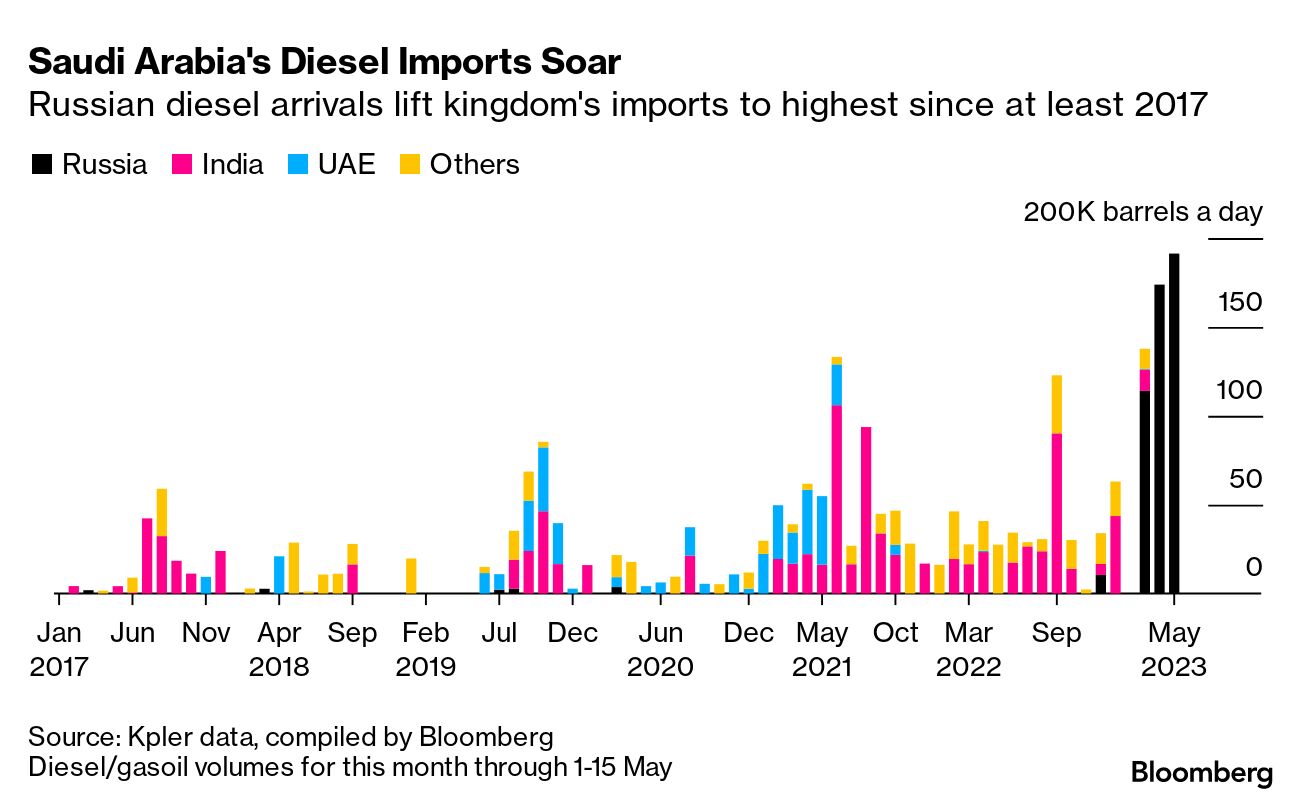

| Turkey's Recep Tayyip Erdogan sealed an election victory that many pollsters thought unlikely just weeks ago, raising the prospect of more friction with foreign investors. Erdogan won with 52% of the vote in a presidential runoff against Kemal Kilicdaroglu on Sunday, giving him another five-year term. Investors' attention now turns to Erdogan's new economic team, with the cabinet possibly being announced on Friday. Its makeup may hint at whether the 69-year-old is preparing to shift away from his unorthodox approach to managing the nation's finances. The country's longest-serving leader appeared on top of a bus in Istanbul and thanked Turks for re-electing him. While saying "the winner of today is Turkey only," he acknowledged that inflation — which stands at more than 40% — is hurting the economy. Many foreign investors say he's largely to blame for exerting a tighter grip on the the central bank, which has kept interest rates well below the level of inflation.  A supporter watches a video speech of Recep Tayyip Erdogan in Istanbul on Sunday, May 28, 2023. Photographer: Kerem Uzel/Bloomberg The currency weakened near a record low on Monday, falling below 20 against the dollar. Wall Street analysts are predicting more pain for Turkish assets. Morgan Stanley says the lira may slide almost 30% by the end of the year. Many analysts and money managers are unconvinced there will be a shift from ultra-loose monetary policy and heavy state intervention in markets anytime soon. "An Erdogan win offers no comfort for any foreign investor," said Hasnain Malik, a strategist at Tellimer in Dubai. "Only the most optimistic would hope that Erdogan now feels sufficiently secure politically to revert to orthodox economic policy." Erdogan will undoubtedly read his latest election victory as a mandate to continue his pugnacious foreign and economic policies. Both he and Turkey would be better off steering a more pragmatic course, Bloomberg Opinion's editorial board writes. Saudi Arabia is snapping up millions of barrels of Russian diesel that Europe no longer allows, while simultaneously sending its own supplies back to buyers in the EU. The kingdom imported 174,000 barrels a day of the diesel and gasoil from Russia in April and even more so far this month, data compiled by Bloomberg from analytics firm Kpler show. Simultaneously, it became Europe's top supplier, leapfrogging Russia since February. Also Read: Clock Is Ticking for Qatar to Sell Its LNG Lowest since 2010: Saudi Arabia's foreign reserves fell in April to the lowest in more than 13 years, in an apparent sign the kingdom hasn't yet used last year's $326 billion oil windfall to top up the central bank's holdings. Another Saudi deal: Boeing is in talks to sell at least 150 of its 737 Max jetliners to startup Riyadh Air — a second major win that would give the US planemaker an edge in a Gulf market primed for growth. Ending the IPO drought: The Riyadh initial public offering of generic drugmaker Jamjoom Pharma will raise $336 million after shares were priced at the top of a marketed range. Also Read: Adnoc Unit Gets $125 Billion in Orders for $769 Million IPO Olam Agri and more: Dual listings between the Middle East and Asia are expected to become a new trend as investment flows between the two regions rise, according to bankers. Market makers: Qatar's sovereign wealth is setting up a $275 million program as the country seeks to draw more foreign investor interest and deepen its capital markets. The $450 billion Qatar Investment Authority is also channeling its money into tech startups and private credit. Private equity magnet: French firm Ardian plans to nearly double its presence in Abu Dhabi to take advantage of investment opportunities in the Middle East. Pound dilemma: The currency's value is proving to be a sticking point for Egypt's efforts to sell state assets to allies such as Saudi Arabia, Qatar and the UAE. Economists see deal-by-deal exchange rates among the ways the North African country and its Gulf allies could thread the needle.

Big grants: Israel's parliament passed a national two-year budget that includes billions in funding for West Bank settlements and religious programs, stabilizing Prime Minister Benjamin Netanyahu's right-wing coalition. Climate politics: More than 100 US and EU lawmakers appealed to the leaders of their countries and the United Nations to oust oil executive Sultan Al Jaber as head of this year's COP28 climate summit. Also Read: Maasai Are Getting Pushed Off Their Land So Dubai Royalty Can Shoot Lions Europe-Asia link: Iraq is pitching a $17 billion network of roads and railways it says will help the region transport energy resources, goods and passengers. Social safety net: The World Bank will dispatch $300 million in additional financing for the most vulnerable families in Lebanon, a country mired in what the lender called one of the worst economic and financial crises in history. Crypto concern: Dubai's financial regulator warned that global watchdogs need to step up talks with each other to avoid "bad actors" exploiting gaps in cryptocurrency rules. Also Read: Saudi Arabia's Five-Year-Old Film Industry Hits Cannes Festival - Turkey April trade balance: May 30

- Turkey first-quarter GDP: May 31

- OPEC+ meeting to decide oil output: June 3-4

- Saudi Arabia, UAE and Egypt May PMI : June 5

- Turkey May CPI: June 5

The third annual Qatar Economic Forum last week was dominated by stark warnings from energy rich Gulf nations and conflicting outlooks on the state of global economy. Saudi Arabia's Energy Minister Prince Abdulaziz bin Salman told oil short-sellers to "watch out" just over a week before the OPEC+ alliance is due to meet, causing oil to rally as traders evaluated his words.  Abdulaziz bin Salman, Saudi Arabia's energy minister (second from left), Hayan Abdul Ghani Al-Sawad, Iraq's oil minister, and Saad Sherida Al-Kaabi, Qatar's energy minister, speak during a panel session at the Qatar Economic Forum. Photographer: Christopher Pike/Bloomberg Qatar's energy minister raised the red flag on natural gas shortages in the coming decade. "There's going to be a big shortage in gas in the future, predominantly because of the energy-transition push that we'd say is very aggressive," Saad al-Kaabi said. Also Read: Hungary Seeks Gas From Qatar to Cut Russia Reliance, Orban Says The current turmoil in the banking industry, which has seen the collapse of four US lenders and the takeover of Credit Suisse, isn't over and growth is a concern, according to the chief executive of Commercial Bank of Kuwait. "Many things are happening at the same time, so the world is worried," Elham Mahfouz said. Standard Chartered CEO Bill Winters said the banking system would endure its current issues with plenty of liquidity, but investors will be focused on whether deposits are as sticky as they thought. The British lender's biggest concern is stubborn inflation. Those worries were echoed by Moelis, which expects the US central bank to continue to be aggressive for the time being as the inflation rate is likely to stay higher for longer. More QEF Coverage: |

No comments:

Post a Comment