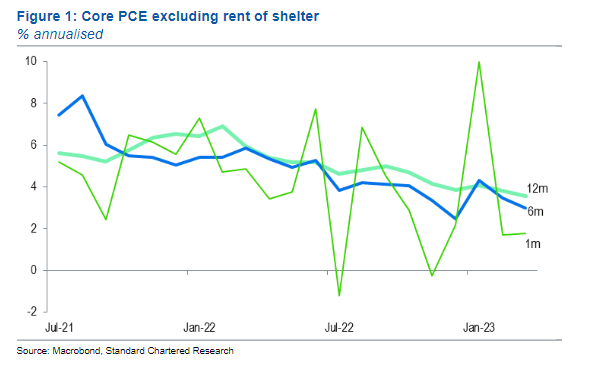

| JPMorgan helps rescue First Republic Bank, China's manufacturing falls back into contraction and investors say following Warren Buffet will be a market-beating strategy. — Sofia Horta e Costa JPMorgan will assume all deposits held by First Republic Bank after the troubled lender was taken over by US regulators. The resolution came after the weekend's emergency auction, where banks including JPMorgan, PNC Financial Services and Citizens Financial were asked to submit offers. Also invited were Bank of America and US Bancorp — but both decided against bidding. JPMorgan, the country's largest bank, had the advantage of what Chief Executive Officer Jamie Dimon calls its fortress balance sheet heading into the government-led attempt to sell First Republic. China's factories are grappling with weaker global demand. Purchasing managers' indexes for April denoted an unexpected slowdown in factory activity, the first time the indicator falls below 50 this year. Sub-indexes for new orders, new export orders and manufacturing employment were all in contraction territory. China's economic recovery risks losing steam, analysts said, with the figures adding pressure on the government to increase policy support. The Communist Party's Politburo — the top decision-making body led by President Xi Jinping — recently said domestic demand is still insufficient. That said, evidence consumers are traveling across the country and splurging over the May holidays may give them some breathing room. Want to beat the US stock market? Follow legendary investor Warren Buffett, according to both professional and retail investors who took part in the latest MLIV Pulse survey. More than half of the 352 respondents expect Berkshire Hathaway's returns to beat the S&P 500 over the next five years. Buffett's strategy of buying shares for less that they're worth will be the Berkshire chairman's biggest legacy, according to 80% of investors. Following his recent trip to Japan, respondents agreed the country offers value but were more divided on whether Japanese stocks will fare better than those in the US. US futures are little changed while Treasuries are edging lower after a muted session in Asia. There was no trading in much of Europe to observe the May 1 holiday, with markets also shut in Asian centers like Hong Kong, Singapore and mainland China. At 10 a.m., we'll get the ISM manufacturing report for April as well as data on construction spending for March. Earnings are due from ON Semiconductor and NXP Semiconductors before US markets open, while MGM Resorts reports after the close. Here's what caught our eye over the weekend: Good morning. It's a huge week for economic news at a time of tremendous economic ambiguity. After this week, we should have a lot more clarity. That last line is a joke. You never get clarity. But in terms of what's coming up, well of course there's the Fed decision on Wednesday, and the expectation is for a 25 bps hike. After that though, nobody is sure. As Steve Matthews and Rich Miller report, there are signs that the FOMC is growing more and more divided about what to do next. The division is understandable. As has been the case all year, you can tell all different kinds of stories right now about the economy. Inflation is still hot and way above trend. On the other hand, as Standard Chartered's Steven Englander observed in a note this weekend, core PCE ex-rent of shelter (which has a emerged as a key measure) continues to trend lower. Meanwhile, here's Tim Duy of SGH Macro: "There is nothing here to hang your hat on and conclusively say, in the words of Federal Reserve Governor Christopher Waller, that inflation is "meaningfully and persistently" on track to 2%. Two more months like March, however, with core PCE inflation running lower than the Fed's year end projection, would go a long way toward meeting that criterion."

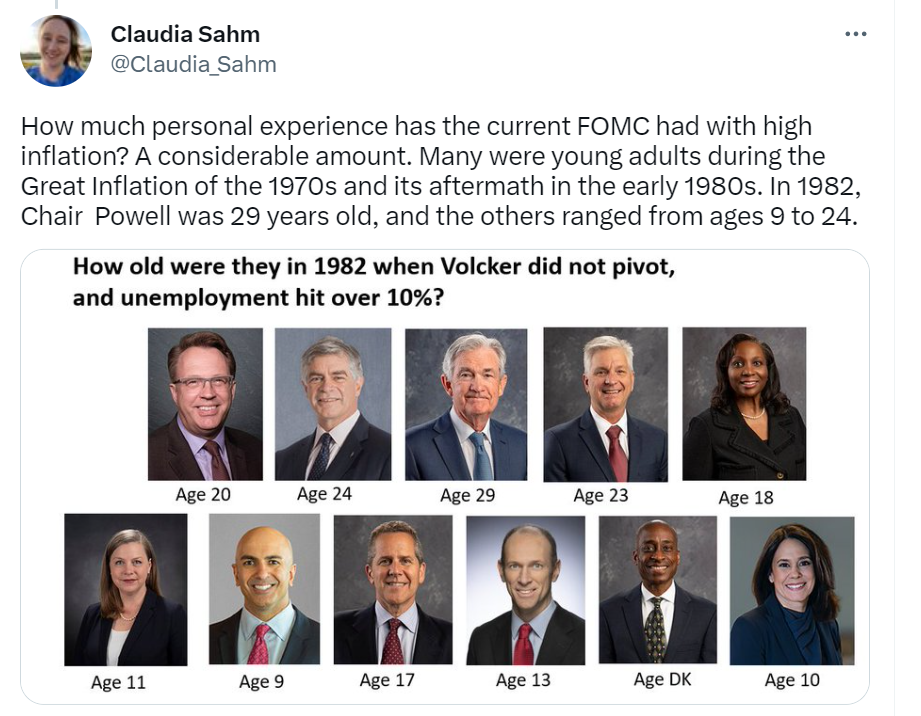

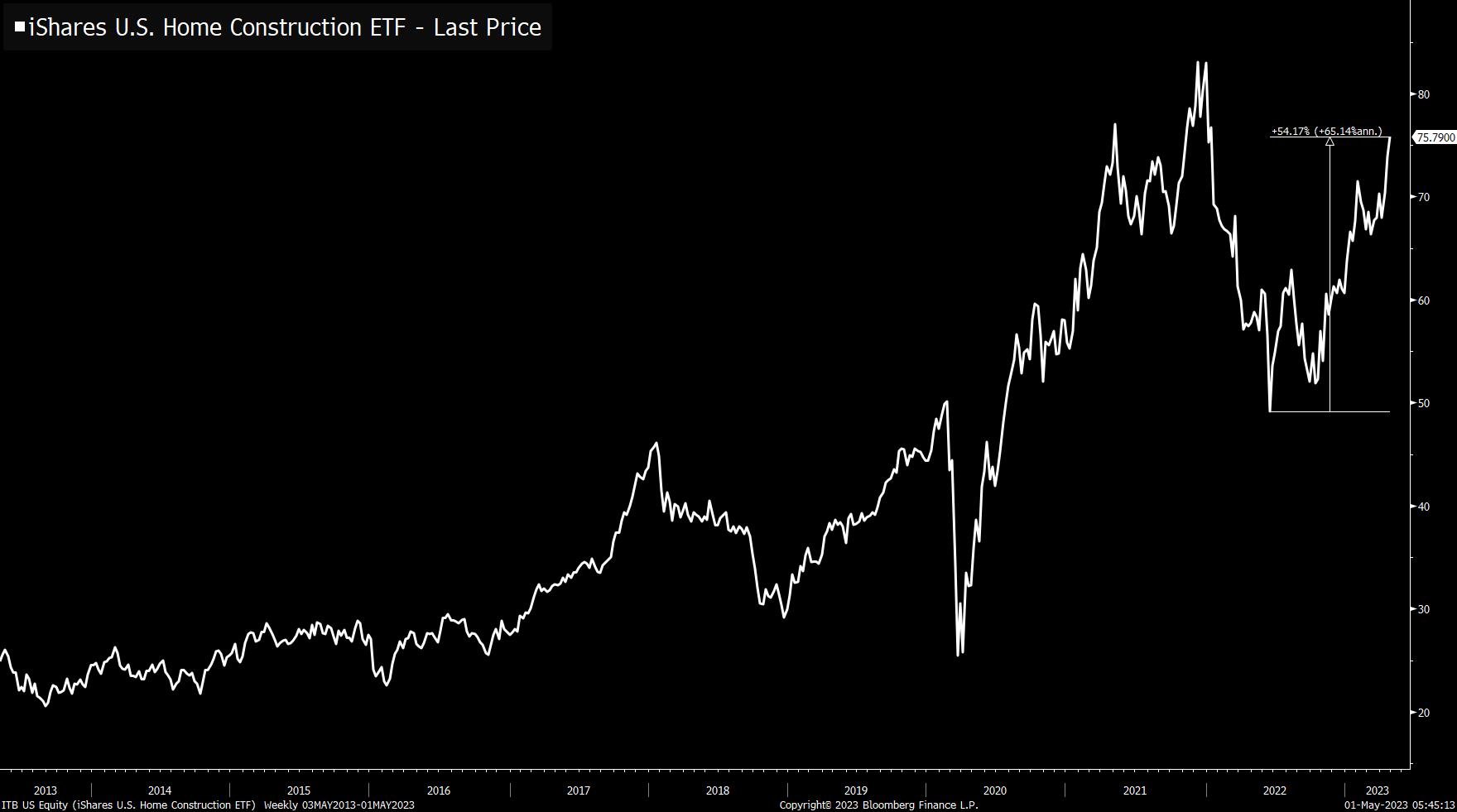

BTW — here is a great thread from Claudia Sahm about why she doesn't expect any imminent pivot, even if the unemployment rate were to pick up. The TLDR is that the memories of Arthur Burns and Paul Volcker (or really, the popular historical perceptions of both of them) loom large in the heads of Fed officials today. I really liked this tweet in the thread. So that's inflation. But ambiguity abounds elsewhere. The regional Fed manufacturing measures have been really ugly, with bad prints from the Philly Fed, Richmond Fed and all the others in recent weeks. Headline labor market measures remain quite strong, but there are signs of slowing. One thing to watch is that there are signs that white collar layoffs are starting to pick up, and that the number of so-called "permanent job losers" is starting to rise. Here is a good read from Preston Mui at Employ America on this. Again, the absolute levels are not bad at all. But all recessions have to start somewhere and so it's worth keeping an eye on any derivative of labor market weakness. Speaking of the labor markets. One thing I noticed last week while reading through quarterly conference calls to see what management was saying about inflation is that multiple companies commented about how hiring has gotten easier. This doesn't necessarily mean a big jump in the unemployment rate is imminent. But there is easing on this front. The other big wild card is housing. This was the one area that was assumed to be very interest rate sensitive. And for a few minutes there, it looked like it really was going to go into a downturn thanks to last year's rapid hikes by the Fed. And yet here we are with ITB homebuilder ETF really not that far from all-time highs, having bounced by 54% since last summer. Meanwhile, there are all the usual reports again about low inventories, a modest pickup in bidding wars, and other signs of life. So if you subscribe to the general idea that "housing is the business cycle" then it's hard to see a recession around the corner. Anyway, today we get the latest ISM Manufacturing report, and then Friday we get the jobs report. And in between we'll get numbers on factory orders, auto sales, and more. It'll be an interesting week, even things will probably end up no less ambiguous when all is said and done. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart. |

No comments:

Post a Comment