| Diversification et gestion de portefeuille.

Lettre n°28 — Mercredi 2 Août

Cher lecteur, chère lectrice,Je suis heureux de te retrouver au beau milieu de l'été pour une nouvelle édition de ma lettre hebdomadaire. À l'honneur, Richard Garnier, analyste financier en Suisse et auteur de 2 livres dont un ouvrage sur la diversification, intitulé "De la Bourse au Bitcoin".

Dans son article, il te montrera comment l'association de plusieurs actifs risqués peut permettre de réduire significativement le risque global d'un portefeuille. Au cas où tu l'aurais manqué, je t'ai repartagé un de mes podcasts préférés, sur l'investissement, le long terme et la diversification, ainsi que mon dernier partenariat. Tu retrouveras ensuite ma revue bi-mensuelle des marchés avec un focus sur une vingtaine d'actions françaises. En clap de fin, j'ai une petite faveur à te demander. Les grandes lignes (10 min de lecture)

🎙️ Réduire son risque de 60 % avec des actifs risqués !

📺 Podcast de vacances

📺 Les marchés en live épisode 11

👉 Besoin de toi Rappel : ajoute-moi à tes contacts pour ne louper aucun mail.

2 nouveaux caps franchis ! 🎉

✅ 8 000 abonnés YouTube dépassés en pleine émission !

✅ 28 000 abonnés sur Instagram ! Un grand merci à chacun d'entre vous 🙏 ⏩ Pour fêter ça, j'ai même franchi un 3ème record avec un ribs de 750g ! Du jamais-vu en 30 ans de carrière... 🥵

Le meme à faire tourner

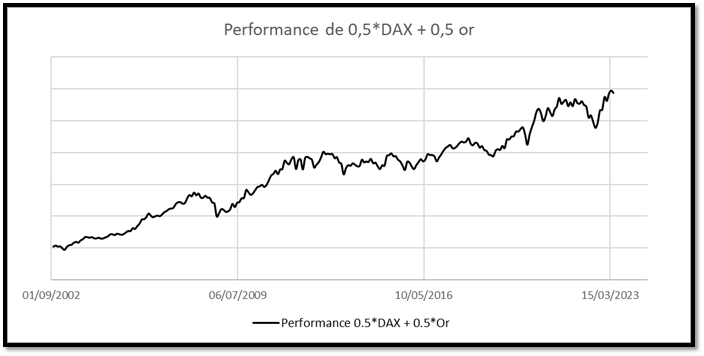

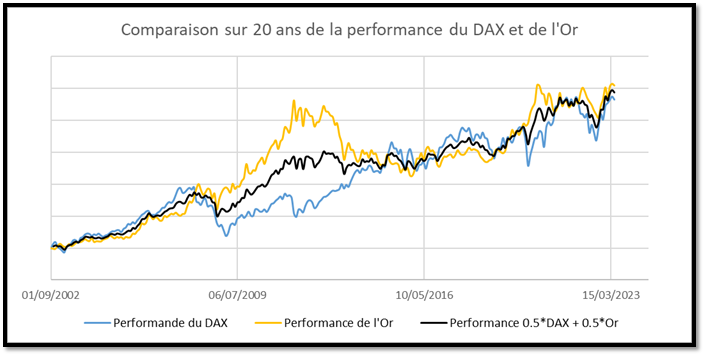

🎙️ Réduire son risque de 60 % avec des actifs risqués !par Richard Garnier Risqué + risqué = risqué ? Logiquement, en investissant en même temps sur deux actifs risqués (par exemple le DAX et l’once d’or), alors on obtient un portefeuille risqué. C’est logique : risqué + risqué = risqué ! Pourtant, dans la pratique, c’est tout à fait l’inverse qui se produit. Explication en 4 images. Le cas du DAX et de l’once d’orVous investissez sur deux actifs risqués en même temps : - le DAX (l’indice boursier Allemand) et

- l’once d’or (le fameux métal jaune)

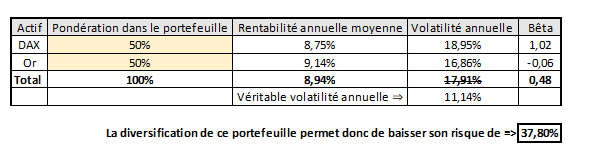

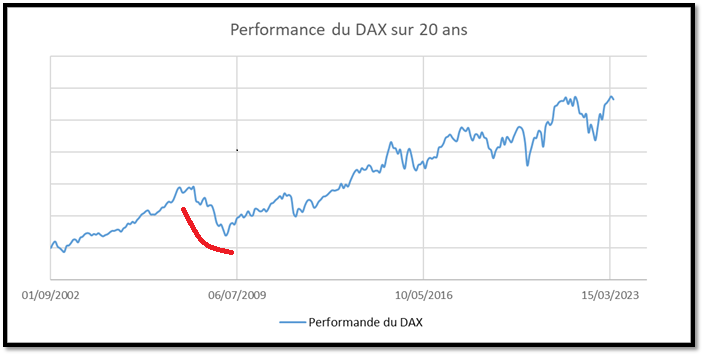

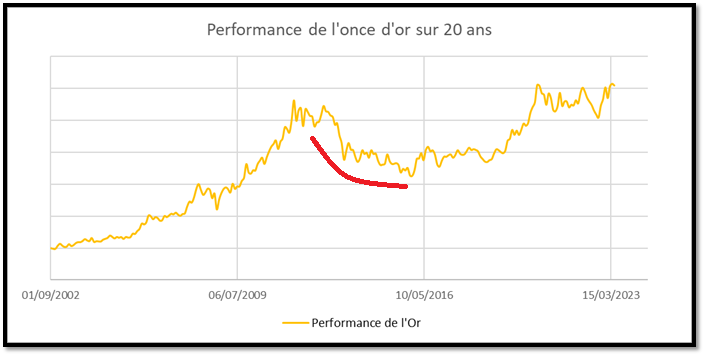

On dit qu’ils sont risqués, car ils peuvent perdre une bonne partie de leur valeur rapidement. Par exemple, le DAX a connu un à-coup pendant la crise des subprimes. Sur un graphique de vingt ans, on voit que le DAX s’est replié en 2008. Plus précisément, il a perdu la moitié de sa valeur entre septembre 2007 et mai 2009. En moyenne le DAX a gagné +8.75 % par an, mais, en 2008, il a connu un krach. Le DAX est donc risqué. L’once d’or, de son côté, a gagné +9.14 % par an en moyenne sur les vingt dernières années, mais l’once d’or n’a pas connu cette performance sans turbulences. Entre septembre 2011 et décembre 2015, le métal précieux a chuté. L’once d’or est donc risquée, elle aussi. 🔍 Le DAX et l’once d’or sont donc deux actifs risqués, Pourtant, en investissant en même temps sur le Dax et l’once d’or, alors nous constatons la chose suivante : ensemble, les deux actifs sont stables comme par magie. Sur un graphique de vingt ans, la performance du portefeuille composé à 50 % du DAX et à 50 % de l’once d’or devient pratiquement une ligne droite. Impressionnant ! Les deux investissements qui sont risqués séparément sont devenus stables ensemble. Et c’est encore plus visible lorsque les trois graphiques sont juxtaposés. Sur 20 ans, quand le DAX a baissé (en 2008 durant la crise des subprimes par exemple), l’once d’or a compensé cette perte avec une forte hausse et quand l’once d’or a baissé (par exemple en 2010) le DAX a compensé cette perte avec une forte hausse : c’est la diversification. Diversification : le calcul ?Vous aurez compris qu’en investissant simultanément sur le DAX et sur l’once d’or, du risque a été supprimé. Face à cette découverte, des financiers se sont demandés quelle quantité exacte de risque avait été supprimée dans la manœuvre. Est-ce qu’en mélangeant du DAX et de l’or 10 % du risque avait été supprimé du portefeuille ? 20 % ? 30 % ? Pour répondre à cette question, il suffit de comparer la volatilité théorique (calculée mathématiquement) d’un portefeuille composé à 50 % de DAX et 50 % d’or avec la véritable volatilité de ce portefeuille (celle constatée sur le graphique au-dessus).  Mathématiquement, en additionnant les performances et les risques du DAX et de l’once d’or, la performance totale de ce portefeuille devrait être de 8.94 % et sa volatilité totale devrait être de 17.91 %. Or, en reconstituant véritablement ce portefeuille, alors nous pouvons constater qu’il a bien une performance de 8.94 %, mais (surprise) il a une volatilité de « seulement » 11,14 %. Plus de 35 % de la volatilité de ce portefeuille a été supprimée par la diversification ! Maitriser la diversification pour supprimer 60 % du risque !Le DAX et l’once d’or est donc une bonne combinaison ! Elle permet de supprimer plus de 35 % du risque. D’une manière générale, l’once d’or permet de stabiliser n’importe quelle combinaison. Le métal jaune est un contrariant naturelle qui joue les amortisseurs dans les périodes de tensions tout en étant aussi un performeur dans les autres périodes. C’est donc un ingrédient primordial dans une stratégie de diversification. Mais la combinaison mélangeant le DAX et l’or n’est pas la meilleure combinaison de diversification. Certaines combinaisons d’actifs permettent de supprimer jusqu’à 60 % du risque d’un portefeuille. Je vous donne quelques pistes pour arriver à ce niveau de diversification. - Avoir de l’or dans son portefeuille.

- Avoir au moins six actifs

- Il est impossible de diversifier un portefeuille avec des actifs cycliques.

- La diversification peut être géographique.

- La diversification demande un certain équilibre des forces.

🎯 En suivant ces règles, la combinaison d’actif suivante supprimerait le risque global de 60 % : Hermès + Air Liquide + Vinci + McDonald’s Corporation + Nike + Or Cette sélection est exposée au secteur du luxe via une marque à la réputation solide, à l’un des leaders de son secteur d’une extrême qualité sur le long terme, aux infrastructures de transports bénéficiant de contrats gouvernementaux, à la célèbre chaine de fast-food connue mondialement, à l’entreprise américaine de vêtements de grande consommation et enfin à la valeur refuge dorée. De cette manière, le risque de ce portefeuille est extrêmement mutualisé. Chaque actif peut connaitre une baisse, mais il est quasi improbable qu’ils connaissent tous une baisse au même moment. Globalement, les baisses temporaires des uns vont être compensées par des hausses temporaires des autres et réciproquement. Globalement, le portefeuille va performer sur du long terme sans connaitre de véritables turbulences. Même si toutes les actions s’effondrent, il restera encore l’or dans ce portefeuille pour jouer les amortisseurs. Il est donc parfaitement diversifié. Vous aurez compris qu’une des règles fondamentales qui offre de la diversification c’est d’avoir de l’or dans son portefeuille, mais tous les investisseurs ne savent pas comment en avoir. Il existe une astuce pour investir facilement dans l’once d’or. Il est possible de mettre de l’or dans son portefeuille via un certificat qui réplique fidèlement, à la hausse comme à la baisse, l’évolution de l’once d’or (aux frais de gestion et à la parité euro/dollar près). Ce certificat peut être retrouver sous le code ISIN NL0006454928 et il s’appelle le « certificat 100% or ». Ce certificat peut même être éligible à l’assurance-vie de cette manière vous combinez diversification et avantage fiscal. N’hésitez pas à demander à votre conseillé s’il propose ce certificat dans votre assurance-vie ! C’est la diversification assurée.

📺 Podcast de vacancesUn de mes podcasts préféré, avec Cédric et Vincent de la chaîne 100 Bornes. Le cadre est original (à bord d'une voiture) et le finish à la Bourse de Paris clôture parfaitement cette interview.

Nous avons discuté : ✅ De mon parcours dans le milieu de la finance,

✅ D'investissement passif,

✅ De la gestion du risque,

✅ Et bien sûr d'automobile (même si je n'ai pas le... 🤫)

Retrouve l’interview complète ci-dessous :

📺 Les marchés en live épisode 11✅ Publications en pagaille

✅ FED et BCE au tournant

✅ Analyses de 20 actions

🤝 La période parfaite pour s'y pencherAu cas où tu n’aurais pas lu ma dernière Newsletter, saches que j’ai signé un nouveau partenariat rémunéré avec Auguste Patrimoine. L’été est la période propice pour faire le bilan de la gestion de ton patrimoine. Un bilan patrimonial est offert en prenant rendez-vous via leur calendrier.

👉 Besoin de toi Afin d'optimiser ma Newsletter j'aimerais te poser 2/3 questions, tu peux répondre directement à ce mail pour me donner ton avis. Qu'apprécies-tu dans mes lettres et qu'aimerais-tu avoir en plus?

As-tu des sujets de prédilections que tu aimerais me voir couvrir? Est-ce qu'une newletter plus longue tous les 15 jours te convient?

Tu souhaites partager cette newsletter à un ami pour qu'il devienne un investisseur averti ?Il peut rejoindre notre communauté de 26 886 investisseurs en cliquant sur le lien juste ici.

✍️ Partenariats rémunérés📣 Tu souhaites débuter un plan d'investissement programmé sans frais, sur une application simple et intuitive ?⏩ Ouvre un compte chez Trade Republic. 🎁 Un cadeau de bienvenue est offert en passant via mon lien et avec le code promo NICOLAS30 🎁 Tu souhaites trader via les graphiques avec des outils professionnels ?⏩ Jette un œil sur les offres de ProRealTime. Tu souhaites un bilan patrimonial complet et gratuit avec un professionnel ?⏩ Réserve un rendez-vous chez Auguste Patrimoine. Communication à caractère promotionnelTu souhaites utiliser et découvrir les produits de bourse que je traite ?⏩ Je t'invite à découvrir les produits Citi. Produits à effet de levier présentant un risque de perte en capital en cours de vie et à l’échéance

Nicolas ChéronAnalyste et vulgarisateur boursier

Citi rémunère financièrement Nicolas Cheron pour la mention publicitaire de ses produits, toutefois Citi ne participe à aucun moment à la sélection d’un produit spécifique. Produits à effet de levier présentant un risque de perte en capital en cours de vie et à l’échéance Les produits CitiFirst sont des produits complexes qui peuvent être difficiles à comprendre. Ils s’adressent uniquement à des investisseurs avertis, professionnels ou non professionnels, disposant de connaissances suffisantes des spécificités de ces produits. Les facteurs de risques sont notamment : - Risque de perte du capital : Les produits CitiFirst peuvent perdre tout ou partie de leur valeur notamment en raison d'une perte de valeur temps des Warrants, de désactivation des Turbos ou de franchissement de la Borne Basse des Certificats Bonus Cappés.

- Risque lié à l’effet de levier : En raison de leur effet de levier à la hausse comme à la baisse, ce qui peut être favorable ou défavorable à l’investisseur, les produits CitiFirst peuvent connaître de grandes variations, voire perdre tout ou partie de leur valeur.

- Risque de marché : Les produits CitiFirst peuvent connaître à tout moment d’importantes fluctuations de cours, pouvant aboutir à la perte totale ou partielle du montant investi.

- Risque de crédit : L’insolvabilité de l’émetteur peut entraîner la perte totale ou partielle du montant investi.

- Risque de désactivation : La désactivation engendre un risque de perte totale et définitive du capital investi. Sur les Turbos Infinis et Infinis BEST l’ajustement du prix d'exercice et de la barrière désactivante accroit le risque de perte partielle ou totale en capital.

- Risque de liquidité : L’absence totale ou partielle de liquidité peut entrainer une perte totale ou partielle en capital.

- Risque lié au sous-jacent : Lors de la reconduction du contrat Future Brent, l’ajustement de la barrière de désactivation s’accompagne d’un changement de sous-jacent vers le contrat d’échéance suivante. Les Turbos sur actions US, devises et matières premières ont des horaires/jours de désactivation spécifiques figurant sur le site fr.citifirst.com. Sur une période de plusieurs jours, la performance de l'indice à levier des Leverage & Short peut être inférieure à la performance des composants de l’indice multipliée par le levier, ce qui peut ne pas être adapté à un investissement à long terme.

Les investisseurs sont invités à prendre connaissance des facteurs de risques énoncés dans les prospectus de base, disponibles gratuitement sur la page fr.citifirst.com/FR/Documentation-legale/Base-prospectus et dans les conditions définitives (« Final Terms ») disponibles gratuitement sur le site fr.citifirst.com dans la rubrique « Documents » de chaque fiche produit, afin d’établir si le produit correspond à leurs besoins et à leurs moyens. Le Prospectus de Base Warrants et le Prospectus de Base Certificats de Citigroup Global Markets Europe AG ont été visés par la BaFin (régulateur financier allemand) le 16 novembre 2022 et ont fait l'objet d'un certificat d'approbation par la BaFin à destination de l'AMF, ce qui ne doit pas être considéré comme un avis favorable. Document communiqué à l’AMF conformément à l’article 212-28 de son Règlement Général.

C’est la partie “Soyons des adultes”. Avertissements sur les risques. Les partenaires cités sont des partenariats rémunérés. Les informations, graphiques, chiffres, opinions ou commentaires mis à disposition par Nicolas Chéron s’adressent à des investisseurs disposant des connaissances et expériences nécessaires pour comprendre et apprécier les informations développées. Ces informations sont données à titre informatif et ne représentent en aucun cas une obligation d’investissement ni une offre ou sollicitation d’acquérir ou de vendre des produits ou services financiers. L’investisseur est seul responsable de l’utilisation de l’information fournie, sans recours contre Nicolas Chéron, qui n’est pas responsable en cas d’erreur, d’omission, d’investissement inopportun ou d’évolution du marché défavorable aux opérations réalisées. Le placement en bourse est risqué. Vous pouvez subir des pertes. Les performances passées ne préjugent pas des performances futures, elles ne sont pas constantes dans le temps et ne constituent en aucun cas une garantie future de performance ou de capital. Les références à des classements et récompenses passés ne préjugent pas des classements ou des récompenses à venir. Les contenus de ces e-mails ne sont pas des conseils juridiques, fiscaux ou en investissement. Les informations dispensées sont de nature éducative et générale et ne sont pas des conseils en investissement, au sens des articles L. 321-1 et D. 321-1 du Code Monétaire et Financier.

|

No comments:

Post a Comment