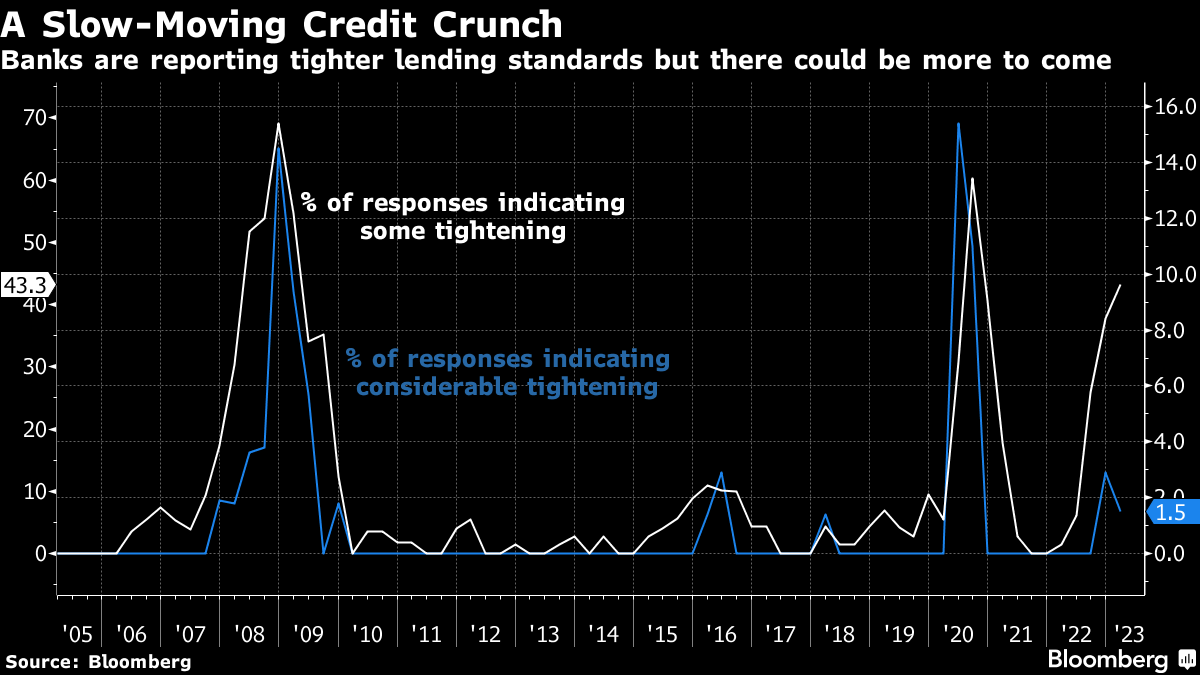

| Hedge funds go all in on the US dollar, First Republic's loans to wealthy homebuyers turn into a headache and investors say tech careers beat those in finance. — Kristine Aquino Hedge funds are betting the dollar is about to reverse its longest stretch of weekly declines in almost three years. Leveraged funds were net short on all major currencies against the dollar last week for the first time since January 2022, according to the latest Commodity Futures Trading Commission data. These wagers notched a win on Friday, after Federal Reserve Governor Christopher Waller said he favored more rate hikes to combat persistently high prices. First Republic's interest-only loans to wealthy homebuyers and property investors have been one of its key challenges to finding investors or a strong lender to take over. The bank is expected to report a $40 billion drop in deposits in first-quarter results due April 24, and its debt portfolio is one of the primary reasons several would-be rescuers aren't willing to pony up cash, according to people with knowledge of their thinking. At the start of this year, First Republic estimated its $137 billion stockpile of mortgages would be worth about $19 billion less than their carrying value if sold off, its annual report shows. Graduating high school students will be best off pursuing a career in tech rather than finance, the latest MLIV Pulse survey showed. For soon-to-be adults, tech is the smartest route despite recent layoffs at Meta, Amazon and Alphabet, according to the 678 professional and retail investors who responded. Even with the rise of artificial intelligence, Andrew Challenger, senior vice president of human-resources consulting firm Challenger, Gray & Christmas Inc., expects tech and finance to remain among the most lucrative careers for the next 20 or 30 years. "I don't see that going away," Challenger said. S&P 500 futures edged higher as of 5:34 a.m. in New York, while Nasdaq 100 contracts climbed 0.2%. The Bloomberg Dollar Spot Index traded near the day's highs, weighing on most Group-of-10 currencies. Treasury yields were little changed across the curve in a quiet day in bond markets. Oil fell while gold rose, and Bitcoin dropped more than 1.4% to below $30k. At 8:30 a.m., we'll get the latest figures on New York state manufacturing, followed by a housing report from the National Association of Home Builders at 10 a.m. The Treasury will publish data on foreign purchases of US securities at 4 p.m. Earnings include Charles Schwab, State Street, and JB Hunt. Here's what caught our eye over the weekend: Utter the dreaded words 'credit crunch' and everyone immediately thinks back to 2008 and beginnings of the global financial crisis. But there's no hard and fast rule that credit crunches have to be cataclysmic, or that they must unfold suddenly and indiscriminately. Credit crunches can be slow-moving affairs -- more of a sinister squeeze than an all-encompassing chomp. And there's some evidence that in the aftermath of March's banking turmoil plus the ongoing effects of higher rates from the Federal Reserve, that's exactly what we're seeing today. We already know, of course, that banks have been more reluctant to lend, with the Fed's survey of senior loan officers showing the biggest tightening of lending standards since the Covid sell-off of early 2020. Meanwhile there are signs that financial intermediaries are scrambling for collateral, which may be one reason why one-month T-bills are now yielding below the effective Fed fund's rate. But given that March's banking crisis was mostly about interest rate risk, it seems reasonable that the most significant strains are destined to appear in bank businesses with the biggest duration exposure. The market for residential mortgage-backed securities (MBS) is a case in point. If you listened to Odd Lots back in October, you know that despite being some of the largest buyers of MBS, banks tend to be reluctant purchasers of these securities in a rising rate environment. And added regulatory scrutiny on banks' rate risk is probably not going to do much to change that. All of which means, that spreads on MBS (the difference between mortgage rates and equivalent US Treasuries) could increase, which potentially means higher mortgage rates even if the Fed doesn't hike. That doesn't necessarily spell disaster for the US housing market given that what we've seen so far is that homeowners are extremely reluctant to sell their homes and take out new mortgages at a higher cost, which has basically already put the market into a deep freeze. But it does highlight the possibility of a slow-moving credit crunch in specific areas of the US financial system. — Tracy Alloway Follow Bloomberg's Tracy Alloway on Twitter @tracyalloway. |

No comments:

Post a Comment