| I'm Chris Anstey, a senior economics editor in Boston and today I'm looking at Argentina's economic policy dilemma. Send us feedback and tips to ecodaily@bloomberg.net or get in touch on X (formerly known as Twitter) via @economics. And if you aren't yet signed up to receive this newsletter, you can do so here. - China's manufacturing and services sectors slowed in November.

- Euro-zone inflation cooled more than expected.

- An EU-South America trade agreement could be reached soon.

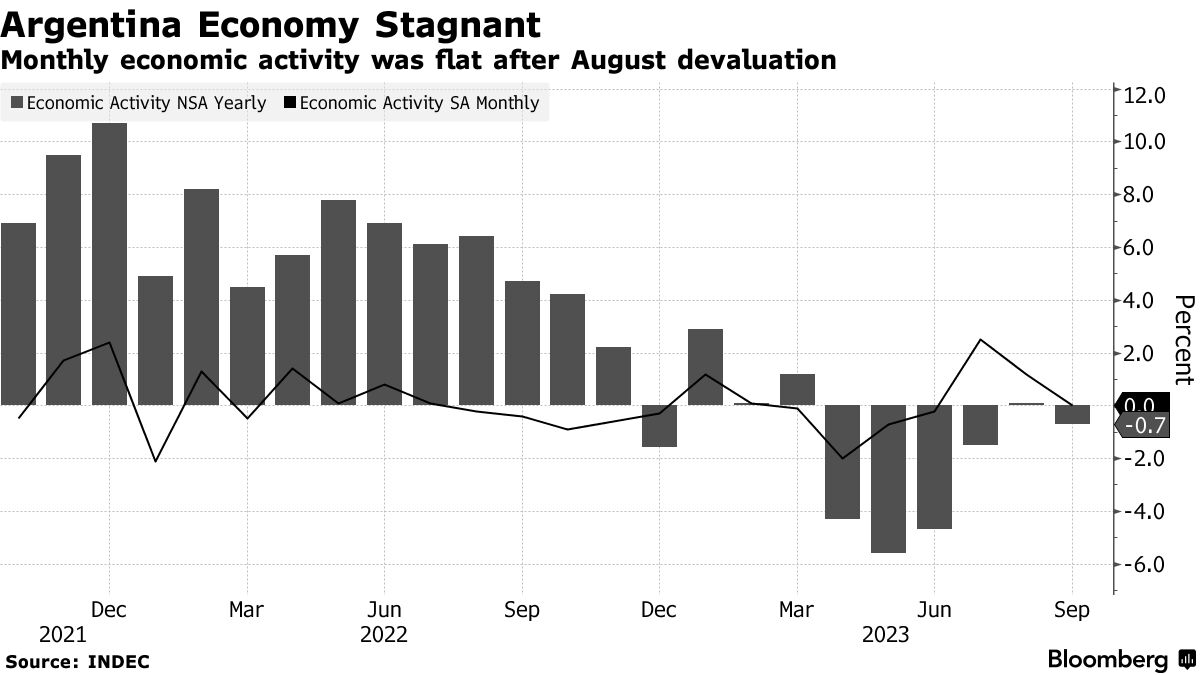

Argentina should, as its president-elect has proposed, adopt the US dollar as the nation's currency, according to a former director of the Federal Reserve's international division. An ex-top career official at the US Treasury's international section says the opposite. The differing views serve to showcase how there's no obvious answer to the challenges of the South American nation, which once was among the world's richest in per-capita output terms. After stabilizing for a time in the 1990s, Argentina's economy has had a rough time in the current century, with repeated bouts of high inflation, exchange-rate depreciation and debt default. The latest data showed GDP shrank over the 12 months to September while the monthly pace of inflation hit almost 13% — a pace unseen since the early 1990s. Desperate for change, voters opted in this month's presidential election for Javier Milei, whose platform included dollarizing the economy. Steven Kamin, the former Fed official who's now at the American Enterprise Institute, wrote Monday that the radical step would deal with inflation once and for all by removing the ability of Buenos Aires to print money. It would have to borrow to finance budget deficits, and — assuming those continue to be excessive — defaults would ultimately enforce fiscal discipline. Mark Sobel, the ex-Treasury official who's currently US chair of the Official Monetary and Financial Institutions Forum, is among the many who see the debate over dollarization as a "diversion." The bottom line is simply that "Argentina doesn't have the dollars for such a regime," he wrote in his own note Monday. Bloomberg Economics recently did the math: It would take about an 86% devaluation of Argentina's peso in order to exchange its currency base into dollars. And that could trigger a "depression." The risks involved "advise against committing to dollarization before there's been a successful fiscal adjustment and boost to reserves — which could facilitate the process at a reasonable rate," Adriana Dupita at Bloomberg Economics wrote Nov. 22.  Javier Milei. Photographer: Anita Pouchard Serra/Bloomberg Indeed, Milei himself has suggested that the move, which would face major legislative hurdles, is on pause until he can rein in public spending to balance the budget. On Wednesday, the incoming president indicated that a former finance chief, Luis Caputo, will take the reins as economy minister. His top task arguably will be figuring out how to unwind a web of currency controls and price freezes imposed by the outgoing government without triggering hyperinflation. While it sounds an impossible task, other Latin American nations have proved able to contain prices with their own reform programs. Monica de Bolle at the Peterson Institute for International Economics advises that Argentina set up its own new currency, alongside deep institutional reforms, to revive trust. Milei and Caputo have their work cut out for them. - Two Federal Reserve officials made the case for continuing to hold interest rates steady, while a third warned that the risk of stubborn inflation should keep the option to hike further on the table. Meanwhile, a regional Fed report showed US economic activity slowed in recent weeks.

- France's economy unexpectedly contracted in the third quarter, prompting investors to step up bets that the ECB will cut interest rates in the spring.

- China's President Xi Jinping visited Shanghai for the first time in three years, putting a spotlight on the mainland's top financial center.

- Saudi Arabia has approached Iran with an offer to boost cooperation and invest in its sanctions-stricken economy if the Islamic Republic stops its regional proxies from turning the Israel-Hamas war into a wider conflict.

- The Bank of Korea softened the tone of its hawkish holding pattern on interest rates while trying to tame speculation over an early policy pivot with warnings about stickier-than-expected inflation.

- Turkey's economy cooled last quarter as the central bank moved to tighten monetary policy after May elections, a pivot that's turning around sentiment among investors without crashing growth.

UBS economists have called attention to a line in minutes of the Federal Reserve's last policy meeting, released last week, that highlighted how all participants judged that policy settings should remain "restrictive" for "some time." They didn't say that interest rates should be kept at current levels for some time. "Higher for longer is not the same as restrictive for longer," the UBS economists led by Jonathan Pingle wrote in a note last week. Restrictive for longer suggests that, should inflation keep coming down, the policy rate could be lowered, the team wrote. The UBS team went on to predict that, at the Dec. 13 press conference, Chair Jerome Powell will explain the importance of real rates — that is, adjusted for inflation. Looking at communications into 2024, the Fed could advise "that any rate cut is seen within the context of policy still being 'restrictive for longer,'" the economists wrote. Read more reactions on X |

No comments:

Post a Comment