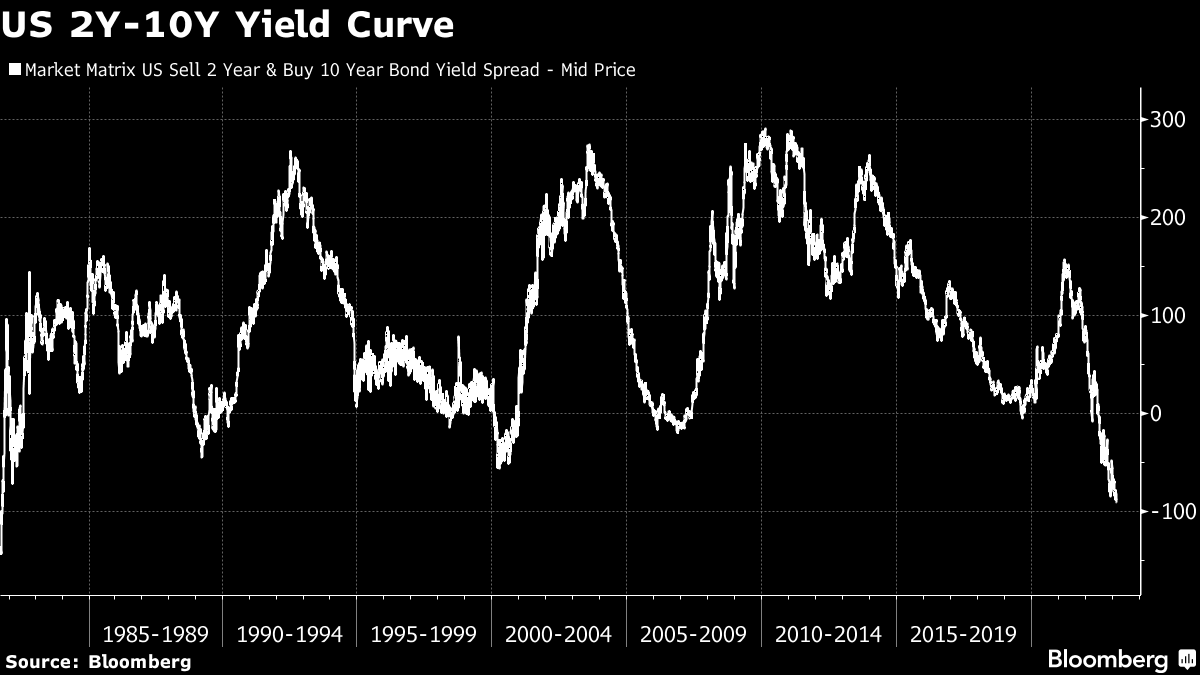

| Goldman Sachs fails to impress investors, China's economy rebounds after Covid Zero and the wealthy hunt bargains in real estate. — Kristine Aquino To catch up on the trading day in the UK and Europe, check out Markets Today. Goldman Sachs shares slid even after top executives touted the firm's strengths at the bank's investor day on Tuesday. Chief Executive Officer David Solomon got visibly flustered as analysts pressed him to explain the apparent divergence between promising to scale up operations such as credit cards and installment lending, while signaling parts could also be sold. "This is an albatross around Goldman's neck," Gerard Cassidy, a banking analyst with Royal Bank of Canada said of the consumer business in an interview, adding that it was disheartening to hear that it's not going to break even until 2025. China's economy is showing signs of a stronger rebound after Covid restrictions were abandoned. Manufacturing posted its biggest improvement in more than a decade, services activity climbed and the housing market showed signs of stabilizing. The figures come ahead of next week's National People's Congress, where a new growth target will be disclosed. In the run-up to the event, President Xi Jinping moved to consolidate the Communist Party's hold over the economy and said it would roll out plans for " deepening structural reform" in the financial sector and exercise more control over science and technology work.  | Wealthy individuals, family offices and closely held companies spent a combined $455 billion last year on commercial real estate, according to Knight Frank's 2023 Wealth Report. They were the most active buyers in the sector annually for the first time, the London-based broker said in the report, released Wednesday. That's a stark contrast from institutional investors, who pared their share of the $1.1 trillion market for offices, logistics sites and rental housing. "Private buyers are taking advantage of the ongoing repricing of assets and stronger currency positions," Alex James, Knight Frank's head of private client advisory, said in a statement. S&P 500 futures climbed about 0.3% as of 5:53 a.m. in New York, while Nasdaq 100 futures rose 0.4%. The Bloomberg Dollar Spot Index traded near the day's lows, boosting most Group-of-10 currencies. Treasuries edged lower, mirroring moves in Europe. Oil fell, while gold gained with Bitcoin. At 7 a.m., we'll get MBA mortgage applications data, followed by the latest reading of S&P Global's manufacturing gauge at 9:45 a.m. and construction spending and ISM manufacturing figures at 10 a.m. Federal Reserve of Minneapolis President Neel Kashkari is due to speak at 9 a.m. Earnings include Lowe's, Dollar Tree and Kohl's. Tesla is due to hold an investor day. Here's what caught our eye over the past 24 hours: For a while, the market was betting on imminent Fed rate cuts, possibly starting as soon as later this year. The expectation was either that there was going to be some kind of recession that caused cuts, or that maybe they would make sense in the context of a soft landing. Anyway, it looks like that's gone for now. The 3M-2Y portion of the yield curve has almost totally un-inverted. This is in keeping with our new "higher for longer" and "no landing" times. But what's interesting is that while one curve un-inverts, another curve's inversion gets deeper and deeper. The 2Y-10Y spread is now at -90.4. That's a level we haven't seen since October 1981, more than 40 years ago. Of course, this is the part of the curve that for years people have generally talked about as having recession-predictive power. Now setting aside whether that's true, or why it would be true, it's arguably still flashing a deep red, perhaps signaling that ultimately the tightening the Fed will have to do to kill inflation will induce that recession after all. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart. |

No comments:

Post a Comment