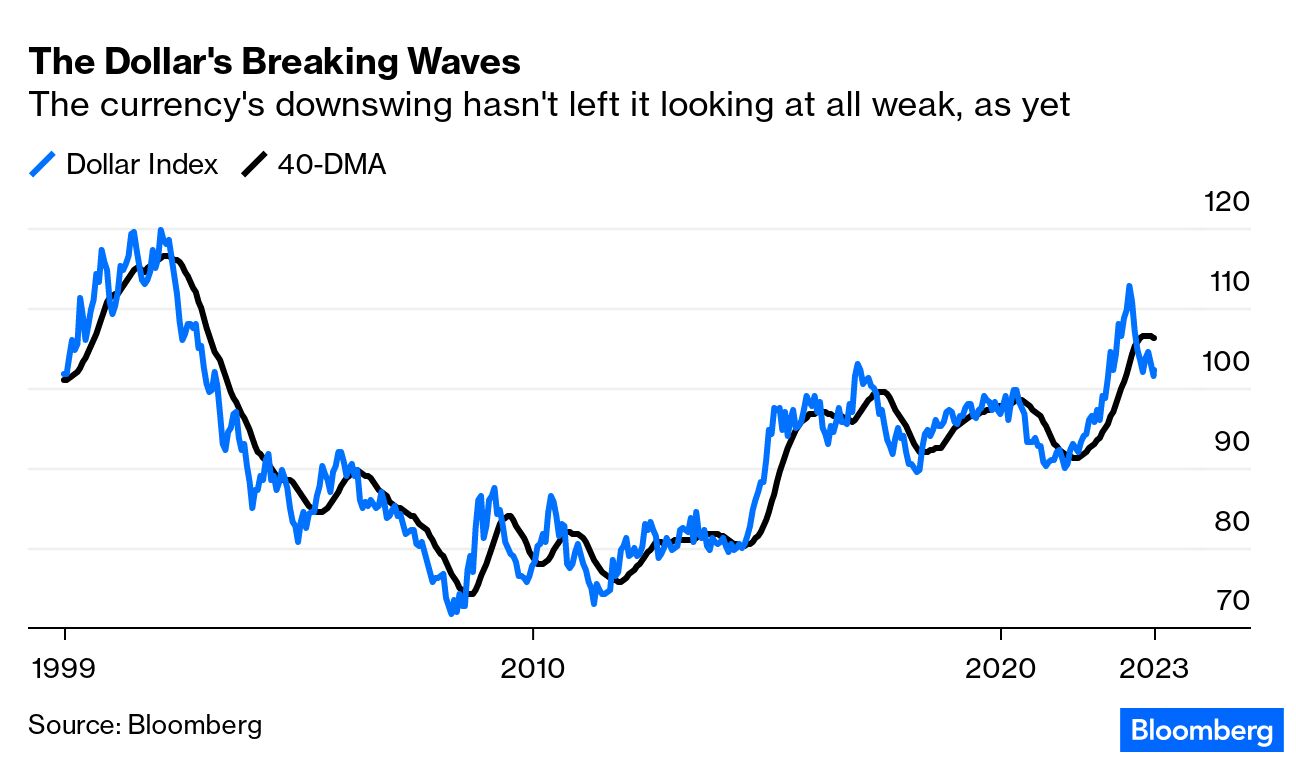

| De-dollarization is all the rage. Or at least talk about it. Television pundits as disparate as Fareed Zakaria on CNN and Tucker Carlson on Fox News have devoted entire shows to the US currency's status. According to the research group GlobalData, discussion of de-dollarization on platforms such as Twitter and Reddit was up 600% during the first quarter, compared to the last three months of 2022. Why the excitement? There are two separate if related concepts here. First, there is the strength, or value, of the dollar in terms of its exchange rates compared to other currencies. Second, there is the role it plays as the global reserve currency. Its value has dipped recently, and appears to be entering a new long-term downward trend. But it's still stronger than it has been for most of this century. It's therefore intriguing that a cyclical downturn in the dollar's value has been accompanied by a welter of speculation that it's about to lose its role in the global economy:  There's nothing in the greenback's recent performance to suggest that its status is in danger. But a number of separate political incidents have driven the discussion. Various presidents, including Emmanuel Macron of France and Luiz Inacio Lula da Silva of Brazil, have been to China to meet Xi Jinping, who has himself gone to see Vladimir Putin in Moscow. China and Brazil are working on a deal to settle trades in their own currencies rather than dollars. All feed a narrative that the dollar is losing its "exorbitant privilege" (to use the phrase of the late French president Valery Giscard d'Eistaing), which has given successive US leaders and central bankers far more freedom of action than their peers. Any discussion along these lines swiftly gets into deep waters. Those who most vehemently oppose US monetary policy of the last quarter century (and they have plenty of reason to do so) present de-dollarization as an inevitable result of currency debasement. As in many other fields, this creates an odd alliance between the socialist left and libertarian right. The notion is obviously appealing to US competitors, which is why they promote it with evident enthusiasm. This piece from Russia's Duma gives arguments for de-dollarization from a Russian perspective. Search for "de-dollarization" on Google and you find a sponsored link to this handy page on the Chinese-backed Epoch Times, which groups all the many pieces it has published on the subject. As these publications have a strong interest in the dollar's dethronement, their arguments need to be treated with extreme caution, but at least they are well expressed. Louis-Vincent Gave of Gavekal Research suggests that the volume of speculation shows that the zeitgeist is changing, and that US policy might now be to weaken the dollar (although the Federal Reserve's actions over the last year would undercut such a thing.) Global confidence in the US as a jurisdiction is eroding, he adds: Over the past 15 years or so, capital in the US was both very cheap and easily accessible, whereas in Japan and Europe, while capital was cheap, banks weren't exactly lending hand over fist, and in most emerging markets capital was never stupidly cheap nor easily accessible. It stands to reason therefore that if capital was wasted, it was most likely wasted in the US. So if you agree that handing out cheap and plentiful money is the financial equivalent of giving adolescent boys fast cars and free whiskey, you will not be surprised if, as the price of capital rises, most of the financial accidents take place in the US. Purely on anecdotal evidence, it does feel as if most of the stupidity of recent years — Theranos, FTX, GameStop, Bed Bath & Beyond — was a US phenomenon.

So there are good reasons why the rest of the world might want to abandon the dollar. But that doesn't mean that de-dollarization is imminent, and it certainly shouldn't imply that it would be easy to abandon the buck. Brad McMillan, Chief Investment Officer for Commonwealth Financial Network, offers the following neat thought experiment to explain how difficult it will be: Suppose I told you that Amazon would collapse this year and that people would abandon it and flock to other merchants (e.g., Walmart). That argument makes a certain amount of sense, in that Walmart is indeed a valid competitor, is trying very hard and spending a lot of money to take business from Amazon, and has the scale to do so credibly. But when you think about it, the idea is kind of silly. Personally, I have an Amazon Prime account, I have multiple orders pre-set, I watch Prime video, and so on. It would be a lot of work and a major inconvenience to switch — even if Walmart offered a full range of competitive services. Walmart may do so, but I haven't even looked, which kind of proves my point. Unless you believe that tens of millions of people are suddenly going to do the work and endure the inconvenience of switching, then the idea that Amazon will suddenly collapse simply isn't credible. I think you see where I am going with this. The US dollar is Amazon, and the Chinese yuan is Walmart. Yes, China would like to dethrone the dollar, but it isn't that simple. As long as the US is the largest open trading economy, as long as everyone in the world wants access to the US economy, and as long as it is a lot of work and a great inconvenience to switch, the position of the dollar as the global reserve currency is secure.

Brent Donnelly, president at Spectra Markets, is even more dismissive, and offers plenty of examples of the way that de-dollarization has been discussed for years, without every happening: People have been talking about de-dollarization since 1990 and say gradually then all at once. But that only sounds smart when Hemingway says it. I believe it'll be a very gradual process because there's no legitimate competitor. That's the issue with the de-dollarization story. The yuan is gaining a little bit of market share. But essentially, I don't think anything's going to replace the dollar in our lifetime as a reserve currency.

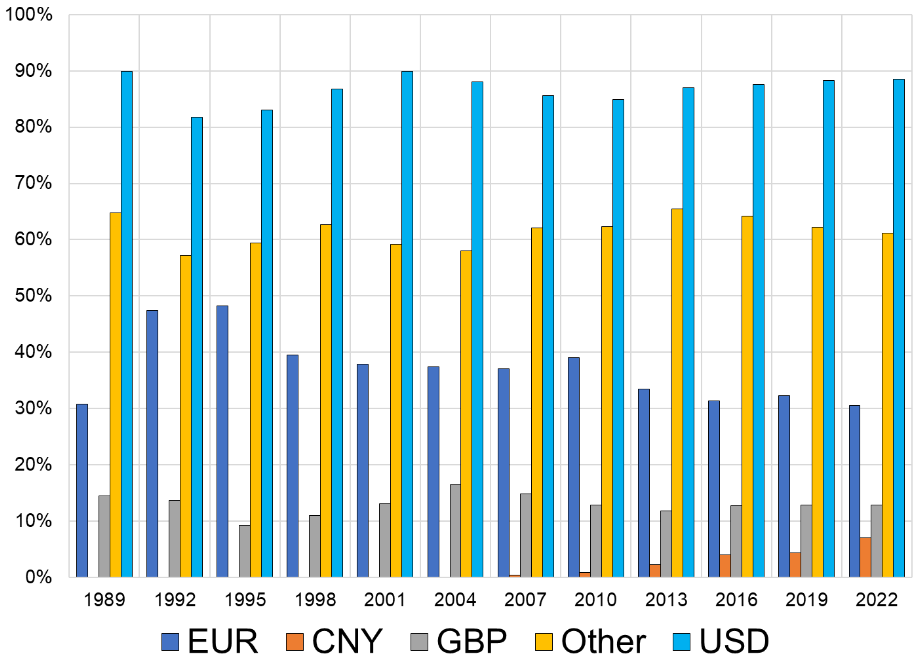

The triennial surveys of foreign-exchange markets conducted by the Bank of International Settlements confirm that though the dollar is losing a little market share, it remains a long way ahead of the competition. And even the British pound is still involved in more transactions than the Chinese yuan. The chart was produced by Spectra Markets using BIS data:  Source: Spectra Markets, BIS Triennial Survey Thus, the most fundamental measures of currency trading suggest that de-dollarization isn't happening at all, despite the valid criticisms of US money-printing in recent years. Donnelly makes clear that he sympathizes with this point of view, even though he disagrees with it: The reality is that it's more like all fiat currencies are being devalued and actually the dollar is the cleanest dirty shirt; it's the best of the fiat currencies. It doesn't mean owning gold or crypto is wrong because the orthodox policies now allow for unlimited spending in times of difficulty. But the idea that the dollar losing its status, to me, is just not true. And I guess the reason that bugs me is because I've been hearing this for so long and the data doesn't support it at all.

Does this mean that the dollar's exorbitant privilege is eternal? That would be a very dangerous bet; the British pound used to be the reserve currency for the better part of a century, and other imperial powers had that rank before that. Reserve currency status is difficult to lose once you have it, but it can happen. McMillan offers three things that make the dollar "special:" - The sheer size of the US economy. Only the yuan and euro are anywhere close.

- The freely convertible nature of the dollar. While China's government continues to exercise strong control over the yuan's exchange rate, it creates far more political risk.

- The political and economic stability of the US compared with both Europe and China

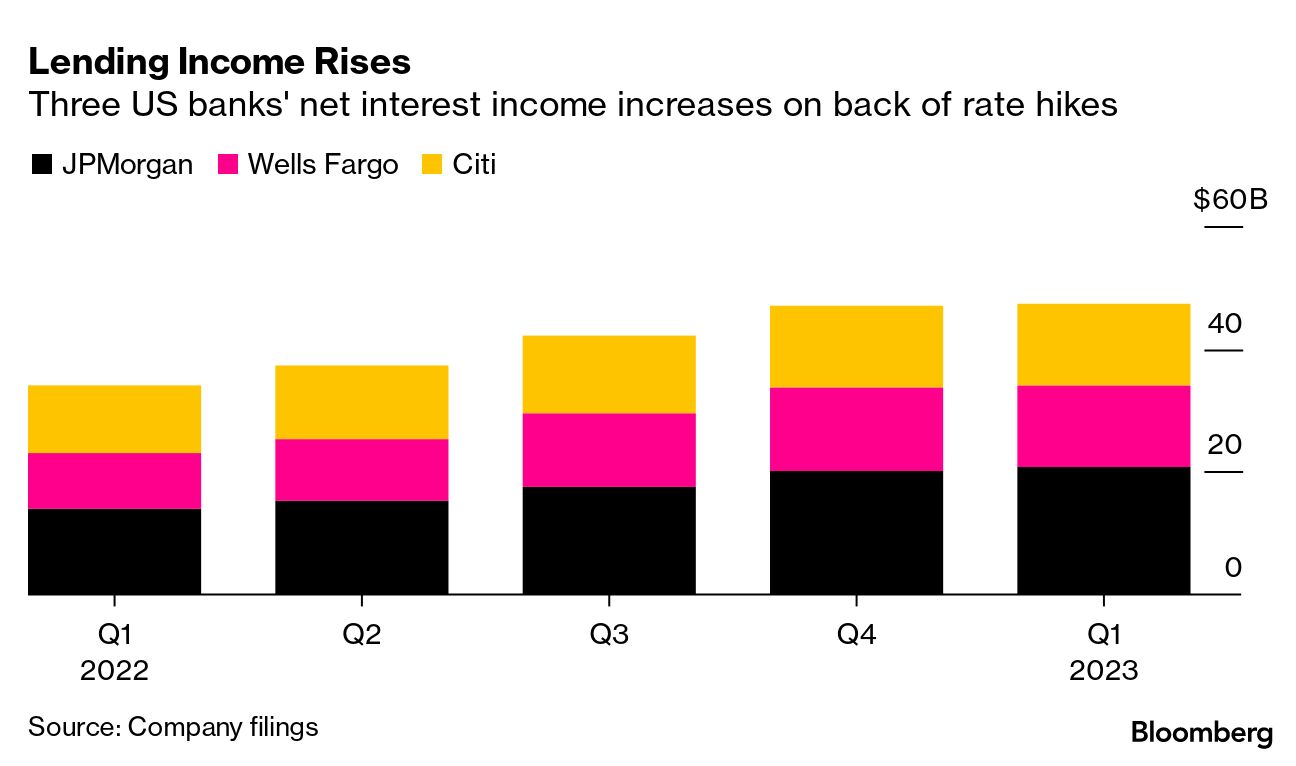

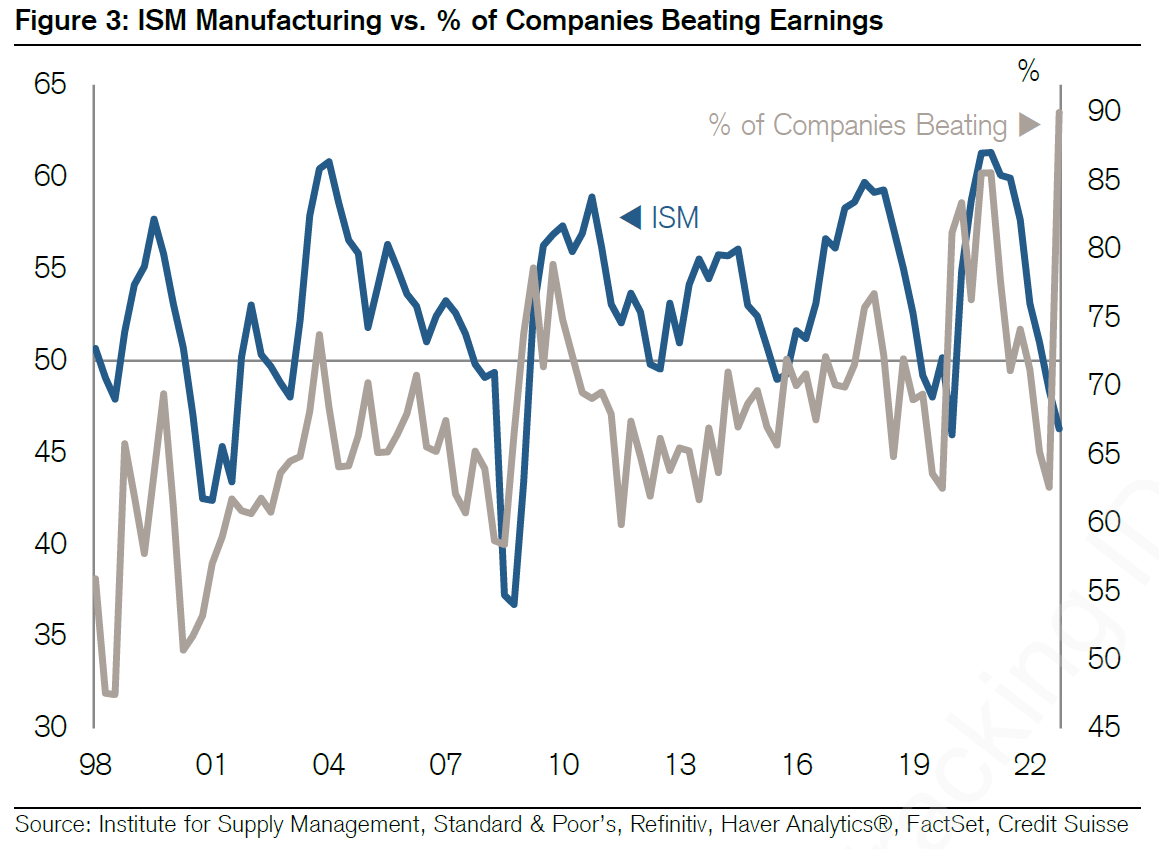

None of these things will necessarily last forever. If China keeps growing, and opens its economy, and if the more worrying polarization trends in the US imperil its political stability, then the dollar could, in time, lose the exorbitant privilege Giscard detested. Barring an economic and political implosion in the US, the dollar will keep its status for a while. Which doesn't mean that a fresh easing in rate expectations couldn't bring its value down in the meanwhile. After all the gloom ahead of the first-quarter earnings season, the early announcements haven't been all that bad. At least not yet. In fact, the big banks — JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co. — pleasantly surprised traders. Most reaped gains from the problems that suddenly roiled smaller, regional banks as the Fed continues to raise rates to curb inflation. The hikes are generally boosting revenue from lending and driving trades: The tune shifted slightly on Monday as the brokerage Charles Schwab Corp. revealed its deposits tumbled 30% during the quarter, in line with most estimates, and that this had forced it to halt stock buybacks. Schwab was a casualty of the move by depositors to move uninsured deposits. Shares of Schwab rose 3.9%, paring their decline this year to 37%. It's much too early to read anything into this, but the better-than-expected kickoff to the season has shifted the mood ever so slightly. A slew of banks is slated to report this week and offer more insight into the macroeconomic outlook. These include too-big-to-fail investment banks Goldman Sachs Group Inc. and Morgan Stanley, but more heavily scrutinized will be large regional banks that don't benefit from that status, such as Fifth Third Bancorp and KeyCorp. Here's a handy schedule to guide you. Overall, forecasts seem very bearish. Bloomberg Intelligence predicts first-quarter earnings in the S&P 500 to fall about 8% from a year ago, the biggest decline since the start of 2020. Forecasts now imply a top-line recession, though not until the second quarter, BI's Gina Martin Adams and Wendy Soong wrote. But despite this, the benchmark has rallied since the last earnings season. Despite the biggest earnings drop since the onset of the pandemic, surprises have been extremely strong in the early going, Credit Suisse Group AG strategists, including Jonathan Golub, wrote Monday. Twenty-seven of 30 companies have topped estimates, with an aggregate beat of 9%. This, they said, is "unusual" as the pace of surprises typically wanes when economic sentiment suggests a recession, indicated by any time the Institute for Supply Management's gauge of manufacturing activity dips below 50. Currently, it stands at 46.3, which was below expectations, and would normally imply a lot of companies failing to meet their estimates: As reporting season gets going and bearish calls prevail, Societe Generale strategists, including Andrew Lapthorne, said behind the "apparent pessimism," bottom-up earnings do not seem consistent with either a recession or inflation reverting back to the 2% target: This is set to be quite an interesting reporting season. At first look, forward profit expectations for 2023 appear quite bearish, with a decline in non-financial earnings expected in the US and Europe and with 45% of countries forecast by the consensus to see profits decline this year ... despite the low headline number, the bottom-up consensus estimates envisage a transfer of wealth away from input prices to consumption, i.e. simply a reverse of what happened last year.

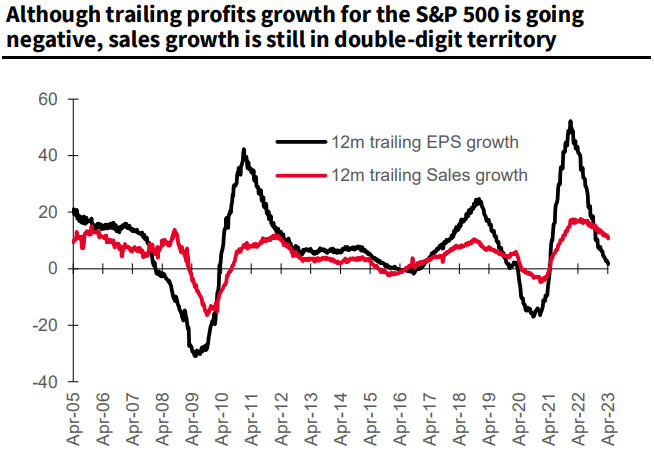

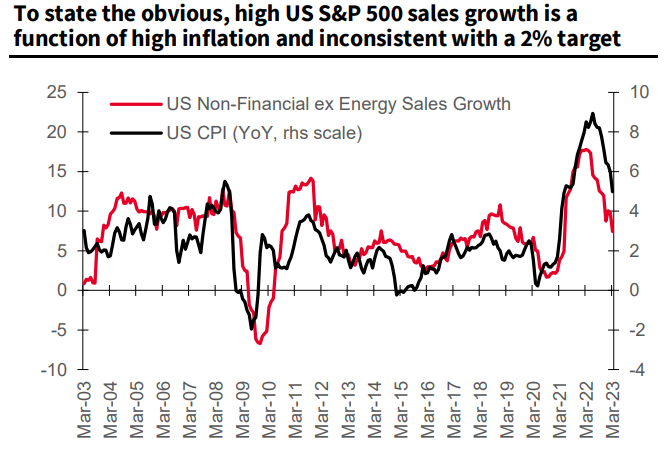

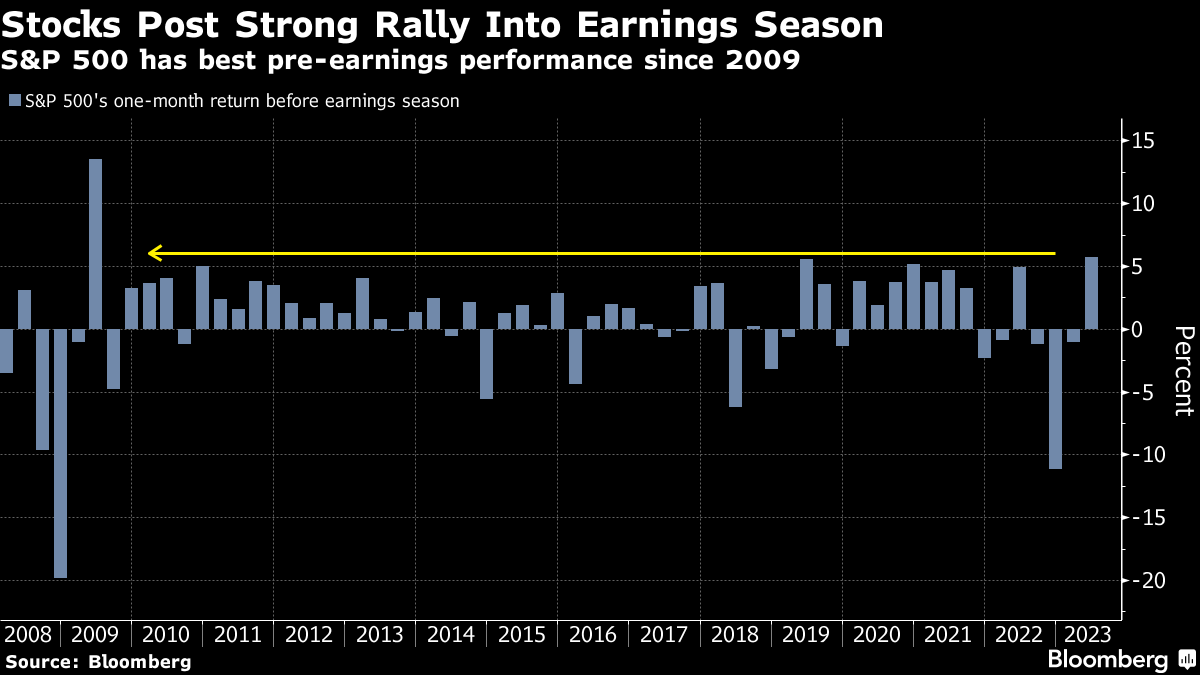

While margins have come under pressure, double-digit profit sales growth has more than compensated for that, Lapthorne said, as exhibited by the fact that revenues are still rising at a rate near 10% in the US, excluding energy. "This is clearly inconsistent with the Fed's inflation target of 2%, which would typically see sales growth in the 3-5% range:"  Source: SG Cross Asset Research/Quant Research, Factset As for the seemingly massive quarter-on-quarter declines in S&P 500 profits that are now projected, a huge chunk of that comes from two sectors that largely gained during the pandemic: technology hardware and pharmaceuticals. "So once again, apparently bearish headline numbers are really envisaging post-pandemic normalization, not a recession," Lapthorne said:  Source: SG Cross Asset Research/Quant Research, Factset What this means for the S&P 500 in the short term is less clear. The benchmark fell in the month leading up to the last two earnings seasons and then bounced back once firms started reporting. This time around, lower interest rates have helped to drive a rally. According to Bloomberg, over the past year, when stocks rose before earnings began, they tended to fall once financial results were delivered, and vice versa. On the face of it, it's unusual for stocks to rally so strongly ahead of a contentious earnings period: For some, like Lisa Shalett, chief investment officer at Morgan Stanley Wealth Management, this is a rally within an ongoing bear market that can be attributed to hopes of an imminent end to the Fed's tightening cycle. But she warns, the uptrend may not last: Leads and lags may be distorted and delayed by the idiosyncrasies of the post-Covid cycle, but critical drivers like the credit and labor market are weakening. No doubt earnings will follow, yet that is not discounted in current prices. The next round of bad news, while potentially lowering short-term yields, will likely be bad for stocks.

That bad news might yet arise from company guidance on earnings calls. If a recession is really coming, as the bond market plainly implies, you'd expect companies to have caught wind of it. That evidence is going to come through gradually. Roughly 26% of S&P 500 companies will have reported by the end of this week and around 60% by the end of next. — Isabelle Lee Getting back to the US and its hegemony, I'd like to recommend a new Survival Tips playlist put together with invaluable expertise from the Bloomberg Opinion social media team. This one is called Americana, and it's a compendium of all the songs about the US, with very different attitudes to it, which was crowd-sourced from Points of Return subscribers when I was celebrating my new American citizenship. You can find it on Apple Music, or Spotify. Whatever the future of the dollar, it's a good bet that America will continue to fascinate musicians. Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close. More From Bloomberg Opinion: Want more Bloomberg Opinion? OPIN <GO>. Or you can subscribe to our daily newsletter. |

No comments:

Post a Comment