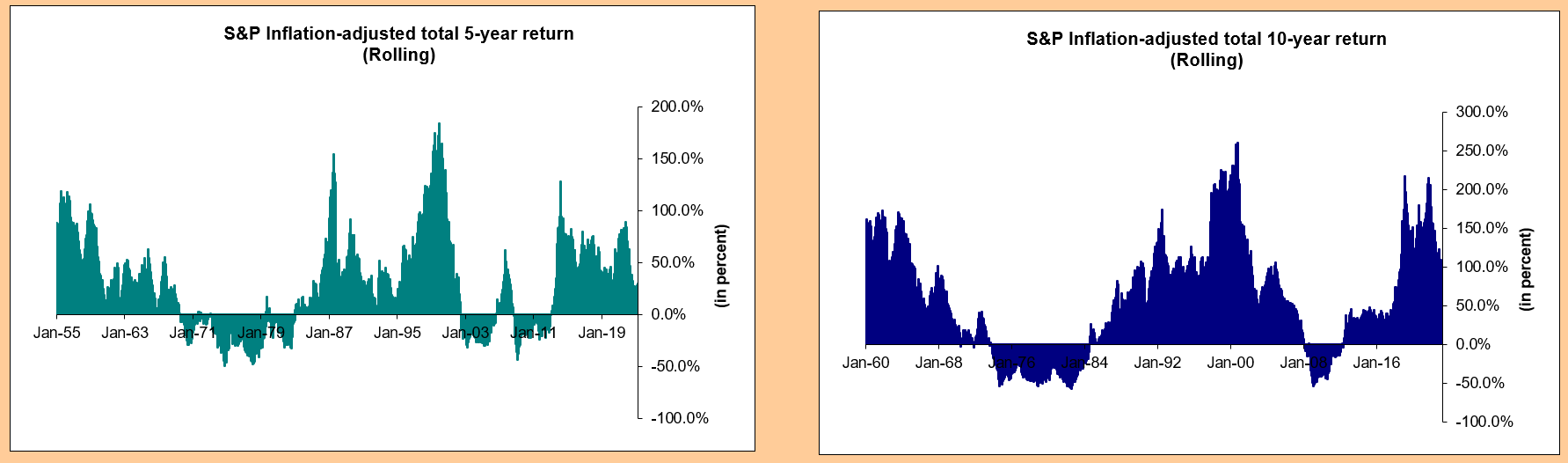

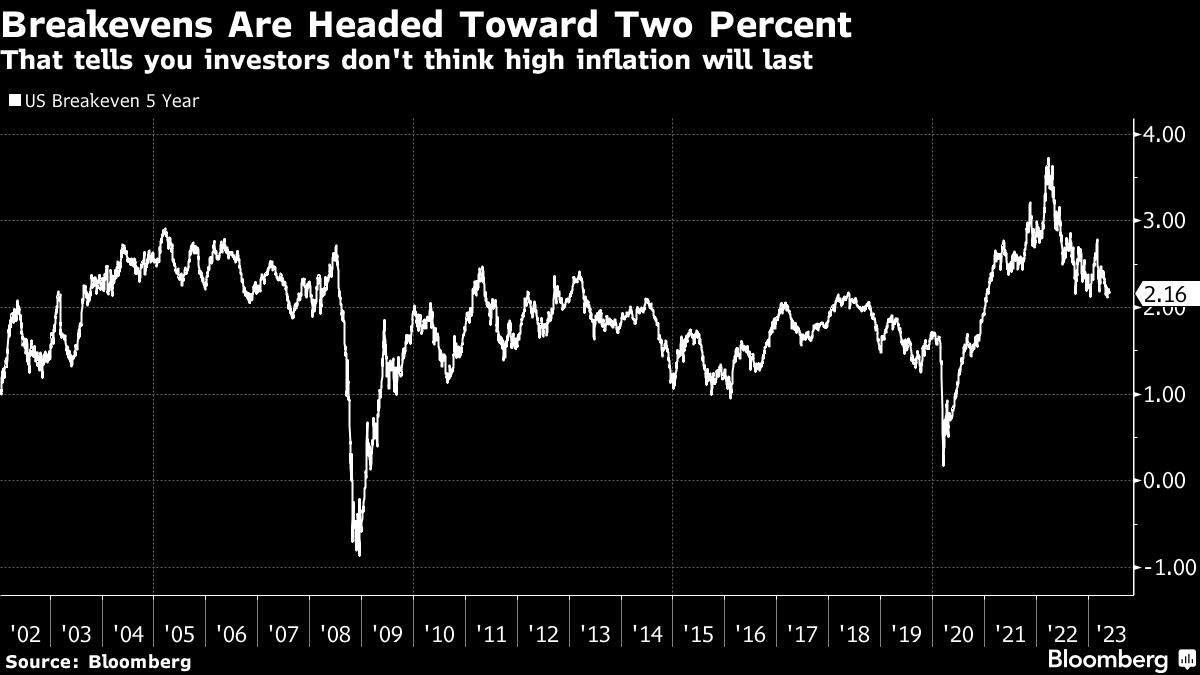

| Why does this mean reversion and overshoot happen? Here's my thinking. Equities are a residual. By that I mean, the equity is what's left over after employees, suppliers, taxes and interest are all paid. That free cash flow can be very volatile if any of those payment streams increases or decreases significantly, especially given any need to reinvest in the business. So equity holders usually get a return far in excess of the so-called risk-free rate that Treasury bond holders do (we'll call it risk free even though we all know the debt ceiling shenanigans make it riskier). The thing is, this premium is heavily influenced by interest rates because most of the free cash flows equity holders are paying for when they buy a share will only come in the future. And since that future money is less useful and less certain than a dollar in your pocket today, you have to discount it by an interest rate. Here's the thing, the unprecedented low rate regime we are leaving was unique in terms of the "real" interest rate investors required, both for risk-free Treasuries and for any other asset. Take a look at this chart of 5-year Treasury Inflation-Protected Securities (aka TIPS). It shows you what people have been willing to pay for a risk-free bond after stripping away inflation. Notice how we were at 4% when the dotcom bubble burst and have never returned to those levels. When Greenspan cut rates to 1%, the real rate (after inflation) plummeted well below 1%, fomenting the housing bubble. When the Fed tried to unwind this excess, it blew up into the Great Financial Crisis. This time, the Fed dropped rates even lower, to zero, and started asset purchases to boot. And real interest rates fell to nearly -2% in 2013 before Fed Chair Bernanke warned he was going to stop asset purchases. Eventually, his successor's successor, Jerome Powell, got real interest rates all the way back up to 1%. Presently, they're at about 1.7%, having briefly flirted with 2%. That's less than half the peak rate we saw in the late 1990s. Now, when we talk about real rates we're talking about the so-called breakeven rate on TIPS. That's the level of inflation implied from the interest rate TIPS that makes you indifferent to a normal Treasury security of the same maturity. It's the difference in rate between, say, a 5-year Treasury bond and the 5-year TIPS. And we can take inflation out of the picture here because that rate has remained fairly constant near the Fed's two-percent objective except during a recent inflation scare and the brief GFC deflation scare. So when we think about why discount rates are higher, let's think of it purely in "real" terms. It's only the real interest rate that's driving this bus. And that bus is being driven a lot faster right now, but nowhere near as fast as in a fully normalized situation. If we had 4% real rates, as we did when the tech bubble blew up, the echo bubble in stocks would blow up in a hurry. So forget about fiscal policy, the debt ceiling and inflation. Focus purely on real interest rates as you think about how this plays out. And mesh that with the business cycle in terms of corporate profitability. Doing so will go a long way of telling you where we're heading. A high real interest rate alone won't necessarily kill stocks. But it will when it is combined with a deep cyclical downturn as we saw in 1973-74 and in 2007-08. As bad as the tech bust was (with 4% real rates), it was still a garden-variety recession. Ten-year inflation adjusted returns on the S&P 500 were back to over 100% by November 2004. It took the Great Financial Crisis to wilt longer-term stock returns. Nvidia is trading at 25 times sales right now, on the back of an AI-centered stock mania. That's four times the level for other chip stocks in the Philadelphia Semiconductor Index. This isn't emblematic of early cycle bull market dynamics. It's the hallmark of late cycle, or echo bubble periods, as a market is coming down. So while inflation-adjusted 10-year returns for the S&P have been cut in half since September 2021, there is more downside to come. How far down depends on how high the real interest rate gets and how deep the recession is. Right now, this is looking to be a cycle more akin to the early 1990s or 2000s than the oil shock in 1973-74 or the GFC. That means 10-year returns getting cut in half again to around 50%. Not great, but not terrible. But that also means a market that treads water for a considerable period of time. Moreover, the more pronounced the echo bubble becomes, the more pronounced and the longer the mean-reversion is likely to be. For those close to retirement, that presents some minor risks for sure. And it's one reason that overweighting towards investment-grade bonds and cash is looking ever more attractive. |

.png)

No comments:

Post a Comment