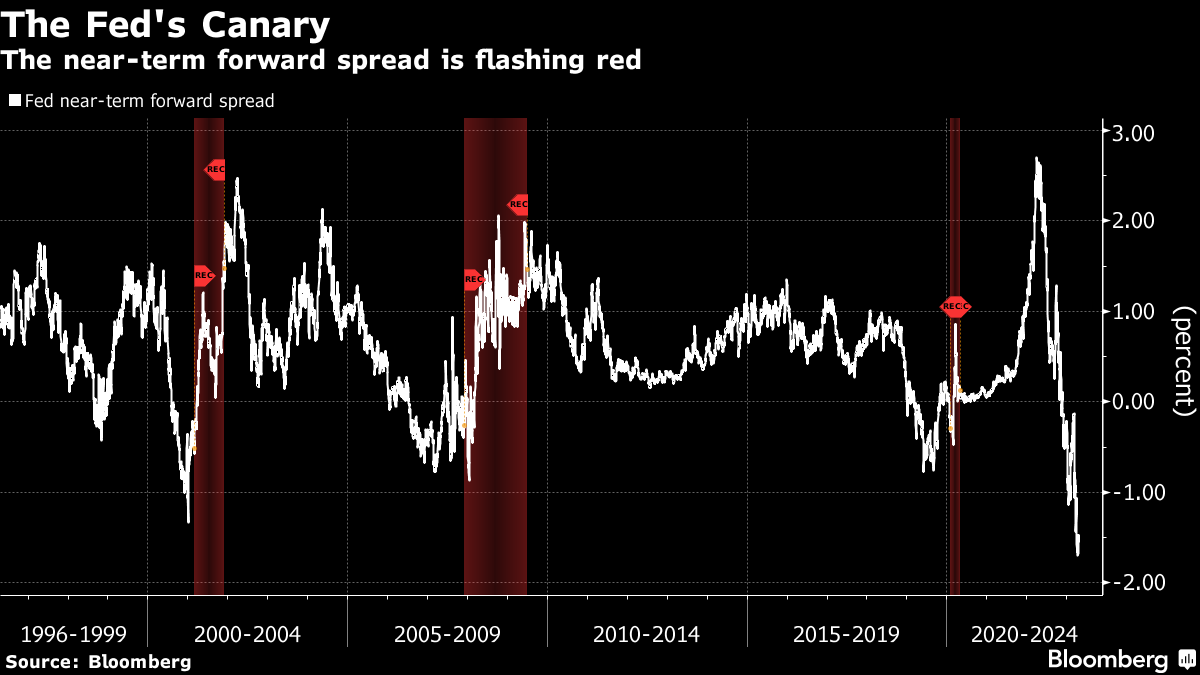

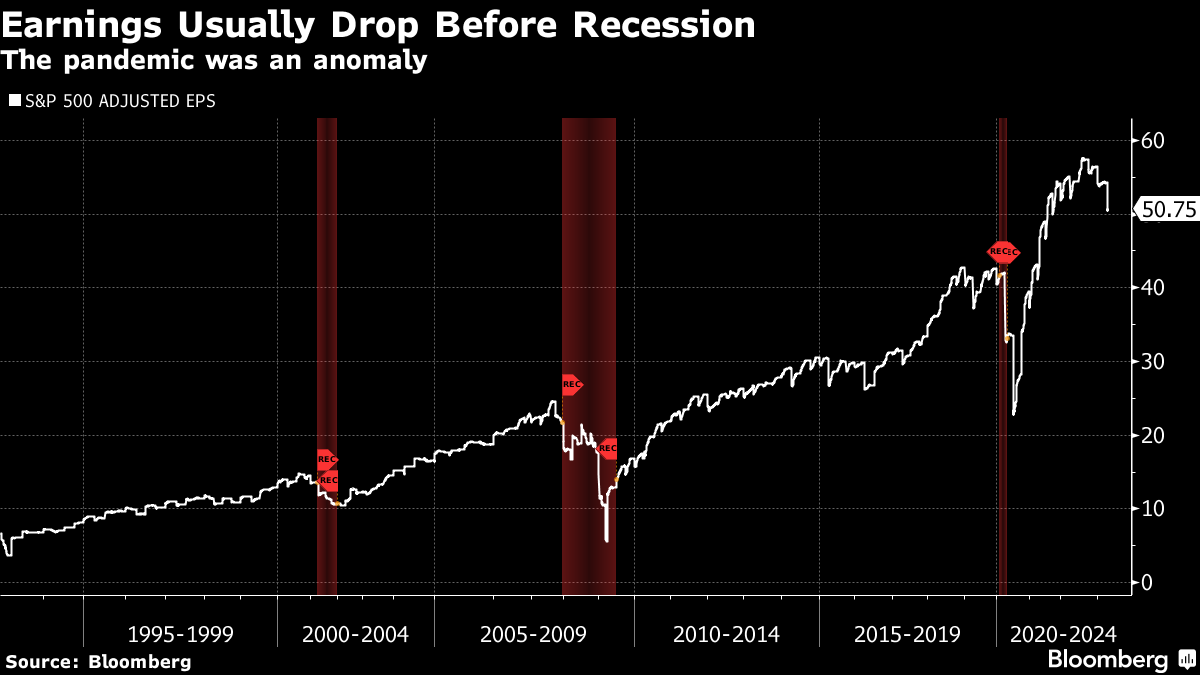

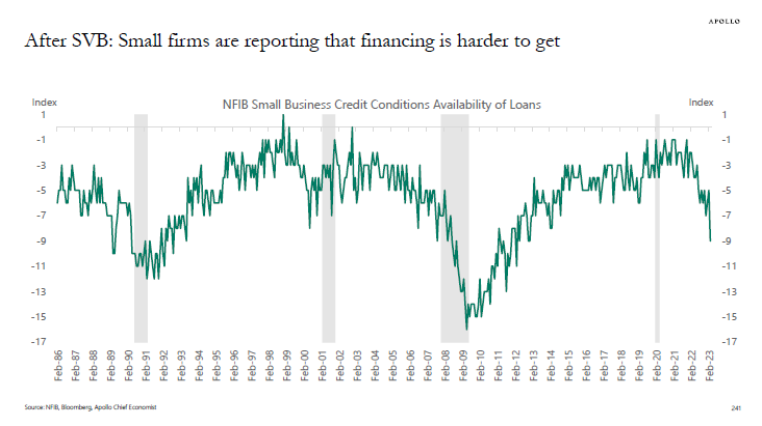

| Are we in a recession right now? Sure, the Atlanta Fed's GDPNow figure suggests the economy grew by 2.5% last quarter. But such numbers get revised and much of that strength was in the earlier part of the quarter. I worry about numbers for March because of what they say about the economy, and because a credit crunch is likely brewing. That mix signals we have to be on alert for a recession, which means lower earnings and lower stock prices. We went through a recession scare just last year. Back then, GDP dipped in the first two quarters of the year, though the labor market was still doing well. Having looked at the three signals for recession, I came to the conclusion that none of those early warning signals was flashing red. It makes sense that the economy eventually strengthened, with the unemployment rate ultimately heading to five-decade lows earlier this year. This time, the data look a lot worse. Take jobless claims for example. My rule of thumb has been that when continuing claims an increase by 200,000 and initial claims by 50,000, a recession is likely. In the past, when this development emerged for more than a couple of weeks, it was always followed by a recession. Right now, continuing claims are up 512,000 from six months ago and nearly 185,000 higher than a year ago. They've been higher than levels seen six months prior continuously for the past four months. That shows many people who are unemployed are staying unemployed, a clear signal of a weakening labor market. Initial claims, which correlate more to non-farm payrolls, have been right around the +50,000 recession level versus the period six months ago for the last three weeks. Year-on-year levels are vaulting higher as well. While it's not a full-on recession signal, it's getting close. Back in June 2022, I looked at the Federal Reserve Chair Jay Powell's preferred recession indicator: the spread between three-month Treasuries and the anticipated three-month rate in 18 months. The spread level, which Powell touted in a post-rate decision press conference, was so high, it was nearly two percentage points above a recession signal — and it made any notion of an economic contraction seem impossible. Now, it's so deeply negative, a recession seems all but inevitable. I also looked at the difference between yields on two- and five-year Treasuries last year, when it was a good 20 basis away from critical levels. Since then, it has inverted by a half percentage point. While such signals weren't sounding alarms last year, they all are now. In other words, the canaries in the coal mine are dying and it's time to make a move because a recession is a matter of when, not if. The employment data will be what locks in a recession, because the loss of employment means a loss of income to support consumption. The number of people who report themselves as unemployed on the household survey tends to rise into a recession (a coincident to leading indicator). For example, the year-on-year increase in unemployment was more than 500,000 for the first time in March 2020, when a recession began. That was also the case two months before recessions in September 2007 as well as in January 2001, and five months prior in March 1990. Right now, there are fewer Americans unemployed than this time last year — but only just. Within the next couple of months, this is likely to flip and a recession will have begun. The timing matters because stock prices tend to rise right up until a recession begins, as investors pile into an increasingly narrow set of market leaders whose earnings haven't been hit. Right now, a market capitalization-weighted S&P 500 index is near year-to-date highs. Looking at the same index in equal-weighted terms, it's almost in correction territory, down 9% from the highs. That signals an increasingly select cadre of giant firms are carrying the market while smaller companies are hurting. |

No comments:

Post a Comment