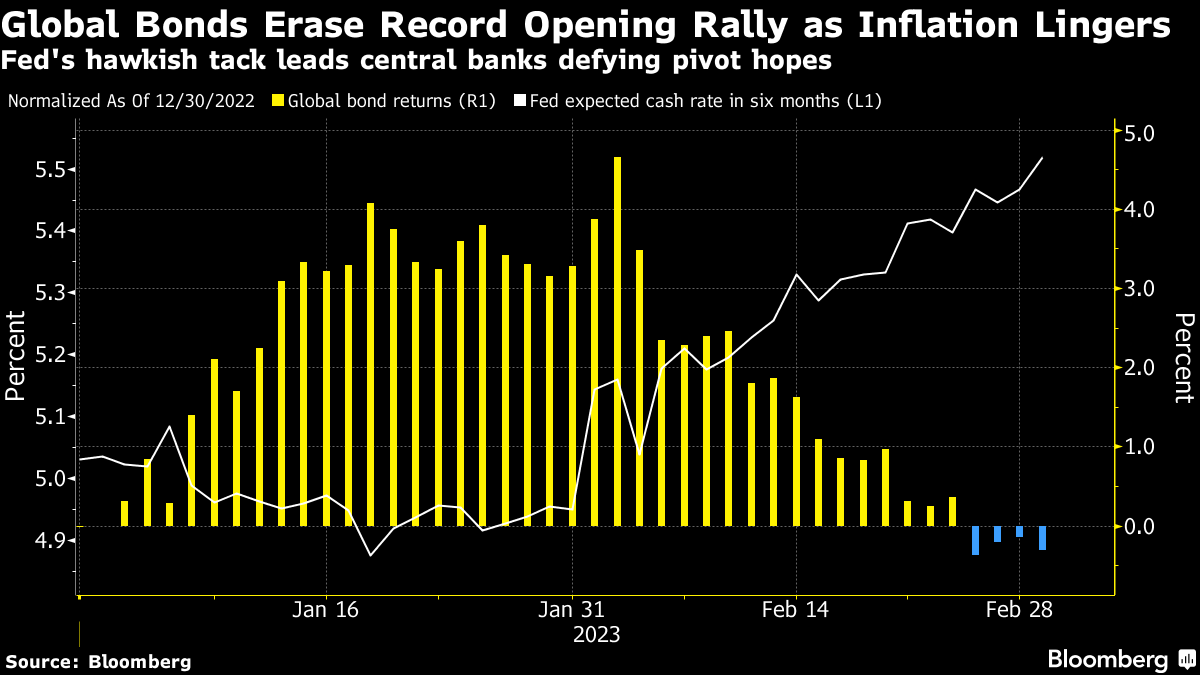

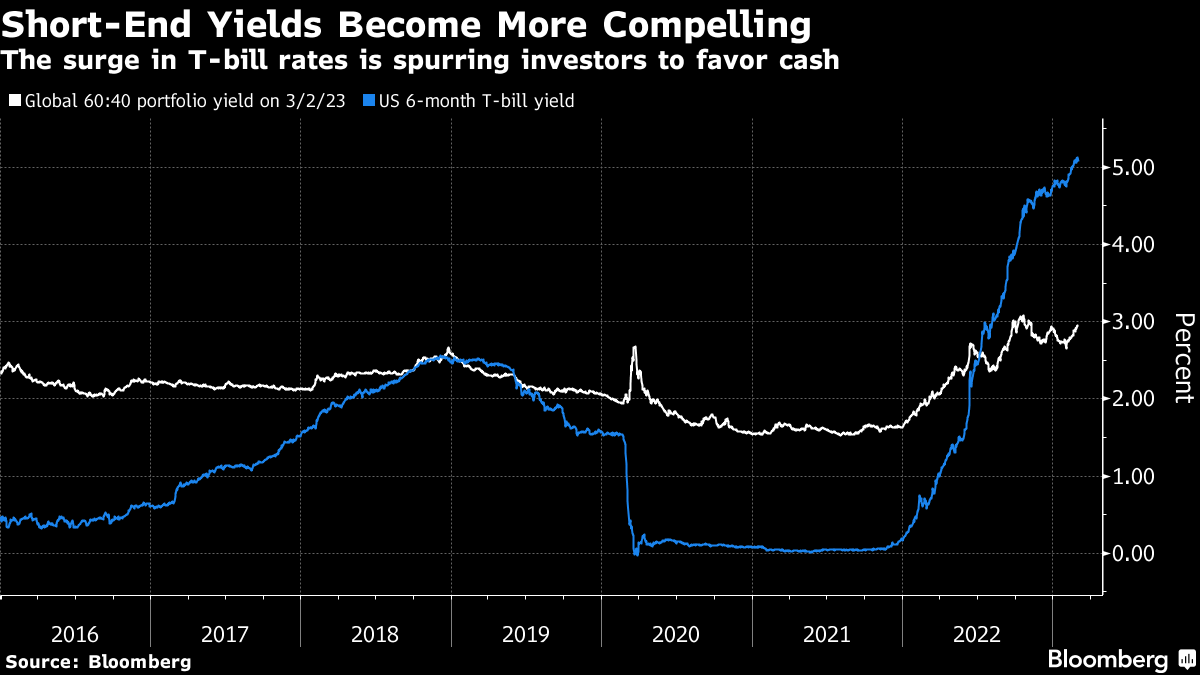

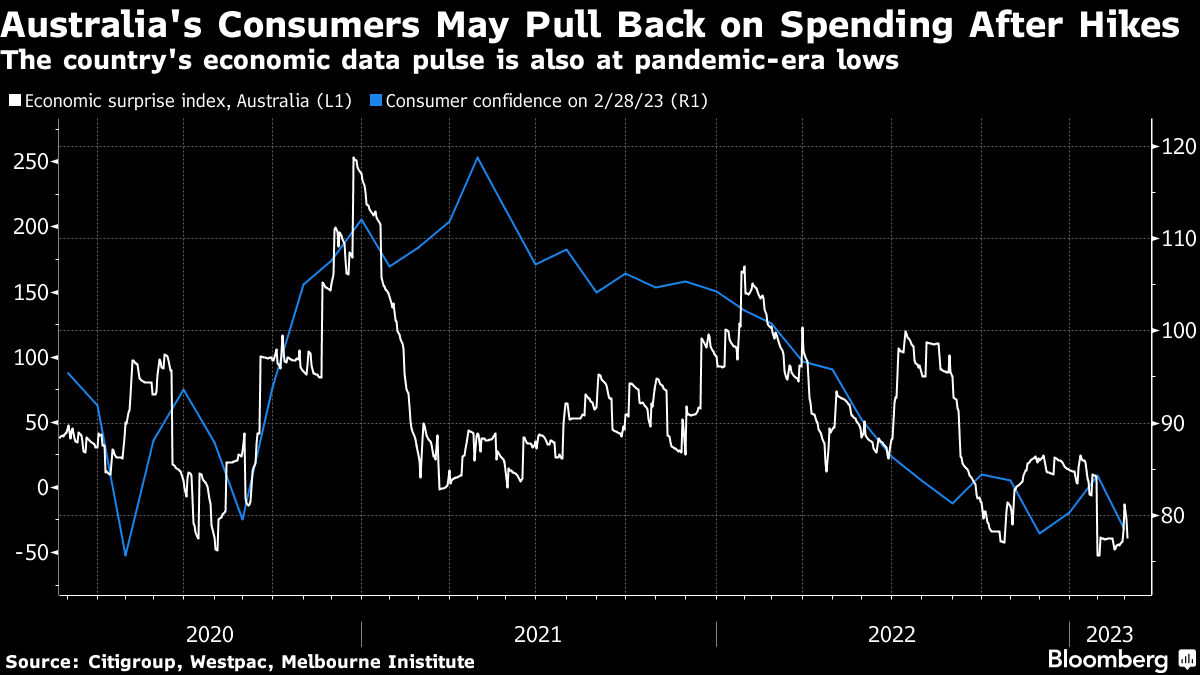

| Welcome to the Weekly Fix, the newsletter that expects to stay elevated throughout 2023. I'm Bloomberg's chief rates correspondent, Garfield Reynolds. The whole Treasury market moved to yields above 4% as a relentlessly robust US data pulse met a similarly robust rhetorical response from policymakers. Federal Reserve Bank of Atlanta President Raphael Bostic, currently deemed on the dovish side by Bloomberg's spectrometer, is mulling whether the US cash rate will need to go beyond the 5% to 5.25% range he has endorsed as necessary to tame cost pressures. Markets are already pricing in strong odds for a 5.5% peak, and they've backed away from the expectation that the Fed will pivot to rate cuts this year to favor the idea it won't ease policy before 2024. Meanwhile, the trader who bet big in early February on a 6% cash rate has begun unwinding the position, which has already doubled in value since it was put on. That number four cropped up again in Europe. For the first time, investors boosted bets on the ECB's peak interest rate being higher than 4% after inflation in France and Spain came in unexpectedly hot. Core CPI growth for the euro area came in at a record high later in the week to underscore the case earlier laid out by the central bank's Chief Economist Philip Lane. He said the ECB might hold borrowing costs at a high level for some time once they reach their peak. It all made for a rough start to March after February saw investors hit the sell button across assets. Tumbling bonds completely unwound the gains they made during the market's best January on record. All the same, the fact that yields are at the highest level in a decade keeps investors clinging to the hope of a strong bond-market rebound at some stage in 2023. There's also the consolation of the actual income now on offer. For the first time in more than two decades, some of the world's most risk-free securities are delivering bigger payouts than a 60/40 portfolio of stocks and bonds. Short-end yields may also get an extra fillip as the US Treasury Department is on the cusp of once again slashing the amount of bills floating around, potentially creating ripples in funding markets as investors chase a dwindling supply of securities or hunt for other places to stick short-term cash. Tokyo's policymakers, current and future, look like they are willing to fight a rearguard action to resist the global hawkish wave. That's the message investors took away from hours and hours of testimony from Kazuo Ueda, the government's choice to take over in April once Bank of Japan Governor Haruhiko Kuroda steps down after a decade in charge. The inertia in the country's bond market is so cloying that traders are apparently clamoring for the chance to make 0.01% or so on a deal. A case in point: this week's 10-year note auction, where investors offered to buy almost eight times more debt than was on sale. That's a level of demand last seen in 2005. The surge in offers came as traders forecast some of the securities would price at 0.01% below the price consistent with the BOJ's 0.5% yield cap. Then, the thinking went, traders could flip them to the central bank for a minimally higher price. Japan's central bank has a standing daily operation in place, offering to buy unlimited amounts of 10-year notes at a fixed yield of 0.5%. Instead the sale went off at exactly the BOJ's target level. Growing signs of economic pain from all those rate hikes are also prompting investors to eye bonds. US home prices recently dropped year-on-year for the first time since 2012. UK properties were already sliding, but now prices are declining at the fastest pace since 2012. Oh, and Swedish bankruptcies increased for a seventh month. Australian central bank chief Philip Lowe's expectation of further rate rises is prompting economists and money markets to narrow the odds of a recession in the $1.5 trillion economy. This week brought surprisingly slower economic growth and monthly inflation data Down Under to fuel fresh speculation the RBA may need to reconsider its recent aggressive shift. India's economy also fared poorly at the end of 2022 and Mexico's central bank trimmed its economic growth forecasts for this year and next, after raising borrowing costs more aggressively than expected in February. The bond market thinks this economic bad news is just getting started. - Sotheby's pitching bonds backed by individuals' art collections

- Private equity firms are using some of their companies as ATMs again

- Direct lenders see a chance to grab market share in leveraged buyout loans

|

No comments:

Post a Comment