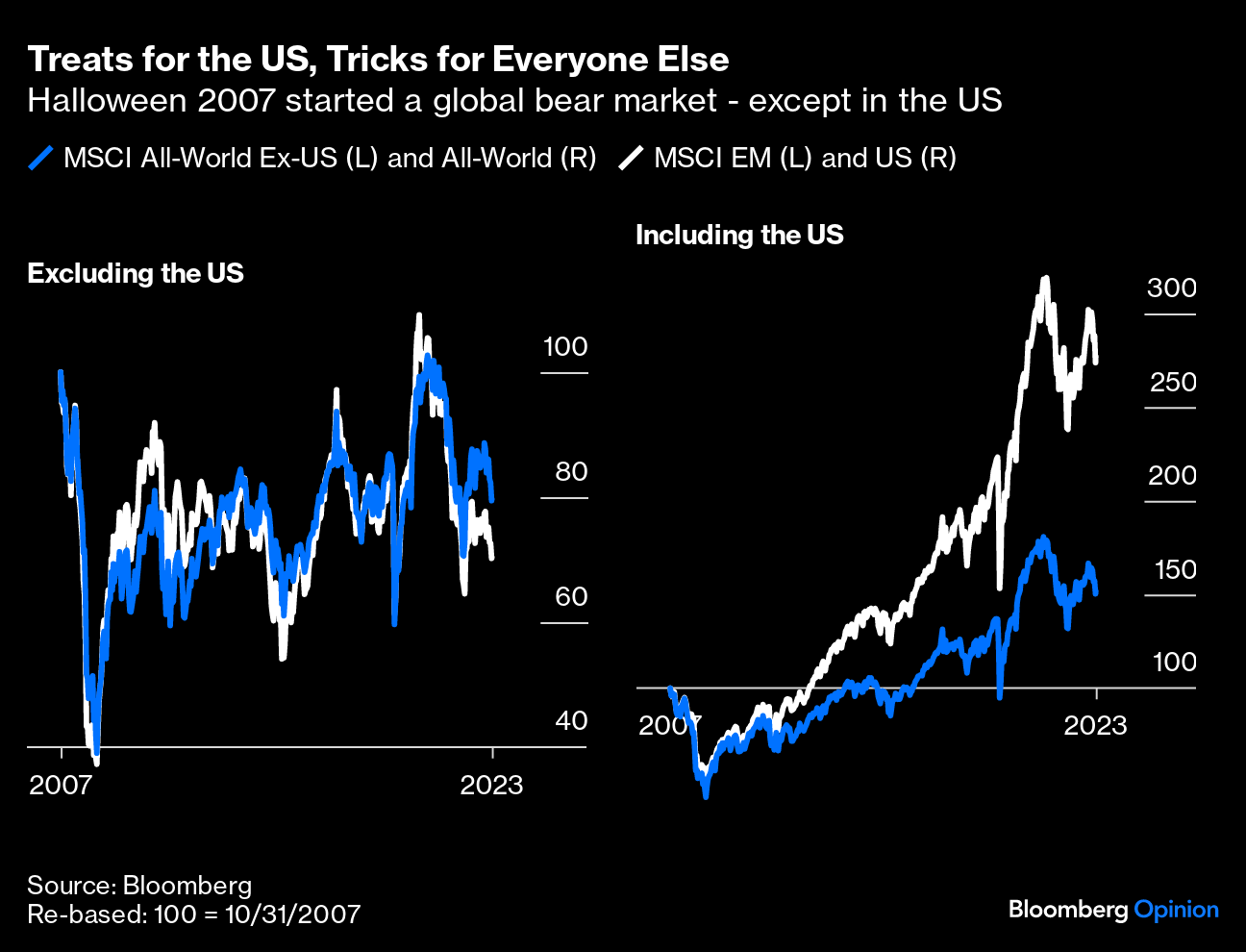

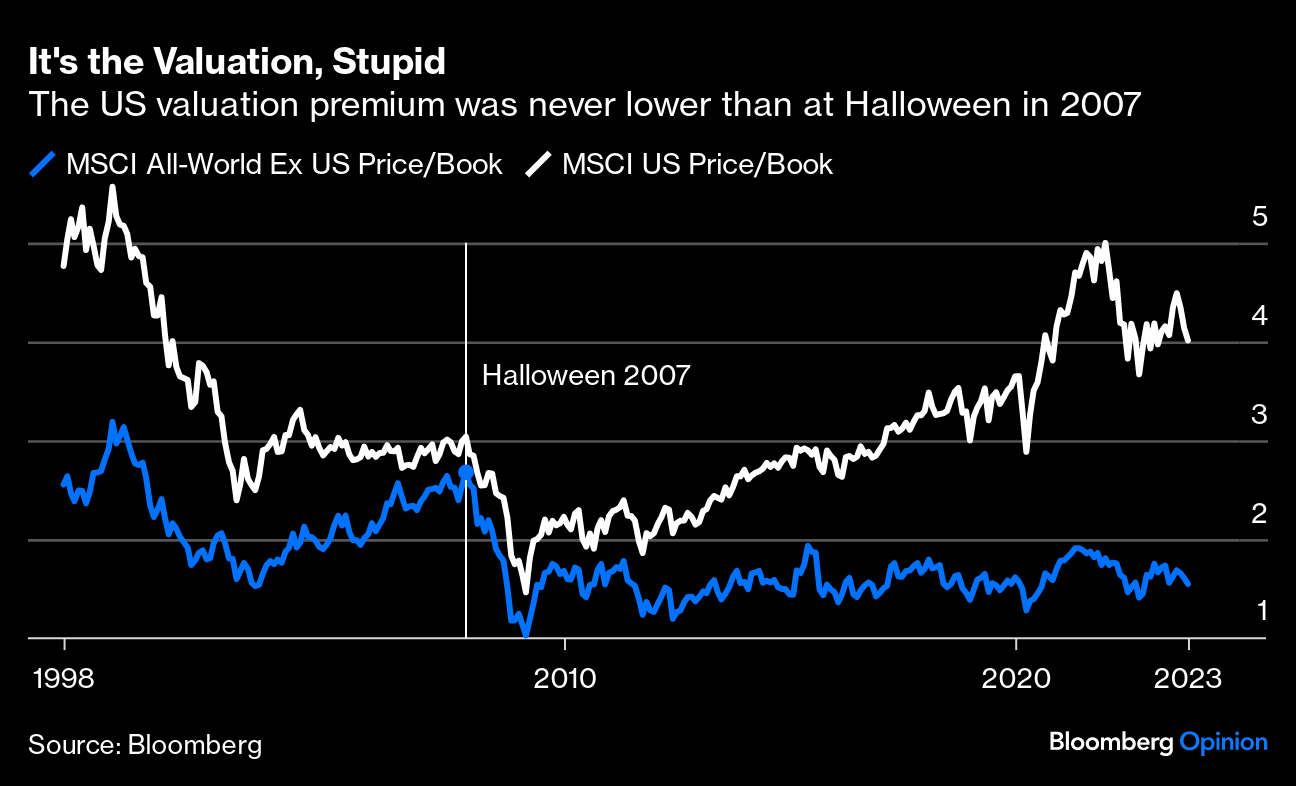

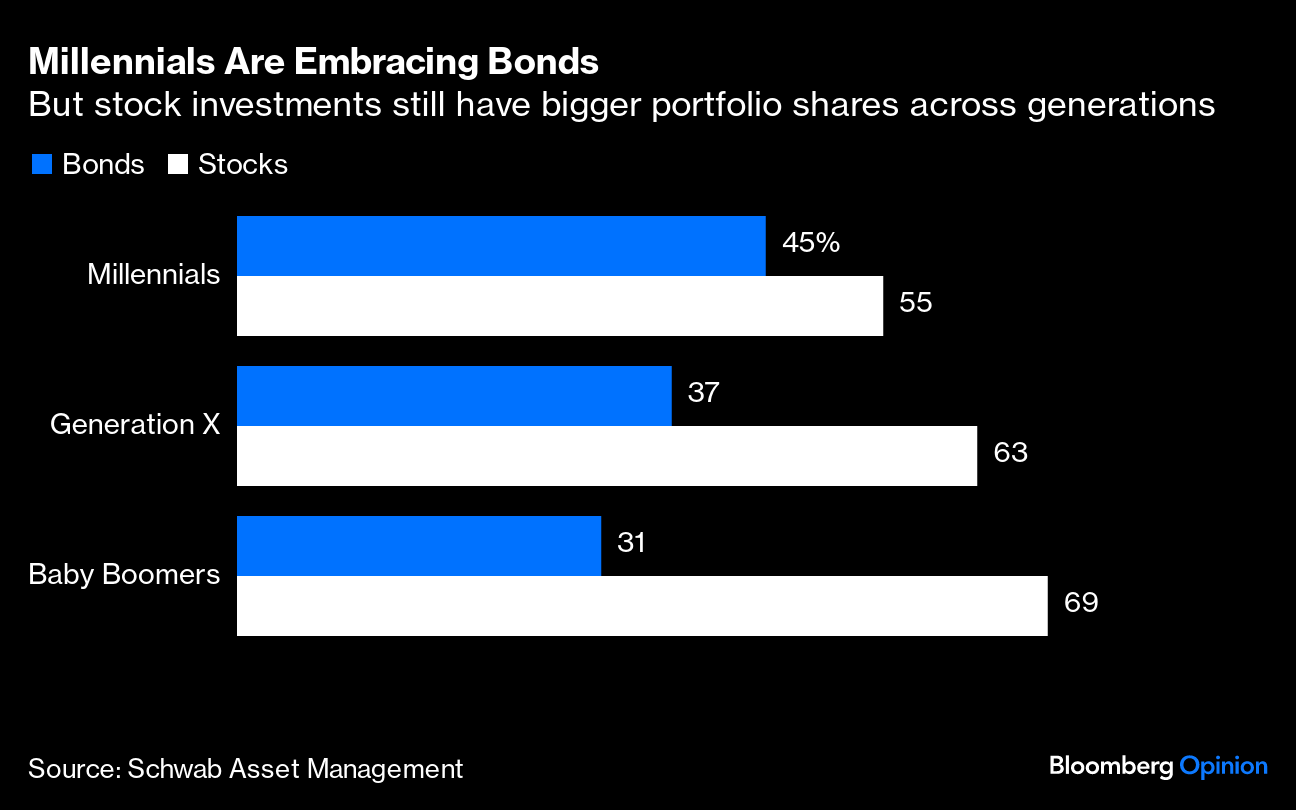

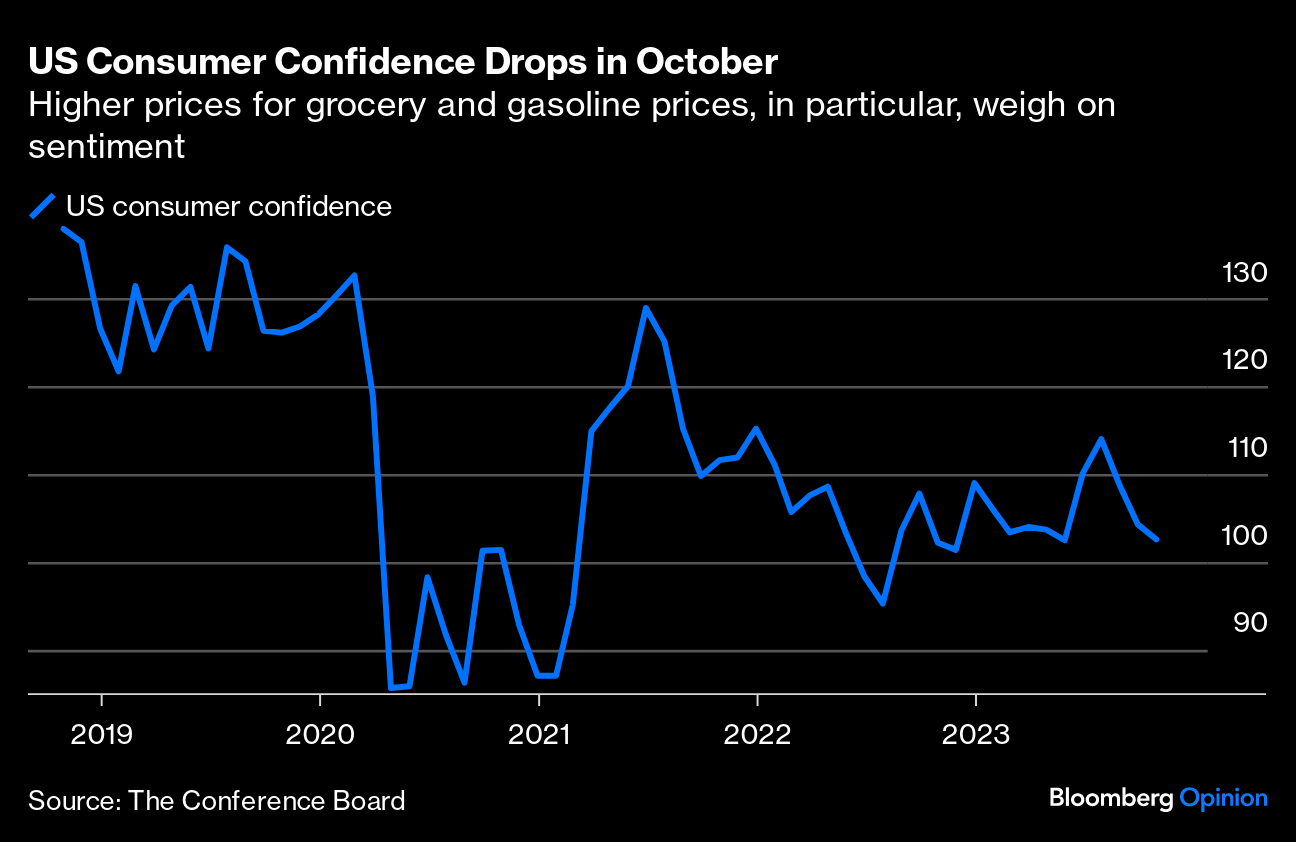

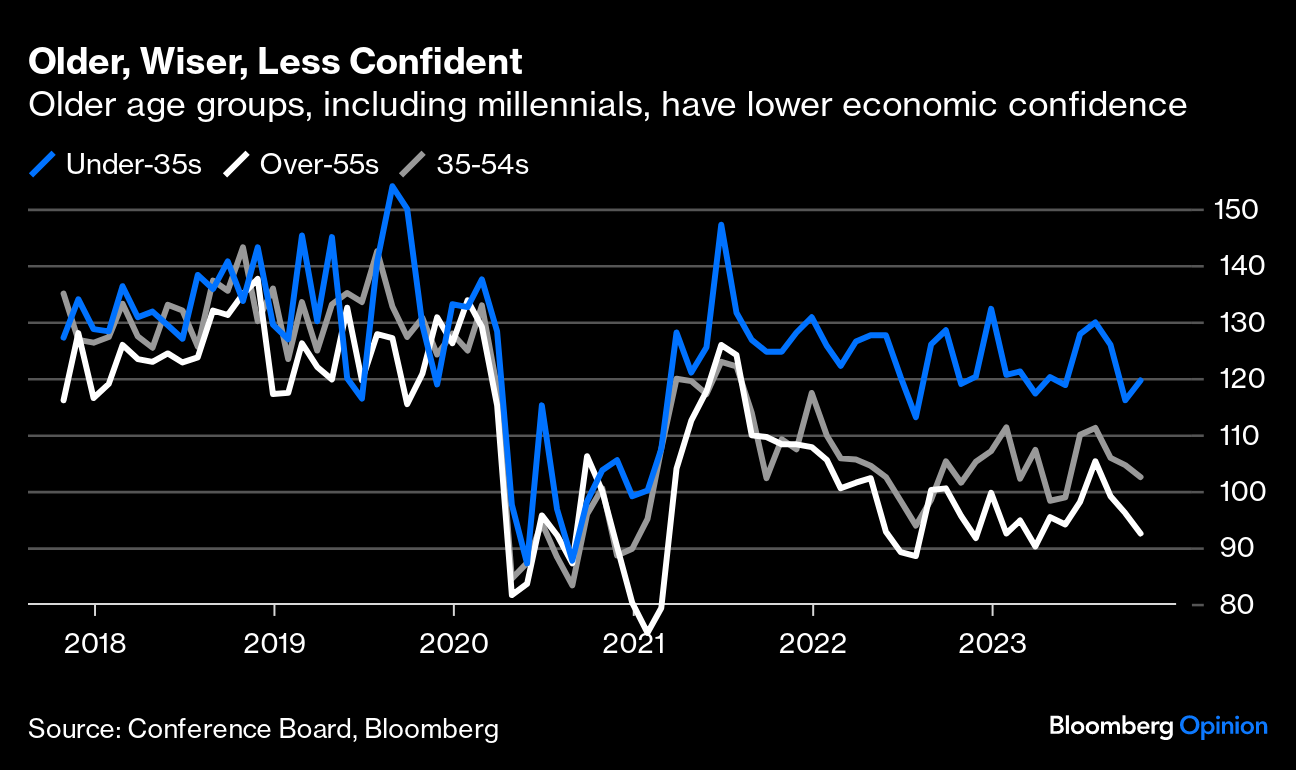

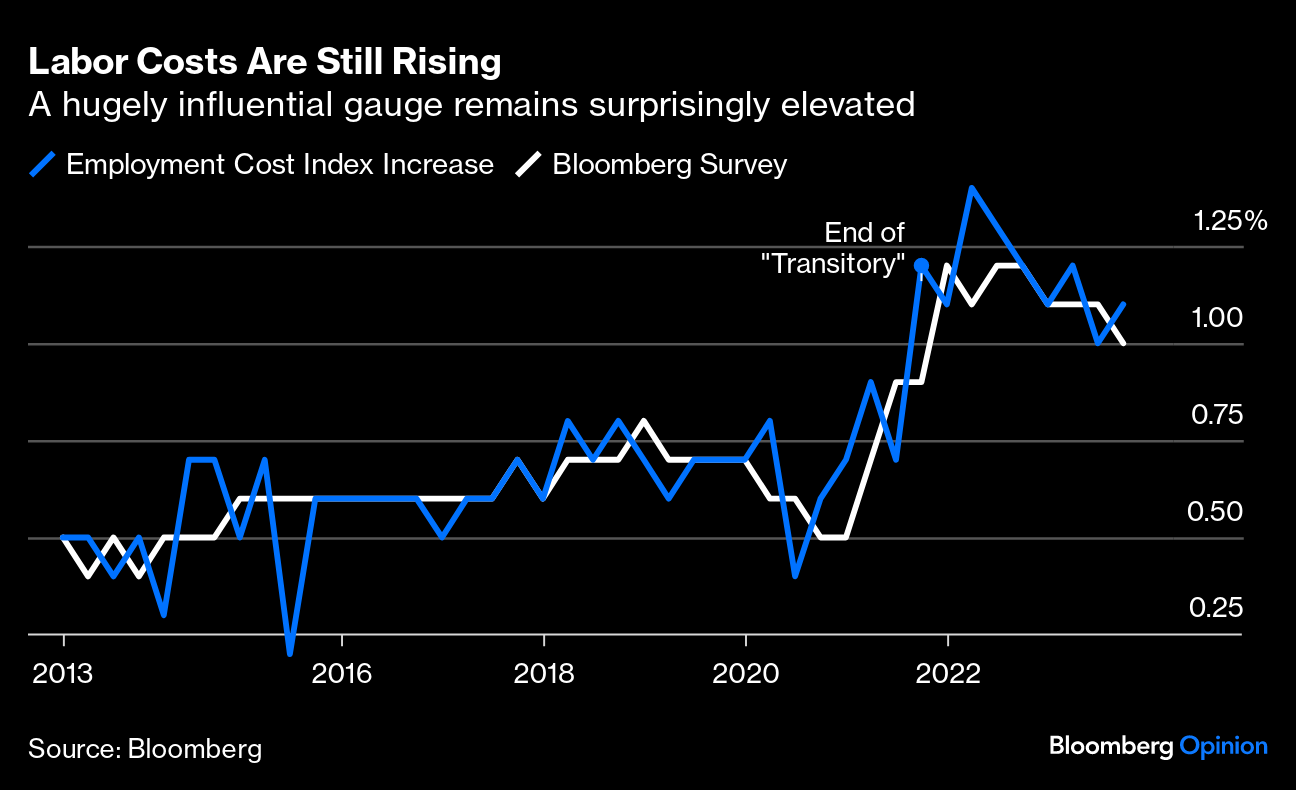

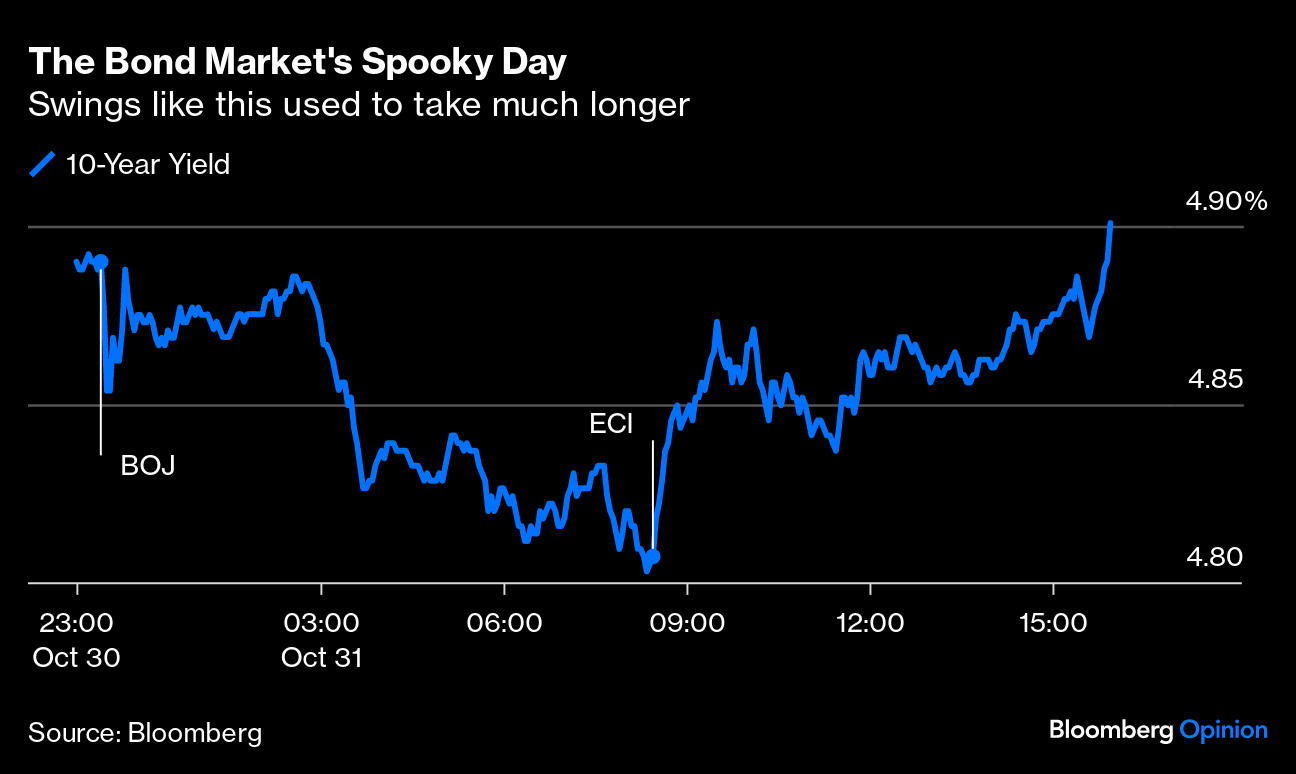

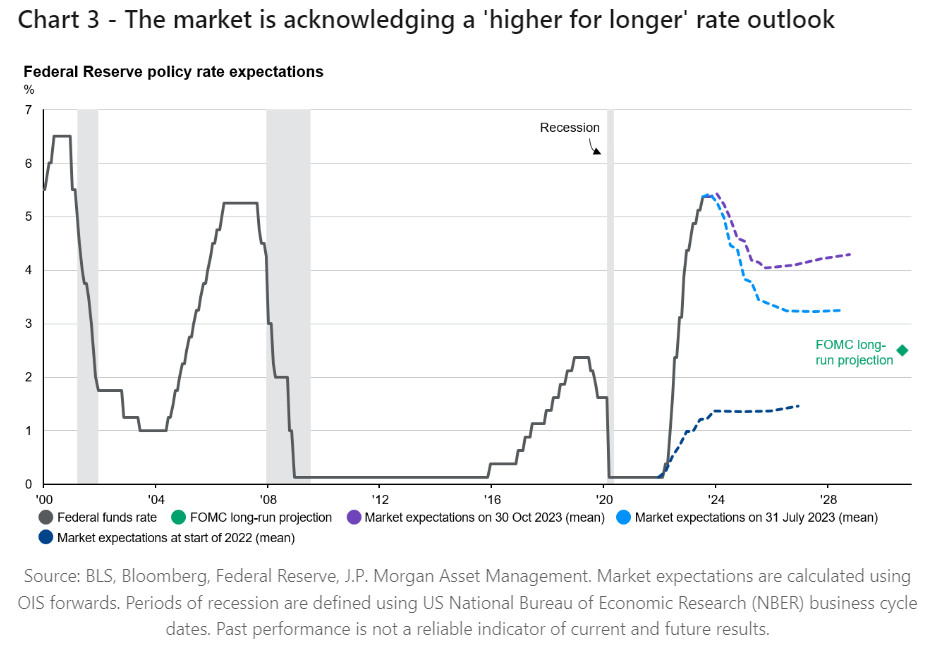

| As the world mops up after this year's night of fancy dress costumes and far too much sugar, it's worth pondering a Halloween landmark for markets. I have otherwise fond memories of Oct. 31, 2007 — I went trick-or-treating with my then three-year-old daughter and her best friend, both of whom were dressed as Dorothy from the Wizard of Oz, which was fun, and the Red Sox had just won their second World Series of the century. Back in the financial world which I inhabited during my working days, however, it turned out to be a landmark. World markets peaked at Halloween 2007. They fell the following day, largely on a warning that Citigroup Inc. might have to cut its dividend. We didn't even know the half of it. A financial meltdown that would sweep the planet and a savage bear market lay ahead. But although we now know that crisis as a "global"one, at this point it appears to have excluded the US, at least judging by stock markets. Using MSCI indexes, this is the 16th Halloween in succession that markets outside the US, and particularly the emerging markets, have closed lower than on the witching night in 2007. In the US, however, stocks are almost triple where they were then, and that's helped pull up broad world markets as well. But what a contrast: It's easy to explain this with grand political theories about US superiority, but most of them don't work. Globalization should have helped everyone. Other economies have grown far faster, and not just China. And in any case, the perception in the US is that the country has slid behind and entered a slump in those years; how else to explain the fact that nearly half the population has twice voted to make the country "great again?" Looking at valuation, we find that it's been a massive driver. For the seven years leading up to Halloween 2007, non-US stocks steadily outperformed as they eroded the valuation gap. The strength of the US tech sector means that the country's stock market as a whole should command a higher multiple. The extent of that US premium was absurd by 2000, at the top of the dot-com bubble. By Halloween 2007, the rest of the world came as close as it ever would to erasing the premium altogether: So excessive interference by the Federal Reserve, buying bonds to create demand for stocks, might have helped the US to take off while the rest of the world languished. In the process, this would also have stoked the inequality that is now causing so much pain. There is more to it than that. US earnings per share have more than doubled over the last 16 years. For the rest of the world, they're barely changed. That unambiguously implies that US companies must be doing something right. But it's also remarkable that they've done this when many other economies have been growing faster: Virtually all the narratives that might explain this are discomfiting. They fall into the left-wing school — that holds that US companies have been allowed to merge, jack up margins and exploit workers, thus making profits while the population is miserable — and the libertarian or Austrian school, which would hold that endemic interference with markets has led to malinvestment, moral hazard, and a bubble that must soon blow up. These ideas aren't mutually exclusive. And both have to incorporate the undeniable fact that a group of companies that all happen to be based in the US have managed to make a lot more money by selling people things that they want since 2007. The Magnificent Seven big tech companies undoubtedly explain some of this difference. But when you think about how these charts might look in another dozen Halloweens from now, it's hard not to be spooked. Now that it's happened, the US collapse after the dot-com bubble burst seems to have been inevitable. Whatever happens to the US stock market in the years ahead, it's hard to avoid the feeling that we should be able to see it coming. And surely a regime of treats for Americans and tricks for everyone else can't endure much longer. There's a lot of over-generalization when it comes to demographics, but sometimes the numbers don't lie and there can even be truths in stereotypes. Case in point: Millennials are embracing bond ETFs to a greater degree than other generations, as muscle memory from the several recessions they have already lived through kicks in. The latest study by Schwab Asset Management shows that ETF investors born from roughly 1981 to 1996 have 45% of their portfolios in fixed income. Those are millennials, aged from 27 years old to 42. That compares to 37% for Generation X — those born from around 1965 to 1980 — and 31% for baby boomers. And it goes exactly in the opposite direction from conventional wisdom, enshrined in the "target date funds" that form the backbone of retirement products, which holds you should increase your bond holdings as you grow older, and that millennials should still be heavily concentrated in equities. David Botset, Schwab AM's head of equity product management and innovation, chalks it up to conservatism, especially after millennials have witnessed repeated market turmoil — from the Global Financial Crisis to the pandemic onset. "Consider the market cycles they experienced growing up," said Botset. "It makes sense against this backdrop that millennials are drawn to fixed income – particularly at a time when yields are the highest they've been in a decade." In general, interest in fixed-income is rising, with 51% of millennials planning to invest in bond ETFs next year, versus 45% of their Gen-X counterparts and 40% of baby boomers, the survey — conducted in June and polling 2,200 investors aged from 25 to 75 — showed. The wild Treasury swings in past weeks raised the payments to be generated from fixed-income, and ETFs are increasingly a vehicle of choice. "The really exciting thing is because they are generally in their 30s and 40s, they have money to invest," Salim Ramji, global head of iShares and index investments at BlackRock Inc., told Katie Greifeld during Bloomberg Indices' Future of Fixed Income conference in New York last week. Millennials are "effectively defaulting into ETFs as their choice for how to invest in markets." Another data point sheds further light on this behavior. US consumer confidence dropped to a five-month low in October, with the Conference Board's index falling to 102.6 from an upwardly revised 104.3 in September. "Consumers continued to be preoccupied with rising prices in general, and for grocery and gasoline prices in particular," Dana Peterson, chief economist, said in a statement. "Consumers also expressed concerns about the political situation and higher interest rates." Delving deeper, the graph below dissects the age range of participants, including those under 35, those 35 to 54, and those older than 55. The pattern is clear: Confidence is still below pre-pandemic levels but the decline is more evident across householders 35 years and up and, as Peterson pointed out, not limited to any one income group. Overall, people are more cautious as the economy adjusts to high-for-longer rates. That means greater demand for bonds than the data might suggest. "There has been a stark divergence between hard and soft economic data for much of this year," Eliza Winger of Bloomberg Economics wrote in a note. "Consumer sentiment remains depressed even as recent hard data have surprised to the upside. Consumers are concerned about a potential recession, with their families' expected financial situation six months hence continuing to fall, boding poorly for future demand." What could matter most, however, is the continuation of demand to buy bonds. With central banks trying to withdraw, bond bulls have been looking to identify new buyers. Millennials might just be the ones. — Isabelle Lee Labor in the US isn't getting any cheaper. This is not just the doing of the Union of Auto Workers, although their success in getting a radically improved pay settlement out of Detroit's "Big Three" carmakers certainly feeds into the zeitgeist. On its own, it's great news if people are being paid more. It improves their living standards, and creates more jobs for others. The issue, of course, is whether workers' extra expenditures will drive inflation. That's altogether tougher to answer. The problem with labor data, as with so much else, is that the best and most reliable numbers are the ones that take the longest to prepare. So, Tuesday's publication of the employment cost index for the third quarter, which ended a month ago, is probably more meaningful than the welter of jobs statistics to come during the rest of this week — but it might not have that much market impact. The ECI matters to the Fed because of its completeness; it incorporates benefits and bonuses to get a better picture of how much workers cost their employers and in turn gives a good idea of how much inflation pressure they are creating. The gauge found that labor costs increased 1.1% in the third quarter compared to the second. That was higher than expected and brought back unpleasant memories of the ECI announcement for the same quarter of 2021, which came as a major shock and was primarily responsible for shaking the Fed out of its belief that inflation was transitory: The muscle memory of that incident remains strong enough that the ECI publication prompted a sharp increase in 10-year bond yields. On the verge of dropping below 4.8% just before the release, they rose in short order and by the end of the day had risen to 4.9% instead: If there were hopes of a pleasant surprise that would allow the Fed to be dovish, they were dashed. But these numbers could still have been much worse. Anna Wong of Bloomberg Economics said the pickup would likely be matched by strong productivity growth for the quarter. "That means policymakers won't be overly alarmed by the ECI print," she said. "Still, upward surprises like this are unwelcome at the Fed, which is unlikely to take the rate-hike option off the table in the near term." Weekly claims data are the most up-to-date and could be the most important. Initial claims for jobless insurance continue to fall, implying that layoffs are reducing despite the tightening financial conditions. But continuing claims are rising, suggesting those out of work are finding it harder to get a new job. Much rests on how this resolves: Apart from Thursday's claims numbers, the remainder of the week will bring data on vacancies and quits in the so-called JOLTS numbers, projected private-sector payrolls from the ADP payroll management group, and then the monthly blunderbuss non-farm payrolls report for October. If these all point strongly in one direction, they might begin to change the calculus for the Fed. And as the central bank is now data-dependent, all of this might even matter more than what Jerome Powell says and does Wednesday. For this week, however, the more or less universal market judgment is that the latest data isn't hot enough to force the Fed into hiking rates — but also wage growth is still too sticky for Powell and his colleagues to take the option of further tightening off the table. In other words, it leaves "high for longer," if not "higher for longer," as the most plausible scenario. That is increasingly accepted, following a swift change of opinion in the last three months. This chart from Karen Ward, chief market strategist for EMEA at JPMorgan Asset Management, demonstrates how quickly this has taken hold: Note that the market, on Ward's calculations, is implicitly expecting the fed funds rate to be higher than the Fed's target long-term projection into 2026. It might be more vulnerable to a surprisingly fast easing cycle than to renewed tightening. But that's all to look forward to. Yesterday, I linked to Metallica performing with former members of Lynyrd Skynyrd. Metallica isn't normally my kind of thing, although they're undeniably great in concert, but I greatly respect how they go out of their way to play with older musicians and introduce them to a new audience. In particular, I love that they've made friends with one of my personal heroes, Ray Davies of the Kinks, who was also a local hero from my years living in Crouch End, North London. The Kinks, from neighboring Muswell Hill, played their first gig there, as shown in this great BBC documentary about him. Davies was obviously enthused to work with Metallica. Here they are playing All Day and All of the Night with him on stage. The exercise does tend to confirm the contention that the Kinks — not any of the other more obvious candidates who followed them — were the true godfathers for heavy metal. Davies and his brother Dave also wrote a fantastic catalogue of songs for others to cover; try All Day and All of the Night by The Stranglers and Van Halen (who also had an early hit with You Really Got Me), Days by Kirstie McColl, David Watts by The Jam, Stop Your Sobbing by the Pretenders, Autumn Almanac by Novelty Island, Sunny Afternoon by Jimmy Buffett, and Lola by Madness and Robbie Williams. "Waterloo Sunset" has been done by everyone from David Bowie, Def Leppard, Damon Albarn (who performed it with Davies himself), and Cathy Dennis. Have a listen.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment