| Hello. Today we look at how central bankers and some investors are split in their views of oil's impact on policy, diverging growth among US states, and how money-market fund flows could influence policymakers. One thing was becoming clearer on the day after OPEC+'s surprise production cut: It has widened the already yawning gap between how central bankers expect monetary policy to pan out this year and investors' bets. For central bankers, the news was just one more headache, after a series of banking dramas, that complicates their policy decisions at a critical time, as Craig Stirling, Philip Aldrick and Steve Matthews write. St. Louis Fed chief James Bullard told Bloomberg Television that it's an "open question" as to how much lasting impact the OPEC+ decision will have on inflation and interest rates, but that oil could make the Fed's inflation fight harder. For markets, a particularly manic Monday was colored not just by the OPEC+ news but also weak factory data globally that fed the narrative of some investors that a fast-easing growth outlook will force central bankers into cuts. Ken Shih, head of wealth management for Greater China at Saxo Markets, put it this way on Bloomberg Television: "The biggest risk for me is really looking at the gap between the expectation of what the market is expecting and what the Fed rhetoric is showing in terms of the Fed policy path," with some still pricing in a cut later this year that runs against the Fed narrative. A downturn from here could raise the risk of a cut at year-end, but "for the time being, rates stay higher for longer."

Range of Views For now, beyond the near-term surge in oil prices, it's mainly sentiment and inflation expectations that are driving the debate. In the hard data, analysts seemed to coalesce around the idea that inflation measures are unlikely to show immediate impact by the mass production cut: - "For now we expect the direct impact of higher oil prices on core inflation to be modest. Upside risks for inflation expectations due to higher energy prices however could be more consequential for Fed policy," said Citi's Veronica Clark and Andrew Hollenhorst

- Marc Ercolao, an economist at TD Bank Group, points out that "the actual reduction in supply may be less than target as many OPEC+ members continue to produce below their quotas"

- Putting the run-up in perspective, Douglas Porter, chief economist at BMO, was among those noting that "while this moderately complicates the disinflation momentum, it's more akin to the removal of a helpful trend, rather than the start of a new problem"

- Michael Tran, commodity strategist at RBC Capital Markets, said the volatility doesn't change an underlying view that crude prices should push higher while they'll "net-net have little material impact on the end use consumer. The greater the passage of time without further macro contagion, the more comfortable the market becomes that oil prices can trend higher"

- Asian Development Bank Chief Economist Albert Park said his team already "anticipated that supply would remain somewhat constrained this year," given higher demand from China amid its rebound. While risks are to the upside, they didn't see urgency in changing their forecast for oil prices to average about $88/barrel this year and $90 in 2024

So, perhaps some solace for central bankers who would prefer to set aside this risk as they charge ahead on their policy paths. If the oil developments contribute to a surge in consumer inflation expectations, and a self-fulfilling prediction on growth downturns, though, it could be a much darker story — one that even OPEC+ might come to regret, Vishnu Varathan, Singapore-based head of economics and strategy at Mizuho Bank, said on Bloomberg Radio: The production cut "has complicated policymaking and intensified risks, which for the OPEC may perversely turn out to be self-defeating."

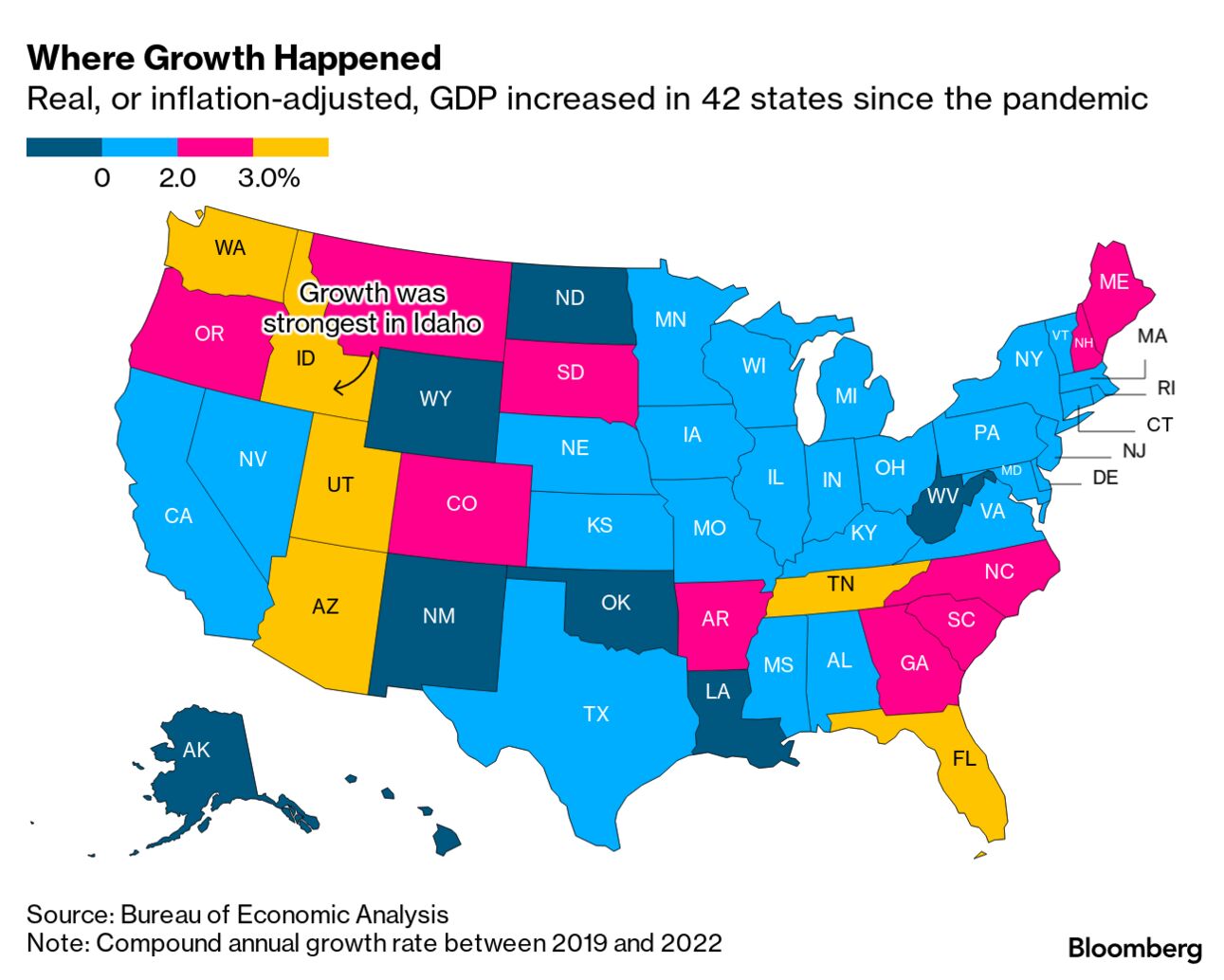

—Michelle Jamrisko While US GDP recouped the losses from the 2020 Covid shock by the first half of 2021, that national marker masks significant variation within the country. New data show that in nearly half of US states, the economies have barely grown — or even shrunk — since the pandemic. Gross domestic product was lower in 2022 in eight states, including Louisiana and Hawaii, which are dependent on tourism, according to a recent release. And 13 states saw GDP expand at an annualized rate of 0.5% or less over the three-year period, the data showed. Florida and Texas, which are each in the top three fastest-growing states since 2019, benefitted from migration shifts. California grew the most in dollar terms, thanks to a tech boom when Americans were stuck at home. - Falling empire | Southern California's Inland Empire, the warehousing mecca that's home to Amazon.com and Walmart facilities, is showing signs of trouble.

- Lower expectations | Consumer expectations for euro-area inflation fell for a second month — supporting recent remarks by European Central Bank officials that interest-rate hikes may be nearing their end.

- Oz pause | Australia's central bank paused its almost yearlong tightening cycle, sending the currency and bond yields lower.

- China crackdown | Chinese authorities warned the nation's top banking executives that the crackdown on the $60 trillion industry isn't over.

- Thatcher's Chancellor | The former UK Chancellor of the Exchequer Nigel Lawson, who oversaw London's Big Bang financial deregulation in 1986 — a key component of Margaret Thatcher's agenda — has died.

- Banks stabilizing | Treasury Secretary Janet Yellen said the situation around US banks was "stabilizing," though regulators stood ready to repeat extraordinary actions taken in March to contain depositor runs.

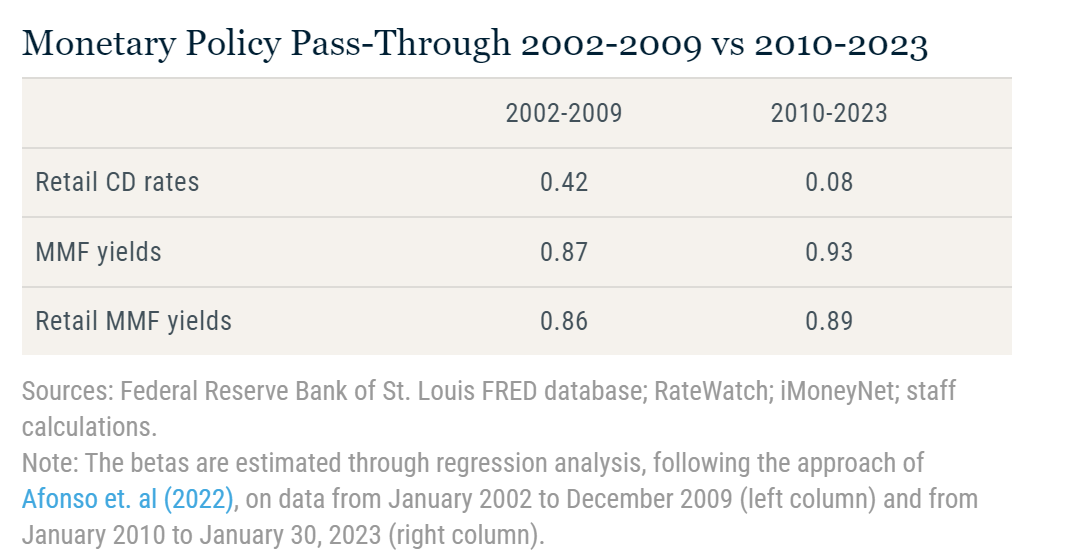

Money-market funds have been siphoning off billions of dollars worth of savings from banks' deposit holdings, and the pattern may be just getting started if research by the New York Fed is a guide. The lure is obvious: MMFs are much faster at passing through higher Fed policy rates to savers. The New York Fed researchers calculate that, since March 2022, yields on MMFs have risen by 4.13 percentage points, while banks' three-month certificate of deposit rates are only up by 0.32 percentage point. (Before the financial crisis, banks used to pass along more of the Fed hikes, the group's analysis showed.) History shows that it takes one to two years for the MMF industry to expand in response to rate-increasing cycles, the study said. Any further swelling could become an important issue for policymakers, as Alex Harris reported here, given how MMFs provide much less credit to non-government borrowers. Bloomberg New Economy Gateway Europe will be held in Ireland, April 19-20. Join us as leaders gather to discuss solutions to the most pressing challenges facing the European economy. Request an invitation. The other jobs day... Read more reactions on Twitter |

No comments:

Post a Comment