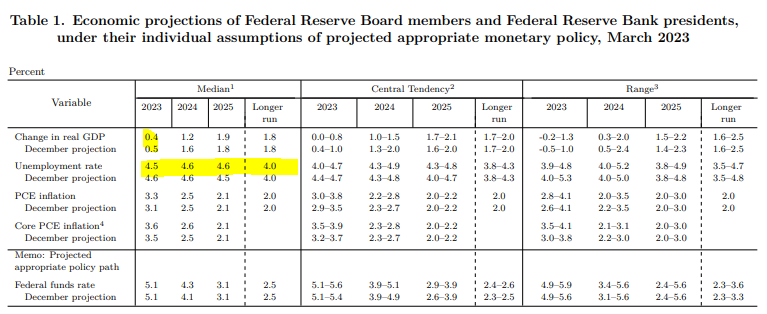

| At the end of February, I was talking about the vibecession not necessarily leading to a real recession. My take then was that the Fed was looking for a Goldilocks outcome for the economy: neither too hot nor too cold for inflation to come down to manageable levels. And I outlined the three potential economic scenarios in that context. The so-called no landing scenario was too hot in my view because it meant a high-pressure economy, sticky inflation and a more aggressive Fed. The silver lining everyone was hoping for in this case was what many of us dubbed the "immaculate disinflation" scenario, where inflation turned down despite a tight labor market and robust consumer spending. But realistically, no landing in 2023 would have made a hard landing later on more likely. This wasn't my base case, but I rated it high. Then there's the soft landing exemplified by the Fed's economic projections, as seen below or on the Fed's website. Unemployment might rise modestly, but economic growth wouldn't necessarily contract on a year-over-year basis. And inflation would come down slowly. While jobs would be lost, this wouldn't be a bad outcome if it means avoiding a hard landing. This is the Goldilocks scenario and I rated it as sort of base case. Then there's the hard landing. It could be induced by either severe, but garden-variety problems of slowing consumer spending, excess inventories and layoffs, like in 1990; or by a full-scale credit crunch and financial crisis, like in 2008. The unemployment rate was as low as 5% in 1989 and 1990, before rising to nearly 8% by mid-1992. Fifteen years later, the economic landing was even harder, with unemployment rocketing up from a low of 4.4% in 2007 to as high as 10% in 2009. These are the outcomes we want to avoid. If you had asked me at the end of February what I thought was likely, my base case would have been on the softish landing, with considerable weight on the no-landing scenario and less on the hard landing. After the SVB collapse, a deeper recession is more likely. "It's the economy, stupid." That's the tag line that James Carville, President Bill Clinton's advisor, came up with to beat George Bush in the 1992 US presidential race. If I had to write a tagline for today, I would say, "it's the credit, stupid." Stress on credit and the financial system could turn a softish landing into a harder landing — and that stress is building. The liquidity crisis associated with SVB's collapse put banks on notice. Either start paying depositors more interest, or face continued withdrawals. Earnings targets for brokerage Charles Schwab were recently cut by 30% by one analyst for this year and next, for example, simply because these pressures would hurt their net interest income. Now, banks are restricting credit as they know that credit distress has begun and loan losses are coming. My colleague Ven Ram recently noted: The spread between high-yield and investment-grade credit widened this month to touch 367 basis points, a differential that has previously proved sufficient for the US economy to enter a recession. The average differential that coincided with the onset of a recession was 354 basis points in December 2007 and 276 basis points in February 2020.

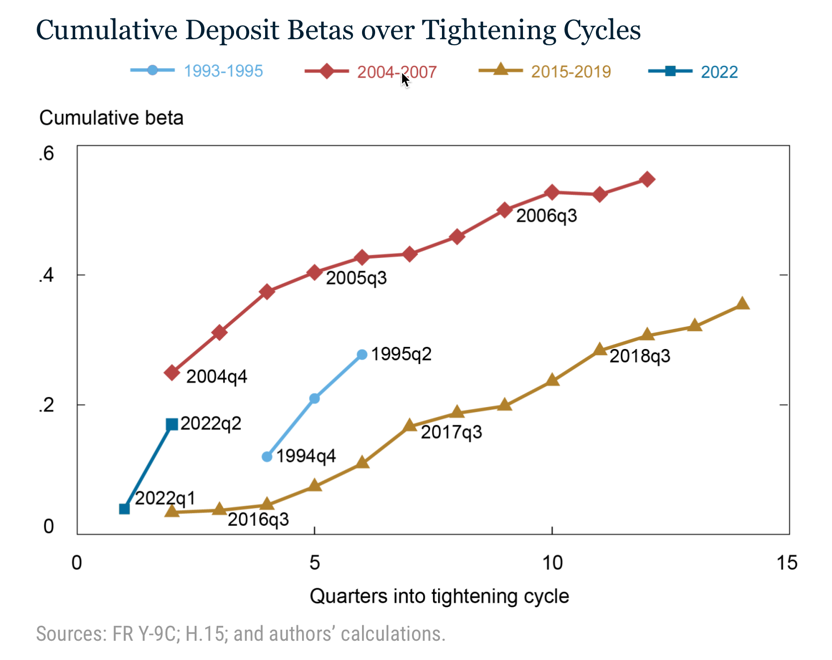

Distressed debt has ballooned to over $600 billion in magnitude. According to Bloomberg Intelligence, distress in junk-rated industrial debt has increased 75% since November. And according to Standard & Poor's, recovery rates are at 30 cents on the dollar or less for more than a quarter of industrial high-yield bonds. As credit constricts, the riskiest borrowers are already being left behind. For example, tech companies are now struggling to get access to leveraged loans. Commercial real estate, as I've mentioned before, is a big problem. See the poor starting position with Manhattan office vacancies climbing to a record, for example. All of the turmoil in credit means more defaults, bankruptcies, liquidations and therefore, job and spending losses. Fears of recession from this sudden restriction in credit are palpable. The question now is not whether the US economy slows but by how much. The big wild cards are: inflation, the Fed, deposit beta (which I will explain below), as well as the potential for credit turmoil in black-swan areas like private markets or commercial real estate. Indicators on the current state of the economy, like the Atlanta Fed's GDPNow figure, show a recession is a long way off. Based on data available through the end of last week, you'd expect the US economy to have been growing by 2.5% last quarter. But with a credit crunch adding to signs of a decelerating labor market, all bets are off. The good thing is that inflation looks like it's headed down enough that we can expect the Fed's rate decision in May to be the end of the line. Reacting to the latest data on Friday, Bloomberg Economics said recent reports provide "a glimmer of hope that the economy is on a steeper disinflationary path." At this point, just one more hike may be coming before the Fed is done. That doesn't mean the Fed will deliver rate cuts priced in by bond markets (and implicitly by equity markets, based on their run-up after SVB.) Cuts are only likely to come with a hard landing, given the Fed's stated views on rate policy. But the data provide some comfort that worst-case inflation scenarios are off the table, easing pressure on the Fed. For banks, the big nugget to crack is so-called deposit beta. The New York Fed, in a November blog entry explained it: The deposit beta is the portion of a change in the fed funds rate that is passed on to deposit rates. For example, if the target fed funds rate is raised by 50 basis points and in response a bank increases its deposit rate 25 basis points, the deposit beta is 50 percent.

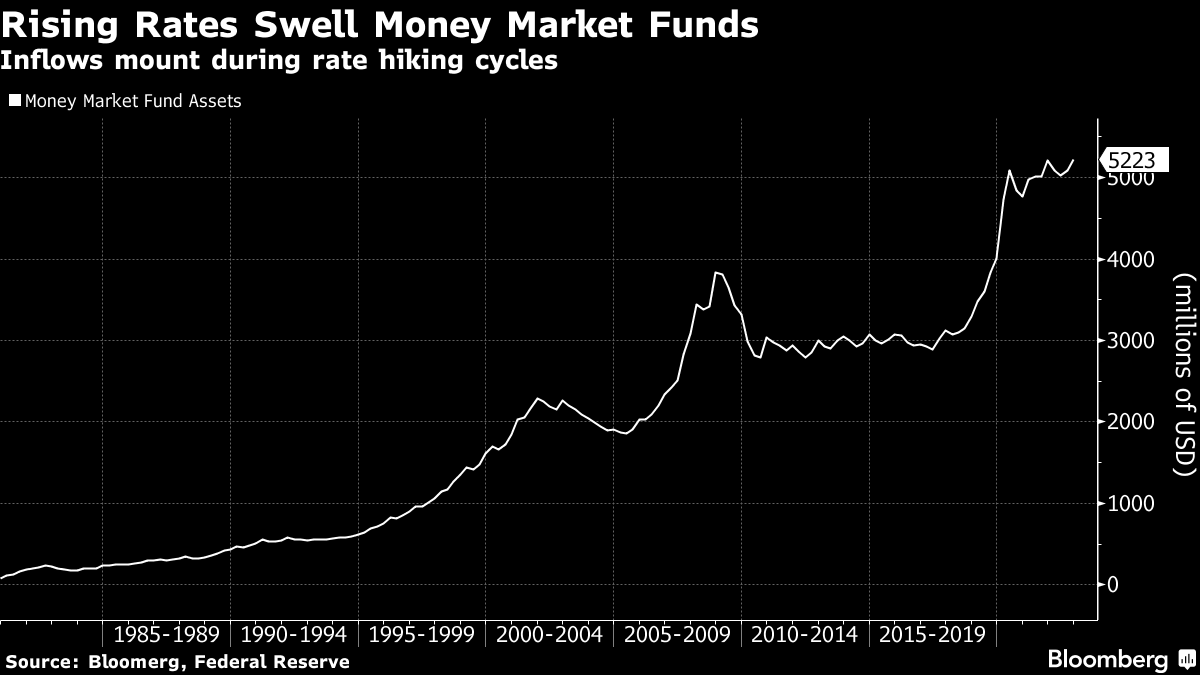

We've had the fastest increase in the fed funds rate in four decades. That's a problem for banks because after the collapse of Silicon Valley Bank — a sort of worst-case scenario in terms of a mass exodus of cash — banks are especially worried this will cause deposit flight. Since many of the assets banks hold are either illiquid or underwater — even so-called risk free assets -- there is therefore a lot of pressure on banks to pass through the Fed's hikes to depositors for fear of the SVB treatment. In that same blog entry, the Fed noted that we are already seeing a fed funds pass-through rate that's more than three times faster than in the last hiking cycle. One top analyst expects another big wave of deposit flight, too. That means shrinking bank margins just as they are about to suffer credit losses from the economy slowing. There are big challenges coming because of the credit situation. The fact that the Fed is less likely to cut rates due to economic weakness than at any time in the last forty years means that stocks will give way when that weakness materializes. Fed officials say they won't use rate policy to smooth out any issues with banks in trouble. But, eventually the Fed is going to have to cut if things deteriorate enough. The fed funds futures market is implying three rate cuts by January of next year. That's a bit too hopeful. For that reason alone, government bonds are less likely to benefit as the economy slows and stocks take it on the chin. However, we should expect to see a big rotation into cash as this plays out given the high yields on offer for low risk cash equivalents like savings accounts, money market funds and certificates of deposit. I remain cautiously optimistic about the US economy, just with a little more caution and a tad less optimism. This isn't a credit crisis like we saw in 2008. It's the end of a cycle with more garden-variety problems like 1990 or 2001. Inflation is the thing that makes this cycle different. I'll stick with my softish landing base case and 3500 year-end target for the S&P 500 for now. Things haven't changed so much for those to give way just yet. My hope is that by the time you read this I'll be on the beach! It's been a hectic couple of weeks and I am looking forward to taking a few days of R&R as this new quarter begins. That means I may not be publishing a column next week — which would make me sad since I have published every week since launching last year! Hopefully I'll find a way to give you a mini-post. |

No comments:

Post a Comment