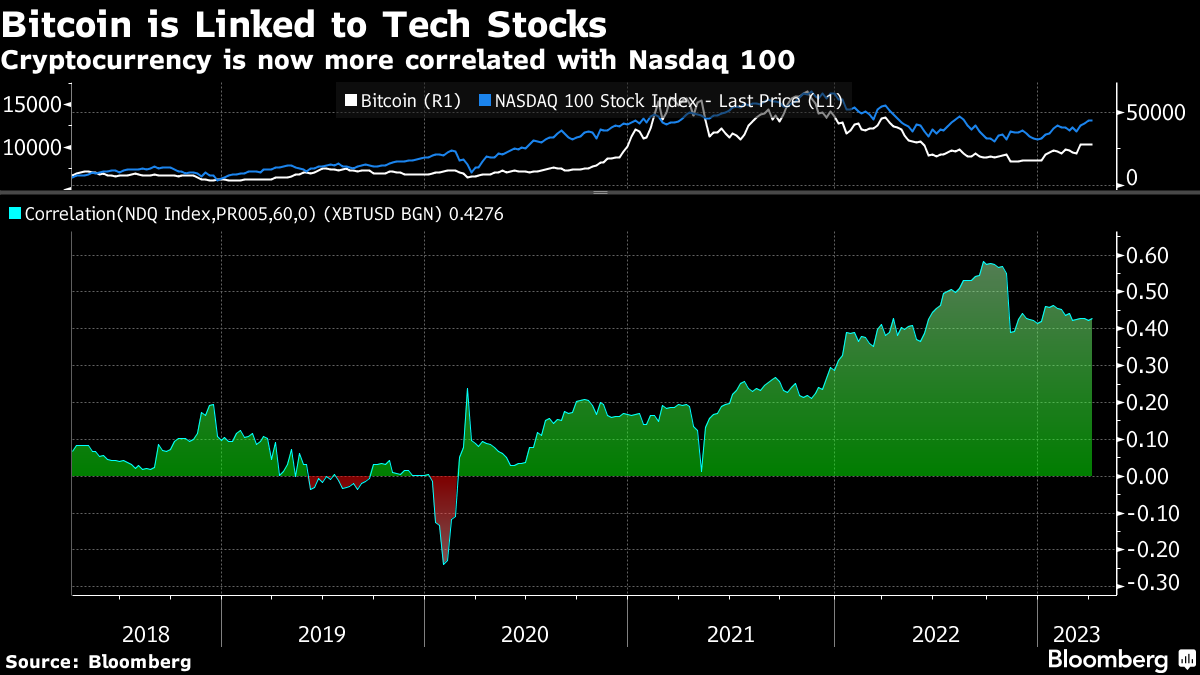

| Good morning. Donald Trump pleads not guilty, a Federal Reserve official warns higher borrowing costs will linger for longer, and Xi Jinping courts Emmanuel Macron. Here's what people are talking about. Donald Trump pleaded not guilty to 34 felonies in an indictment that alleges he used hush money to bury damaging information about an affair and boost his electoral prospects in 2016. Trump, the first former US president to be indicted, was arraigned Tuesday in lower Manhattan, where District Attorney Alvin Bragg had charged him in a broad influence scheme, even as he makes a comeback bid for the White House. Bragg claims Trump falsified business records at his company relating to a $130,000 payment his former lawyer, Michael Cohen, made to porn star Stormy Daniels. Hours later and before hundreds of supporters at his Mar-a-Lago resort in Palm Beach, Trump assailed the 34-count indictment as politically motivated. Federal Reserve Bank of Cleveland President Loretta Mester said policymakers should move their benchmark rate above 5% this year and hold it at restrictive levels for some time to quell inflation, with the exact level depending on how quickly price pressures ease. To put inflation on a steady path down to 2%, monetary policy needs to move "somewhat further into restrictive territory this year, with the fed funds rate moving above 5% and the real fed funds rate staying in positive territory for some time," Mester said at an event Tuesday in New York with the Money Marketeers of New York University. Separately, New Zealand's central bank shocked markets with another jumbo interest rate hike. UBS Group pulled off one of the biggest bank deals ever in a matter of days. But the groundwork had been laid for years. When Colm Kelleher became chairman last April, he inherited feasibility studies by predecessor Axel Weber dating back to at least 2020 on what a takeover of Credit Suisse Group would look like. And early this year, after clients pulled tens of billions of dollars from the Paradeplatz neighbor, Kelleher called on a small group of top advisers from his alma mater Morgan Stanley to ramp up contingency planning, according to people with direct knowledge of matter. The project was top secret and few at the US bank knew what their senior mergers and financial services colleagues were working on with a tight circle of UBS executives, the people said. Xi Jinping is pulling out all the stops for French President Emmanuel Macron as China's leader tries to create some distance between Europe and the US in their approaches toward Beijing. During the three-day visit, which kicks off Wednesday, Macron will have extensive face time with Xi. After formal meetings in Beijing on Thursday, which will also include European Commission President Ursula von der Leyen, Macron and Xi will head to the southern city of Guangzhou. The excursion to meet a world leader at a second location outside the capital is rare for Xi, who normally reserves such honors for close friends like Russian President Vladimir Putin: In 2018, they took a high-speed train to Tianjin east of Beijing and watched a hockey match together. European shares may struggle for traction as concerns over US banks linger. UBS holds its annual general meeting in Basel. Poland's central bank delivers a rate decision. ECB chief economist Phillip Lane speaks in Cyprus. Services and composite PMI data are expected for countries including France, Germany and Italy. Sodexo, Industrivarden and Barry Callebaut are on tap for earnings. This is what's caught our eye over the past 24 hours I'm working on Good Friday. I'm working because, for reasons I don't fully understand, the US Bureau of Labor Statistics has decided to release the Employment Situation Report, which captures such numbers as the change in nonfarm payrolls, average hourly earnings and the unemployment rate in the world's largest economy at a time when most stock markets are closed. I volunteered because this one has me worried. Traders unable to trade when big news lands, then left to fret about what other traders are thinking, is a recipe for pent-up frustration and wild volatility when markets reopen after a weekend of varying lengths in various jurisdictions. That'll be amplified, of course, if the numbers deviate wildly from expectations. Data only move prices when the readings differ from what market participants expect. The best outcome for everyone is probably if it lands exactly in line with current forecasts. If it doesn't though, there are a few places we can look to see how the hive mind is reading the tea leaves. First, there's FX markets. Currency traders will be awake and at their Terminals. Yet a spike in the dollar could mean (A) The US economy is strong and inflation will stay hot forcing the Fed to hike rates faster and higher; or (B) the US economy is weak and haven demand is driving people to the dollar. Not much help, then. Treasury yields (with bond markets open for part of the day) will give a better read. A steepening of the yield curve, with front-end rates falling relative to later ones, means slowing growth, lower inflation and a lower peak Fed rate. Probably. IG's Weekend Wall Street, a contract for difference based on the Dow Jones Industrial Index might give a flavor of what stock traders think. But my favorite indicator of risk appetite when markets are closed is Bitcoin. It is a relatively pure expression of animal spirits. And greater integration in financial markets means that it now trades alongside other risky assets. From virtually zero a few years ago its correlation to the Nasdaq 100 has risen to 0.4 (measured on a weekly basis over the last two years). Liquidity is relatively deep compared with other weekend venues, it trades in most jurisdictions, and, let's face it, it's fun to watch. Eddie van der Walt is Deputy Managing Editor of the Markets Live blog on the Bloomberg Terminal, based in London. Follow him on Twitter at @EdVanDerWalt |

No comments:

Post a Comment