| Welcome to The Weekly Fix, the newsletter that's never been downgraded. I'm cross-asset reporter Katie Greifeld. Fitch Ratings' surprise move to strip US government debt of its top-tier rating this week sparked passionate criticism from Washington and Wall Street alike, with Treasury Secretary Janet Yellen deriding the downgrade as "arbitrary." But to David Beers, former head of S&P Global Ratings' sovereign debt scoring committee and one of the analysts behind the controversial ratings cut in 2011, it's an important reminder that the US isn't entitled to the top grade. "The underlying fiscal position and underlying debt trajectory has picked up pace," Beers, who is now a senior fellow at the Center For Financial Stability, told Romaine Bostick and I on Bloomberg Television. "AAA is the top rating any rating agency can assign, but of course, the US and any other sovereign that's being rated has no god-given or automatic right to that." Fitch's move comes nearly 12 years to the day since S&P shocked markets by dropping the US one level to AA+ from AAA for the first time in history, a move helmed by Beers and John Chambers. Their reasoning more than a decade ago sounded startlingly similar to Fitch's logic this week: ballooning US deficits and political dysfunction. Though May's debt-ceiling drama ended with an as-expected last-minute deal, repeated debt-limit clashes and eleventh-hour resolutions have eroded confidence in the nation's fiscal management. For Beers, it's a bit of a victory lap. S&P has yet to reverse the downgrade, and many of the issues flagged by the rating firm back in 2011 have only escalated since. If anything, other agencies have been a bit meek, he said. "It's fair to say that the rating agencies, based on their own criteria, have been pretty timid in their actions," he said. "If anything, Fitch's action is simply confirming what S&P decided back in 2011, and here we are in 2023." For all the drama around the US downgrade, it was largely business as usual for bond investors. That includes Warren Buffett, who told CNBC on Thursday that the "only question" is whether Berkshire Hathaway is going to buy another $10 billion of 3- or 6-month Treasury bills next week. "There are some things people shouldn't worry about," Berkshire Hathaway chairman and chief executive Buffett said. "This is one." Buffett's comments came hours after Pershing Square Capital Management Founder Bill Ackman said he is short 30-year Treasuries "in size" — a position that doubles as a hedge against the impact of higher long-term rates on the stock market and a standalone bet. As an extremely online person, I pointed that fact out on X, the social media platform formerly named Twitter — Buffett is big on bills, while Ackman is shorting duration — with the unfortunate quip "Buffett vs Ackman." Imagine my surprise when Ackman replied, pointing out that Pershing Square also uses short-dated US paper for cash management purposes: "We actually agree. Buffett would never buy 30-year Treasurys at anywhere near current yields. His purchases are just cash management using short-term T-bills. We also invest our cash in short term Treasurys."

Very fair! And an important nuance missing from my original post. But the day only got stranger when Tesla Inc. chief executive and current X owner Elon Musk weighed in with his thoughts on the shortest end of the Treasury curve: "Yeah, short term T-bills are a no-brainer."

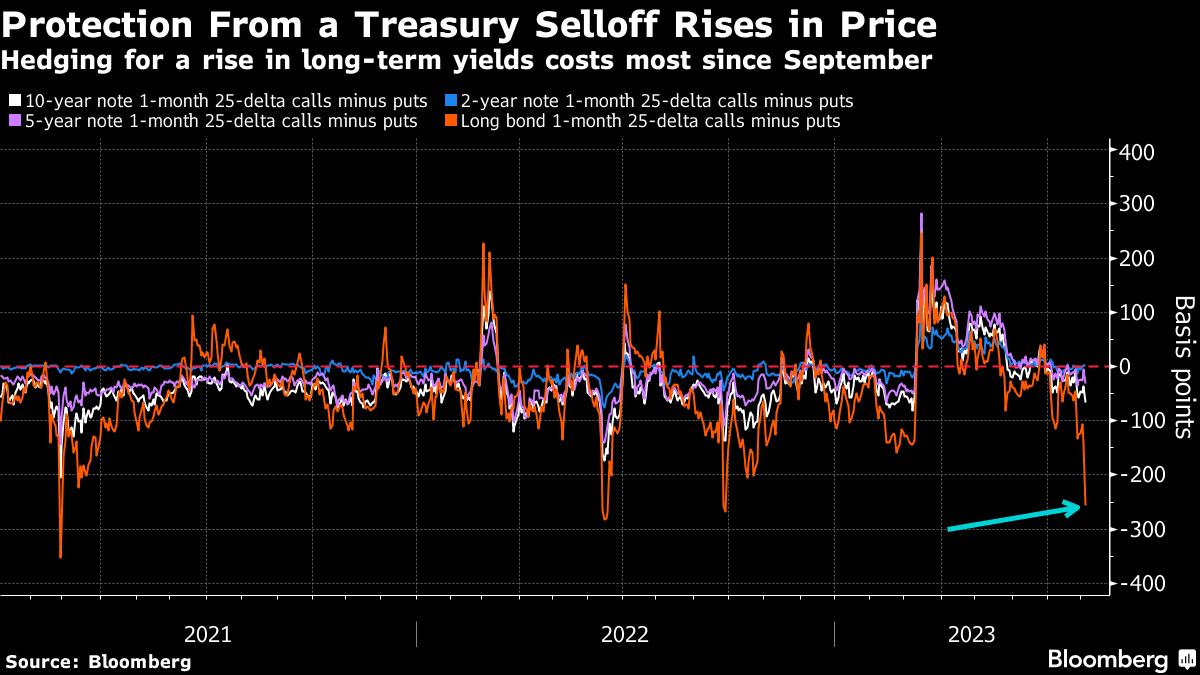

While a sample size of three isn't huge, it's probably safe to say that the shock US downgrade this week hasn't scared the billionaire set away from T-bills — or average investors, for that matter. In fact, assets in money-market funds climbed to a fresh record this week of $5.52 trillion, according to data Thursday from the Investment Company Institute. The roughly $29 billion influx was driven primarily by cash moving into government funds, where short-dated paper is yielding north of 5%. In any case, I tried to get Musk's opinion on debt further out the curve. No answer yet. But while cash is hot, the long-end of the Treasury curve has gotten absolutely hammered this week. Long-duration Treasuries are on track for their worst week of 2023, with yields on 30-year bonds rocketing nearly 25 basis points higher this week to about 4.26% — the loftiest levels since November. It's a similar story for benchmark 10-year notes, which have climbed more than 20 basis points this week. That's good news for Ackman's "in size" short bet against 30-year bonds, and for the likes of Bill Gross as well. The former chief investment officer of Pacific Investment Management Co. took to X to say that he is "overall bearish" on 10-year Treasuries, and that the yield curve may disinvert from the benchmark yield's ascent. We're still a long ways away from positive territory, but the yield curve re-steepening at the hands of the long-bond selloff this week is staggering. The spread between 2-year and 10-year yields is currently negative 73 basis points, versus the negative 105 basis points just last week. Meanwhile, bond traders are budgeting for further pain at the long-end of the curve. Judging by interest-rate options, investors are paying up in a big way for another leg higher in long-dated yields. As reported by Bloomberg's Edward Bolingbroke, a metric that compares demand for bearish put options to demand for bullish call options shows the widest divergence since September for options on CME Group Inc.'s US Treasury Bond Futures contract, which currently tracks a bond that matures in 2039. The gaps are less extreme for options on shorter maturities. While it had just started to feel like long-duration was the consensus trade, there's plenty of reasons to be bracing for higher yields right now. Among them: the US economy is resilient and then some, an eventual Bank of Japan exit from extraordinary easing could mute an important source of bond demand, and the Treasury's decision to boost auction sizes by more than expected means that a wave of supply is about to hit the bond market. In addition to heated criticism, Fitch's downgrade also sparked some awkward questions in the credit market. Specifically, what to make of the US companies that now have a higher rating than their home country? It's an exclusive club, for sure, populated by the likes of Microsoft Corp. and Johnson & Johnson. But that special group could see their spreads tighten further, and benefit from the downgrade in the sense that investors might replace sovereign bonds with those of highly rated companies, as some did during Europe's sovereign debt crisis, according to Citigroup Inc.'s head of global debt capital markets. "The bad news is it is a very small group of companies that have ratings at or above the current sovereign rate for the US government," Richard Zogheb said on Bloomberg Television Wednesday. "There is only so much of your portfolio that you can replace of sovereigns into these multinational, highly-rated areas." It's unclear whether the US downgrade will spark any cascade of corporate downgrades, as is often seen in emerging markets. But in the US municipal bond market, that daisy-chain has already started. In an expected move Thursday, Fitch downgraded billions of dollars worth of public finance credits linked to the rating company's US downgrade. For example, that includes $21.5 billion of the federally-owned Tennessee Valley Authority's global power bonds. "In terms of like the immediate impact on credit, anything that's tied to the US government rating will have to come down," said Lisa Washburn, a managing director for Municipal Market Analytics. "It raises the broader question of how do you think of other municipal credit?" - Trump pleads not guilty to charges of obstructing election

- Cockpit photos show near-collision between JetBlue, charter jets

- Credit Suisse collapsed, and Switzerland went back to making money

|

No comments:

Post a Comment