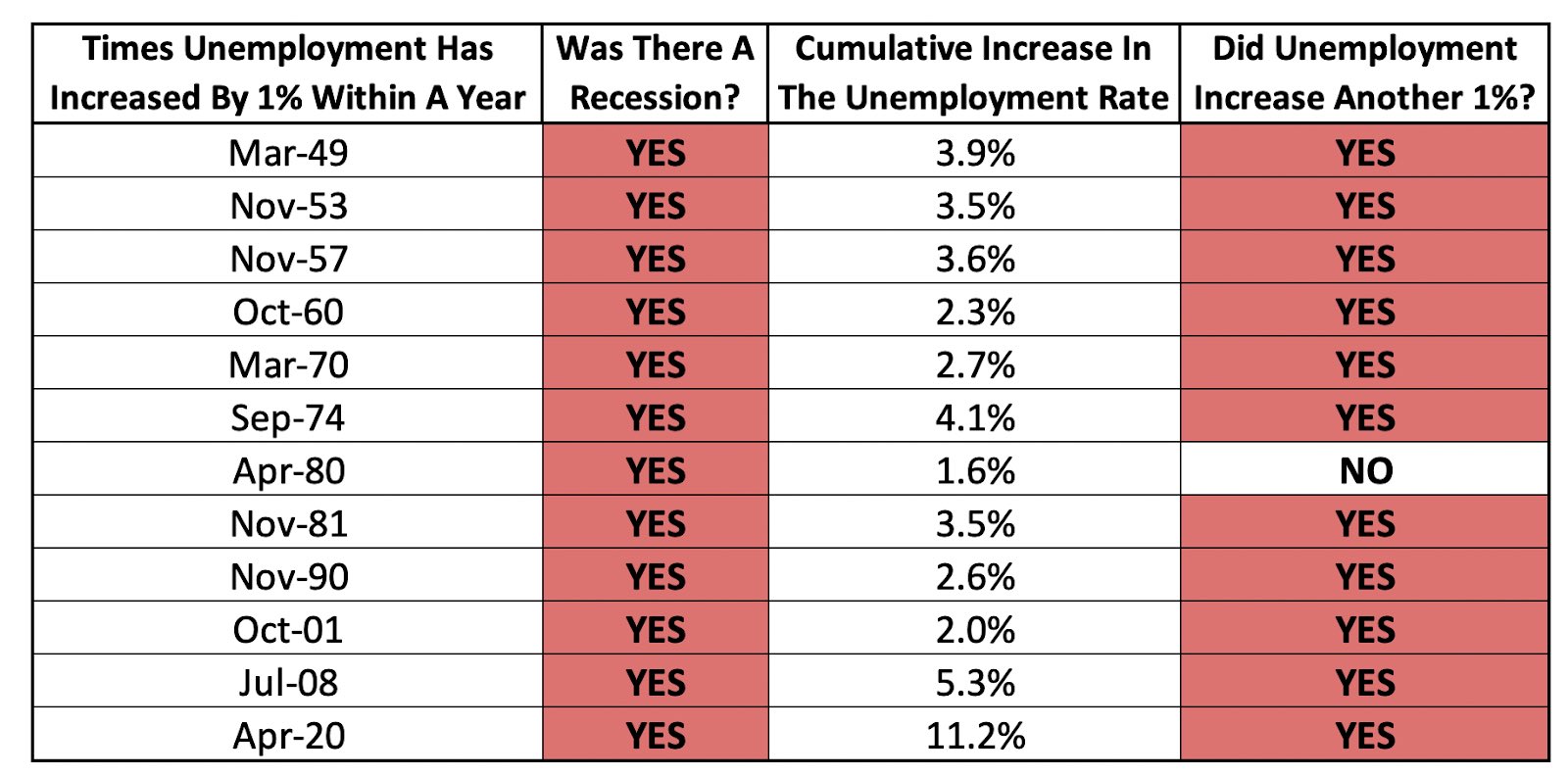

| Federal Reserve Chair Jerome Powell's testimony ripples across markets, bond investors double down on recession bets and tensions simmer between the US and China. — Kristine Aquino After Fed Chair Powell's testimony to US lawmakers roiled markets globally, investors are taking stock of the fallout. There's "a reasonable chance" the US central bank will have to raise its key rate to 6% and keep it there for some time, Rick Rieder, chief investment officer for global fixed income at BlackRock said. Meanwhile, Ken Griffin, the billionaire founder of Citadel and Citadel Securities, said the setup for a US recession is unfolding and that the Fed needs to raise rates further to combat "traumatic" levels of inflation. The bond market is doubling down on the prospect of a US recession after Powell's remarks as traders brace for a full percentage point of rate hikes over the next four Fed meetings. The yield on two-year US notes exceeded its 10-year counterpart by the most in more than four decades — a development that has generally preceded economic downturns by 12 to 18 months. "It is hard to deny the hawkishness of the statement and the message that markets took away," strategists at NatWest Markets wrote in a note to clients. China's Xi Jinping struck a more critical tone toward the US at this week's National People's Congress, calling on the private sector to help overcome "comprehensive containment and suppression by Western countries led by the US." He strengthened oversight of his nation's $60 trillion financial system by creating a new agency to manage data, just as the US steps up efforts to prevent Beijing from obtaining advanced technology. "National security concerns have brought the issue of data protection to the fore, on both sides of the divide," said Tiffany Tam and Robert Lea, analysts with Bloomberg Intelligence. "While there are genuine concerns, the issue is becoming increasingly politicized." S&P 500 futures edged higher as of 5:27 a.m. in New York, after the cash index slid 1.5% on Tuesday. The Bloomberg Dollar Spot Index was little changed near the highest in more than two months, leading to mixed trading in Group-of-10 currencies. Treasury yields climbed across the curve, pulling global bond markets along with them. Oil rose while gold and Bitcoin fell. At 7 a.m., we'll get mortgage applications data, followed by the ADP employment report at 8:15 a.m. and JOLTs job openings figures are 10 a.m. Powell is due to speak to House lawmakers from 10 a.m. Before that, Richmond Fed President Thomas Barkin is due to speak at an event at 8 a.m. The US will sell $32 billion of 10-year notes at 1 p.m. In Canada, the central bank is due to deliver a rate decision at 10 a.m. New York time. Here's what caught our eye over the past 24 hours: Jerome Powell testified in front of the Senate yesterday, and it turned out to be a newsmaker. Markets fell after the Fed Chair unambiguously opened the door to a faster pace of hikes. This comes not long after stepping down to a 25 bps move, so it's a notable acknowledgment of the seeming reheating of the economy that's taking place. There were some other interesting questions about things like childcare, crypto, climate, and whether the dollar's status as a global reserve currency was an unambiguously good thing. (That last one, in particular, was Freshman Senator JD Vance's first question to the Fed Chair, and he likened the global demand for dollars as a de facto 'resource curse' or Dutch Disease. Anyway, it was a little bit more creative and intellectual than the typical elected official question.) And then there was Elizabeth Warren, and because it was Elizabeth Warren, a bunch of people freaked out about it. The Senator posted the whole clip to YouTube here. There were two parts to the question, and it was the first part that got most of the attention. It was basically: 'What do you say to the 2 million people who you plan to put out of work with your rate hikes?' That's a totally a legitimate question. Under the Fed's summary of economic projections (released last December), appropriate monetary policy would cause the unemployment rate to rise to 4.6%. As Warren notes, that's roughly 2 million people. Now the Fed, of course, has a legal mandate to constrain inflation. And its tools aren't particularly nimble, as everyone knows. But it's still a fine discussion to talk explicitly about what the costs are (and who is expected to bear them) of getting back to 2% inflation. Anyway, the second part of the Warren question didn't get as much attention, but it was something that should be top of mind for investors actually. Go to the 3:15 mark of the video. Basically the question was, once the Fed gets unemployment up to 4.6%, would it really stop there? As Warren put it: "Once the economy starts shedding jobs, it's kind of like a runaway train." And she is right. As Alex Williams at Employ America noted in a blog post earlier this year, since WWII there have been 12 times that the unemployment rate rose by at least 1% in a year. And 11 out of 12 times, the unemployment rate increased by at least 1 percentage point more. So even setting aside what you think of asking the Fed chair about the employment costs of the tightening, it's definitely a good question to ask about whether the Fed can stop the layoffs when they really gather steam. It's also a timely discussion to be having in a big week for labor market data. Today we get ADP and JOLTS. Tomorrow, we get initial claims, and then Friday is the non-farm payrolls report. It's worth noting that while the market still seems tight and strong, some of the private sector measures are starting to turn. Yesterday, Nick Bunker at Indeed noted that job postings to the site continued to drop notably. Meanwhile the rate of hiring is also slowing per LinkedIn. Who knows what this batch of data will bring. But if/when the labor market begins to turn at some point, then you should take heed of Elizabeth Warren's question, and the momentum of unemployment once it gets going. Meanwhile, the curve inversion is getting wild. At roughly negative 106, the 2-10 spread is now the most inverted since September 1981, implying that at some point out there, we're gonna be seeing some pretty fast rate cuts whenever things turns around. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart. |

No comments:

Post a Comment