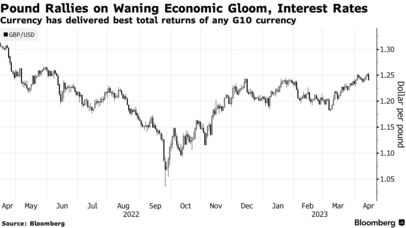

| Andrew Bailey, Governor of the Bank of England, last week raised the prospect of increasing the level of insurance for deposits in the UK, currently set at £85,000. Chancellor Jeremy Hunt followed up with similar comments, in a move that was definitely not coordinated. The recent banking turmoil seems to have finally focused minds: depositors should not lose their money. A blanket guarantee looks very unlikely. But policymakers are working out how to preserve stability at a time when mass bank withdrawals can happen at lightning-fast speed and fears are amplified on social media in a way that would have been inconceivable 15 years ago. Improving deposit insurance will be key. Measures being considered include giving special protection to some funds, such as those used for businesses' working capital. Speeding up payouts — moving from sending out cheques to transferring cash electronically — are also likely to be part of the reforms. John Vickers, one of the architects of the UK's post- financial crisis reforms, told my colleague Philip Aldrick that shielding more client money from bank failures would ultimately expose taxpayers to more risk. Changes could also include getting banks to cough up more to pay into the deposit insurance pot. That won't be popular, particularly among the bigger banks, where the burden would fall the hardest. It could also meet political opposition from the likes of Andrew Griffith, the City Minister. Griffith has been energetically searching for Brexit dividends since taking up his role last year. Today he spoke to Bloomberg's Lizzy Burden about fintechs as a British area of excellence. Those fintechs, the government hopes, will be the golden geese that help create a modern, thriving economy, and lay their golden eggs by listing their businesses in the UK. But some of Griffith's most powerful interlocutors — the big banks — will be keen to impress on him that they are also key to boosting the UK's economy. So piling on the burden of extra funding for deposit insurance, or other measures such as more liquidity to cope with speedy bank runs, could harm that agenda. There are other ongoing difficulties for the government. We could see nurses on strike until Christmas, while teachers are gearing up for walkouts on April 27 and May 2. Against this backdrop, Prime Minister Rishi Sunak is considering an interesting — some might say controversial policy — reducing inheritance tax, as revealed by Alex Wickham this weekend.  Pat Cullen, general secretary of the Royal College of Nursing, center, poses for photographs with striking nurses on a picket line Photographer: Dominic Lipinski/Bloomberg Sunak is also pressing ahead with his campaign to improve the nation's math ability, including considering whether to introduce a new qualification for 16- to 18-year-olds. The aim is hard to argue with, but there are fairly big obstacles, not least attracting enough teachers — who presumably will be pretty good at running the numbers on their chances of buying a house and meeting living expenses on teacher salaries. In more upbeat news, it is deals Monday. International activity appears headed for a spring renaissance, reports Fareed Sahloul. One of those blooms is an approach from private equity behemoth Apollo Global Management to London-listed THG, an e-commerce business formerly known as The Hut Group. THG's founder Matthew Moulding has said he would not recommend listing, so perhaps this or another offer to go private again may be welcome. For the sake of London's future, many will be hoping the wider trend is the other way. Just a few months ago, it was a no-brainer to bet against the British pound, writes Alice Gledhill. But the bleak views are proving to be overstated, at least for now. The pound has roared back this year, delivering the best performance of any major developed currency. Strategists are turning more positive too, with Nomura, NatWest and HSBC saying the rally will continue. |

No comments:

Post a Comment