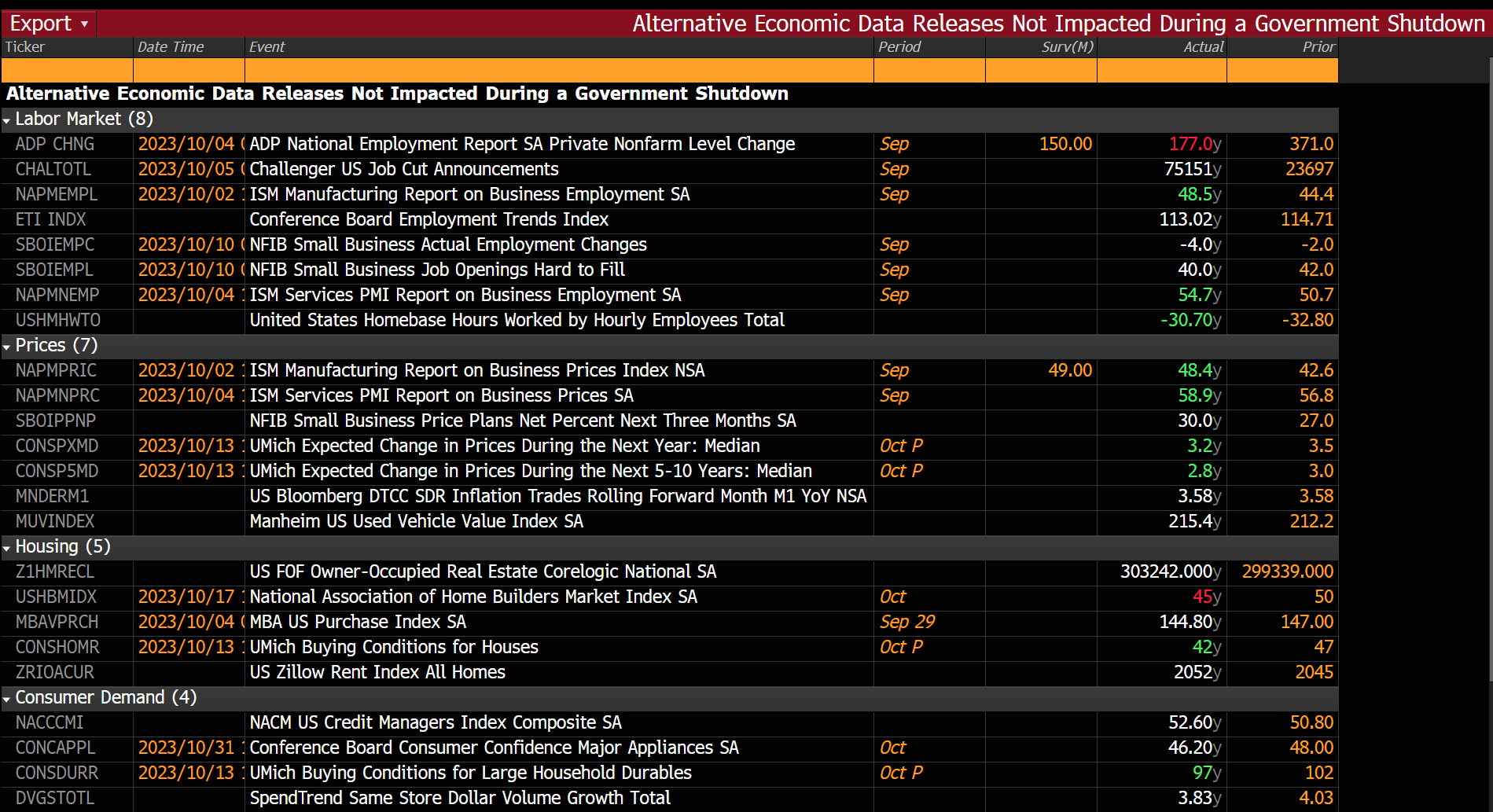

| Good morning. Why the US may not escape recession, President Joe Biden calls for Ukraine funding and investors brace for a crash in office real estate. Here's what's moving markets. — Kristine Aquino A US recession could still be on the horizon, according to Bloomberg Economics. A major auto strike, the resumption of student-loan repayments, and a shutdown that may yet come back after the stop-gap spending deal lapses could easily shave a percentage point off GDP growth in the fourth quarter, economists Anna Wong and Tom Orlik write. Those risks come just as the full force of the Federal Reserve's rate increases are set to hit at the end of this year or early 2024. That said, optimists are pointing to a potential fresh surge in productivity and President Biden's embrace of industrial policy among factors that could sustain growth and help the US avert a severe economic downturn. President Biden urged House Speaker Kevin McCarthy to follow up quickly with funding for Ukraine hours after Congress passed a spending bill to avoid a US government shutdown, but did not include $6 billion in aid. Less than two weeks ago, Ukrainian President Volodymyr Zelenskiy visited Washington to plead for new weapons systems and urged allies to keep up their financial and military support for Kyiv. "There's an overwhelming number of Republicans and Democrats in both the House and the Senate who support Ukraine. Let's vote on it," Biden said Sunday at the White House. Office prices in the US will only rebound after a severe collapse, according to about two-thirds of the 919 respondents surveyed by Bloomberg. An even greater majority says that US commercial real estate prices won't hit bottom until the second half of 2024 or later. Commercial property values are getting hit hard by the Fed's aggressive rate hikes, and pain from higher interest rates can take years to filter through to owners of the US commercial real estate, which Morgan Stanley values at $11 trillion in total. "It tends to be a slow reckoning for US real estate when rates change," Barclays analyst Lea Overby said. S&P 500 futures climbed 0.3% as of 5:42 a.m. in New York, while Nasdaq 100 futures advanced 0.5%. Treasury yields climbed across the curve, with the 10-year yield approaching a 16-year high seen on Friday. The US dollar rose against most Group-of-10 currencies. Brent crude traded around $92, Gold fell and Bitcoin gained for a third-straight day. At 9:45 a.m., we'll get get the latest reading for S&P Global's US manufacturing gauge, followed by the most recent figures for ISM's measure 15 minutes later. At the same time, the US will publish figures on August construction spending. Fed Chair Jerome Powell and Philadelphia Fed President Patrick Harker participate in a roundtable discussion at 11 a.m. New York Fed President John Williams moderates a climate risk discussion at 1:30 p.m., while Cleveland Fed President Loretta Mester speaks on the economic outlook at 7:30 p.m. This is what's caught our eye over the weekend: Originally I planned to write today's section of the newsletter about how to track the economy in the event of a government shutdown, by monitoring all of the published private sector data -- like LinkedIn job postings. This may still be a useful exercise at some point, since the government might shut down later this year.

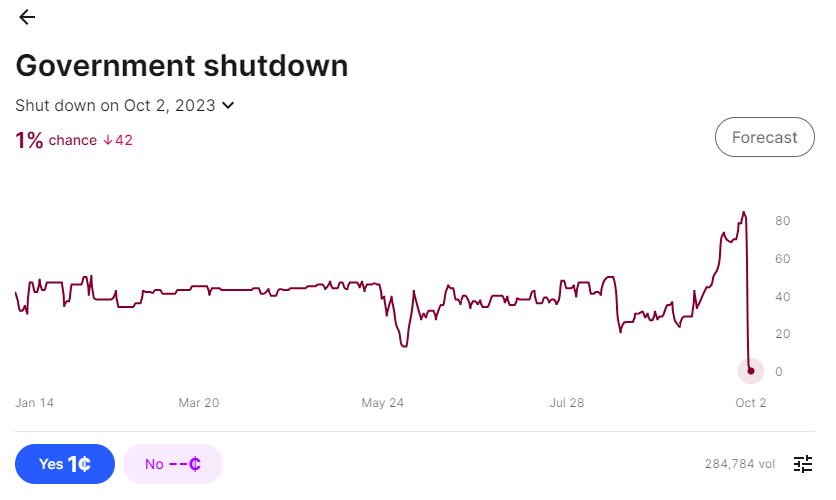

In fact, my colleague Mike McDonough put together a calendar on The Terminal which you can find in the Economics section of {WSL <GO>} to see private sector data as it comes out. But for the moment, that scenario has been averted, catching almost everyone by surprise this past weekend. In fact, you can nicely see the surprise by looking at the betting market on Kalshi for a government shutdown. At one point, traders had priced the odds of the government shutting down by today at nearly 90%. At then it reversed instantly. It was never entirely clear that the risk of a shutdown was moving markets. So it's not clear that the surprise turn will cause some impact in the other direction. Anyway. In the absence of that, I figured I would use this space to just list a few random, big picture things I'm thinking about these days, that interest me. Here they are in no particular order.

- The soft landing debate. Yes, everyone's wondering about it and so am I. Speaking of which, on the new Odd Lots, Richmond Fed President Tom Barking talks about business behavior, and why firms are still concerned with about being caught short on labor. - Mortgage rates. The 30-year fixed was briefly over 7.8% last week. It's up basically a whole percentage point over the last year. When does this start to be a big political issue? Historically speaking, there have been periods where the government expressly tried to bring interest rates down, through fiscal consolidation and a tacit coordination with the Fed. It doesn't seem like we're anywhere close to that happening right now. But could we get there at some point? - Deficits in general. High deficits and rising interest expense (thanks to the rate hikes) is a macro dynamic that's getting more and more attention, with ambiguous consequences. - Chinese tech exports. Lots of people are talking about China's EV prowess these days. But the story goes beyond just EVs. China's domestic jet maker Comac just got its biggest order ever. And it increasingly looks like China's Huawei is catching up in ways to Apple using homegrown tech for its parts. Yes obviously the country has undesirable macro dynamics right now with the real estate bust etc. But by all accounts in continues to make progress at the cutting edge of tech. - Speaking of EVs, there's obviously a lot of anxiety about whether the legacy US automakers will thrive in this environment. And then add in the labor dynamics (the strike's still ongoing) and the concerns seem more acute. - More to this point, it seems as though there's a high degree of pessimism right now towards the current wave of domestic industrial investment. Given the strike and the level of rates, the mood seems to be of one that the country is spending a ton of money and won't get productive output from it. That's been the vibe, anyway, of late. Whether that's fair is a totally different question. - Speaking of the vibes, we're coming into a jam packed calendar from elections from now until late next year. Not just the US obviously, but India, Brazil, South Africa, Indonesia, Poland, Korea, Mexico are all coming up. People with "Geopolitical Risk Expert" in their title will probably have a busy year. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart Like Bloomberg's Five Things? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. |

No comments:

Post a Comment