because of poor credit or low income or whose needs have changed because they are only now forming a separate household — are bearing a considerable cost. In fact, because the Fed's policy works mostly through credit channels to slow the economy, they are the main conduit through which the economy-wide slowing from higher rates is channeled — and, thus, must disproportionately feel pain. Looking at the New York Fed's charts, you can see this debt distress already started rising in the second quarter of 2021 but has only recently hit levels higher than the pre-pandemic averages. Where we go next depends a lot on the back and forth between market expectations and the economy. The Atlanta Fed's economic tracker GDPNow suggests the economy is now growing at about a 2% pace, decent but down from nearly 5% last quarter. The combination of this slowdown and guidance from Fed officials has meant a real climbdown in long-term interest rates from levels Federal reserve Governor Christopher Waller just called an "earthquake" for the economy. The lower 10-year Treasury rate has meant a massive easing in financial conditions, helping the S&P 500 to the most number of consecutive day gains in two years. It has also meant lower mortgage rates, with 30-year mortgages falling the most in more than a year. All of which is to say, it has eased the pressure on the economy. And if that easing subsequently turns out to be too much, we'll see another bout of tightening until we settle on a landing — hard or soft — for this economy. When the dust settles, the Millennial generation will have seen a wrenching transition to a new normal, the likes of which no generational cohort has ever seen. The interest rate hikes in the early 1980s were higher, but the youngest Baby Boomers were just 16 to 18 when it happened and the oldest were 34 to 36. The full weight of that cycle did not fall on them. What's more, they benefitted from the subsequent fall in interest rates during the 1980s and 1990s that produced a long run-up in stock, bond and house prices. If I'm right that the days of zero rates are well and truly over, then after this business cycle ends, the rate relief will be much less than back in the 1980s. And so, any kick higher in real estate, bond and equity asset prices will be much less than what Boomers saw. It will be a rough transition to the new higher for longer regime. And unfortunately, one generation will bear much of the burden. That's bound to change their outlook on life and politics as they become the dominant social and political force for years to come. |

No comments:

Post a Comment