| Good morning. Aid to Ukraine, the UK and French stock markets, and Bill Ackman's possible deal with Elon Musk's X Corp. Here's what people are talking about. Hours after Congress passed a US spending bill without additional funding for Ukraine — in order to avoid a government shutdown — President Joe Biden urged House Speaker Kevin McCarthy to follow up quickly with support. "I fully expect the speaker to keep his commitment to secure passage and support needed to help Ukraine as they defend themselves against aggression and brutality," Biden said Sunday at the White House. Meanwhile, a former prime minister who's derided the European Union's sanctions against Russia and pledged to end military aid to Ukraine, won Slovakia's election, delivering a fresh blow to Western unity. Britain's stock market is getting back on its feet. Less than a year after losing the crown of Europe's biggest equity market, London looks set to recapture it from Paris, as the rally in French luxury shares falters. The combined dollar-based market capitalization of primary British listings now stands at $2.90 trillion versus France's $2.93 trillion, according to an index compiled by Bloomberg. The gap between the two has narrowed steadily, primarily driven by a slide in France's value from last year's $3.5 trillion record as economic gloom in the key Chinese market deepens. Billionaire Bill Ackman would be interested in pursuing a deal with Elon Musk-owned X Corp. as part of a new investment vehicle, the Wall Street Journal reported. Pershing Square received regulatory approval on Friday for a new investment vehicle that targets private companies seeking to raise $1.5 billion or more, and potentially take them public. The product is a new class of special purpose acquisition companies known as SPARC, where investors buy into the company after a purchase target is identified. Representatives for Pershing Square and X didn't immediately respond to requests for comment from Bloomberg on Sunday. From the US to Germany to Japan, yields that were almost unthinkable at the start of 2023 are now within reach. The selloff has been so extreme it's forced bullish investors to capitulate and Wall Street banks to tear up their

forecasts. The question now is how much higher they can go, with no real top in sight after key levels were broken. While some argue the moves have already gone too far, others are calling it the new normal, a return to the world that prevailed before the era of central bank easy money distorted markets with trillions of dollars of bond buying. European stocks are on track for gains in the first trading day of the new quarter. UK nationwide house prices are due. Sweden's Riksbank monetary-policy minutes will be released, as do euro-zone manufacturing PMIs and unemployment data. ECB governing council members Mário Centeno and Pablo Hernandez de Cos speak, as does Bank of England policy-maker Catherine Mann. This is what's caught our eye over the past 24 hours European stocks received some relief on Friday that may be tricky to sustain heading into 4Q with cyclicals underperforming.

Some of this month's most battered sectors -- such as real estate, tech and consumer goods -- were helped by a rebound in bonds while luxury benefitted from a Bank of America upgrade. Still, European stocks have undergone a shift into value sectors such as energy (amid gains in commodities) and more defensive stocks.

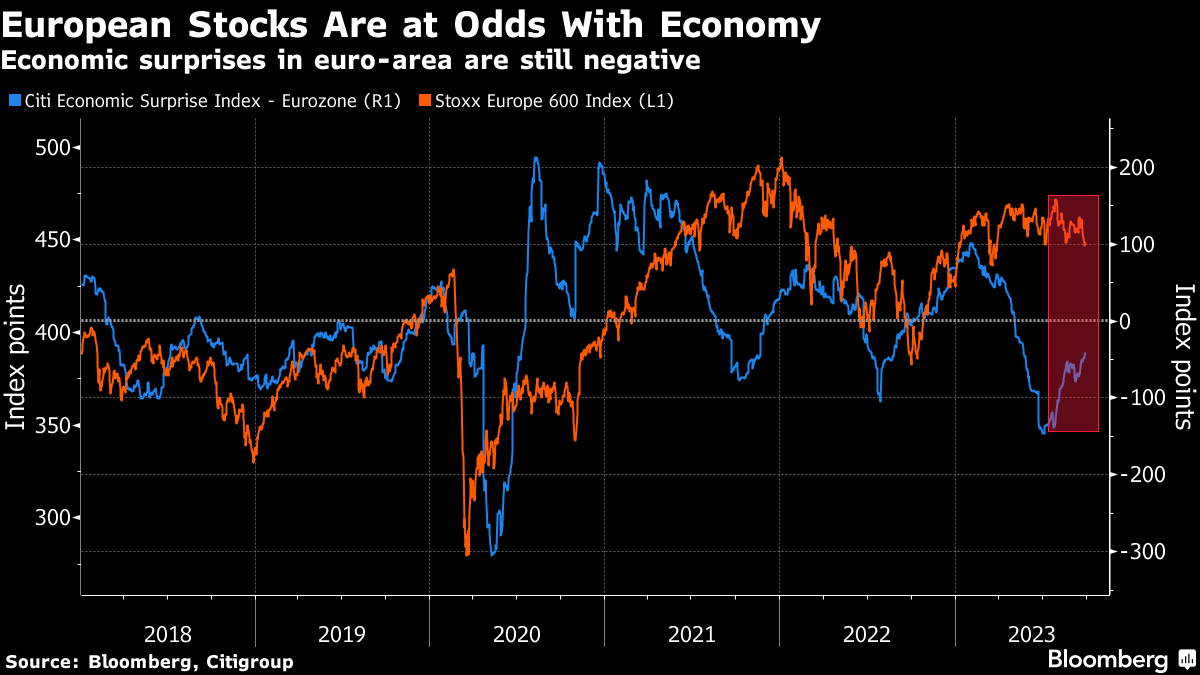

While 4Q is typically the best for the Stoxx 600, two big headwinds can continue to weigh. First is the deteriorating macro backdrop, which equities have largely ignored this year.

That perhaps has started to change, with the cyclically-tilted DAX the worst-performing major Western European benchmark in September. The German economy is set to shrink 0.6% this year and euro-area economic confidence continues to drop. China weakness can also continue to pressure cyclical sectors.

Secondly, higher-for-longer rates are making bond yields an attractive alternative to stocks. On Friday stocks got some balm from slowing euro-area inflation. But the ECB is likely to stay tight and rising oil prices could re-stoke inflation, feeding back into the weak economic narrative. Higher real yields can keep pressuring sectors like luxury and tech.

The upcoming 3Q earnings season will be a test, with a wave of downgrades possible as companies price in a slower backdrop. Still, reasonably-robust results would bring needed relief and support valuations. Consumer optimism will be tested in next week's set of reports.

Heather Burke is an editor in the Markets Live team for Bloomberg News, based in London. |

No comments:

Post a Comment