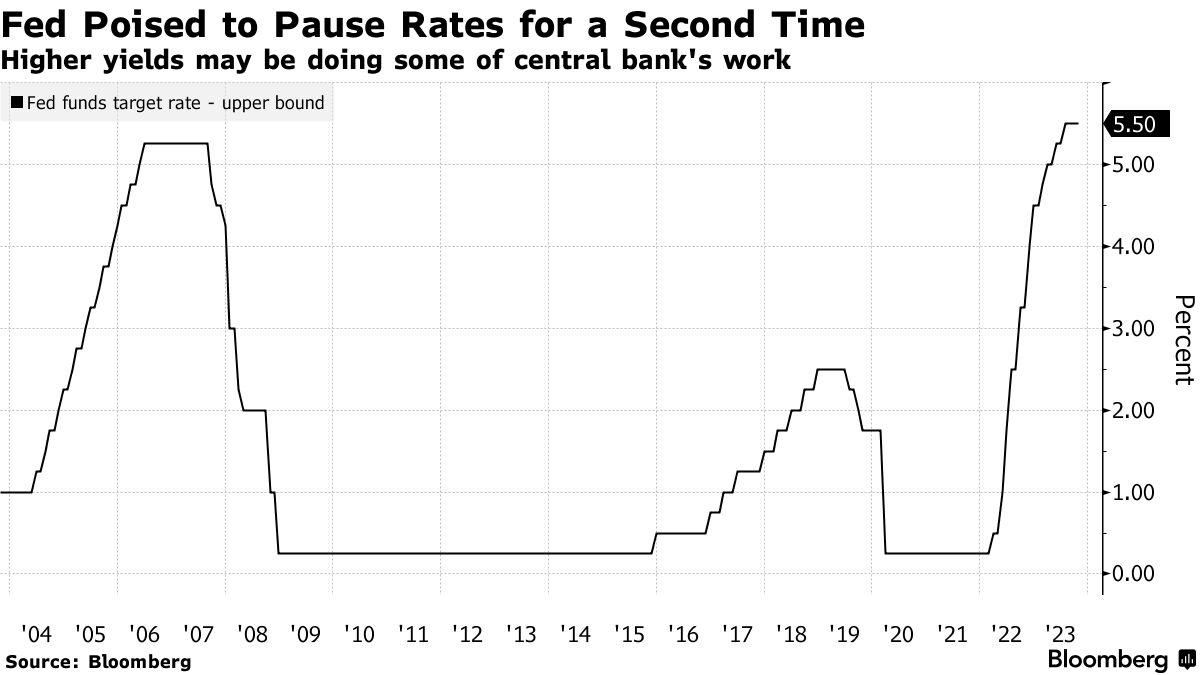

| I'm Craig Torres, a Federal Reserve reporter in Washington, and today we're looking at the US central bank's looming policy decision. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X (formerly known as Twitter) via @economics. And if you aren't yet signed up to receive this newsletter, you can do so here. For the first time since they started hiking interest rates 19 months ago, Federal Reserve policymakers on Wednesday have signaled they will stand pat for a consecutive meeting, suggesting a shift in their approach. For some time now, Chair Jerome Powell and his colleagues have been "data dependent." Strong economic indicators drove them to tighten policy more. Evidence of a slowdown in inflation allowed for smaller, and fewer, rate hikes. That period may be largely over. The latest data have come in hot — retail sales, nonfarm payrolls, housing activity and inflation have all been stronger than forecasters expected. Nevertheless, policymakers clearly telegraphed that they'll hold rates again this time, in a vote likely to be unanimous. One reason to hold: the surge in longer-term interest rates thanks to a selloff in Treasuries that has been prompted by a raft of causes, from the strong economic data to the government's escalating borrowing needs. "The data is making a very hot case to tighten monetary policy, but the Fed is taking up the financial conditions narrative" and saying the rise in Treasury yields counts for additional tightening, says Carl Riccadonna, chief US economist at BNP Paribas.

The broader takeaway is that Fed is now in the mode of risk management. It's putting as much weight on avoiding an overshoot in monetary tightening that kills off the expansion as it is on getting inflation back to the 2% target. Fed officials forecast the US economy will slow below trend next year. But they also appear unwilling to test the economy's stall speed, and are banking on favorable supply trends to cool off prices. The new strategy is itself risky against a backdrop of an economy that just picked up steam to post 4.9% annualized real growth last quarter. In nominal terms, the expansion was about 9%, faster than China. "Inflation risk has gone up," says Robert Brusca, president of Fact & Opinion Economics. "We have a more militant labor force, we have a tight labor market, we have big deficits, we have rising oil prices."

He called a soft landing — where inflation decelerates without much economic pain — "an improbable event, and you shouldn't bet so much on it." Powell's post-decision press conference will be keenly watched for any signal about the openness to hiking rates in the final 2023 meeting. A third straight skip on Dec. 13 would surely convince financial markets that the policy rate has now peaked at the current target range, of 5.25% to 5.5%. Bloomberg's New Economy Forum returns to Singapore Nov. 8-10 as the world's most influential leaders gather to address critical issues facing the global economy. This year's theme, "Embracing Instability," focuses on underlying economic issues such as persistent inflation, geopolitical tensions, the rise of AI and the climate crisis. Request an invitation here. - Brazil's central bank will likely deliver its third half-point rate cut.

- The next UK government has a $172 billion spending headache on its hands.

- A private survey of China's factory activity signaled more economic fragility. Meanwhile, Asian manufacturers are grappling with rising costs.

- Argentina made a $2.6 billion payment to the IMF ahead of a presidential runoff election.

- The IMF is urging Australia to tighten policy further to quell inflation.

- South Korean exports finally returned to growth, boosting the outlook.

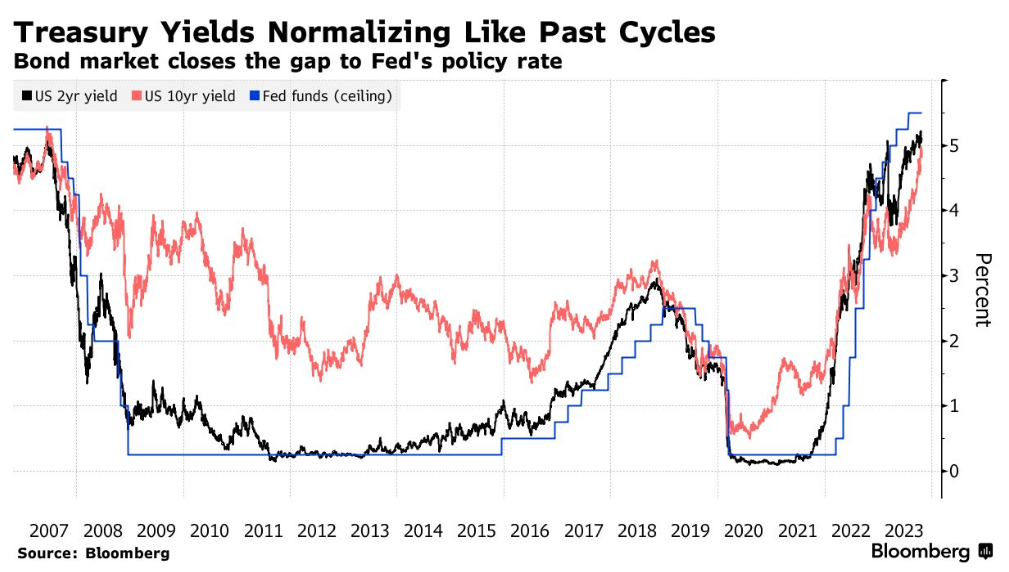

Fed policymakers may have good reason to think that the surge in longer-term US Treasury yields in recent months — 10-year rates are up more than three-quarters of a percentage point since the start of August — will do some of their work for them in slowing the economy. A simulation that Fed economists ran in 2013 reckoned a 75 basis point-rise in Treasury yields would cut 2014 growth almost a percentage point, and boost unemployment about 0.75 percentage point by the end of 2015. The implication for policymakers: The Fed's benchmark rate is more than half a percentage point lower than otherwise by the end of 2015. Anna Wong, a former Fed economist now at Bloomberg Economics, sees a significant impact from higher yields feeding through to weaker growth this time as well. The takeaway, she said in a recent note on the Bloomberg terminal, is that rates may be higher for shorter — not longer. Read more reactions on X |

No comments:

Post a Comment