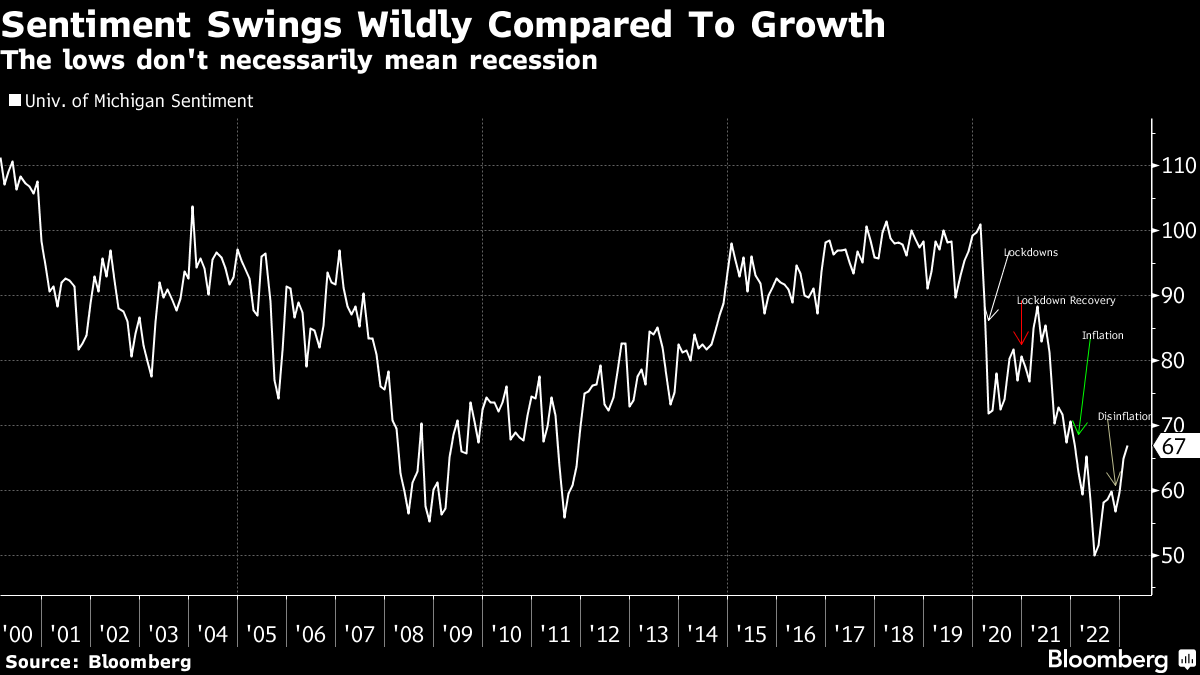

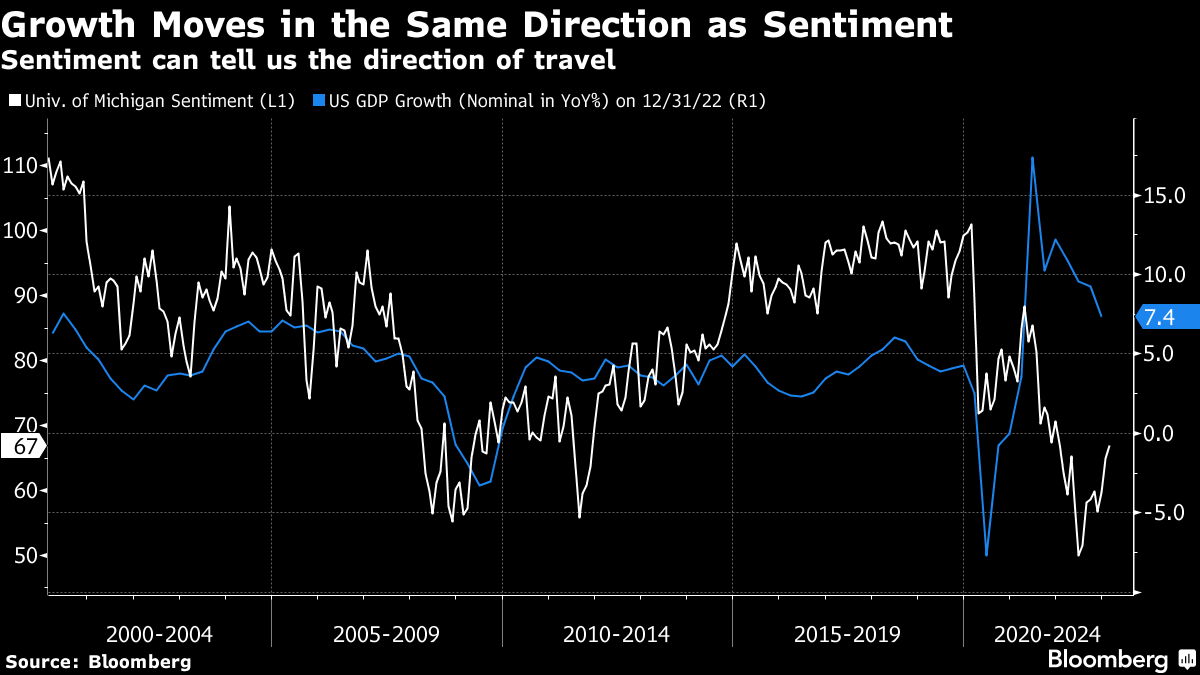

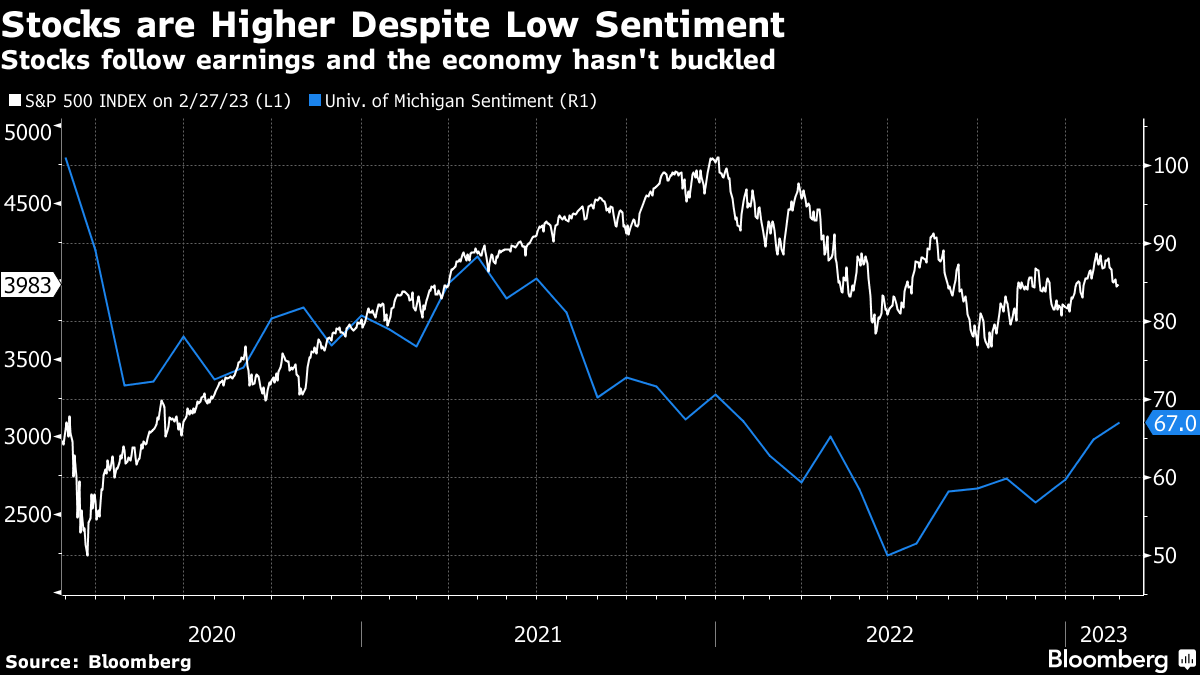

| Since the pandemic, consumers have been pretty pessimistic. And that's understandable. It's a pandemic after all. What's there to be happy about? Still, once people started getting the vaccines, which meant an end to lockdowns and huge infection waves, you would have thought consumer sentiment would pick up. And it did for a while. But then the supply chain issues and inflation crushed hopes and consumer sentiment drifted down to lows in June. Inflation has come off the boil since then and consumer sentiment with it. But the levels are still pretty low. Here's my question: does a vibecession, that sense that all is going wrong, lead to an actual recession? I've been looking at the data and the conclusion I've come to is that vibecessions don't necessarily translate to real recessions. It's basically a difference between soft data and surveys on the one hand and hard data based on sales and spending on the other. In short, there's a wide gulf between what consumers (and businesses) say and do — and that may be the economy's saving grace. So, despite persistently low consumer sentiment — and business sentiment -- readings, I think the US (and global economy) can escape the post-pandemic period with a softish landing if everything goes right. That will be good for both stocks and bonds and most risk assets — though we'll likely have to wait until next year to see it. I'll show you the data and explain my thinking below, with a little help from my London colleague Kristine Aquino to get a gut check from across the pond. Here's the data I want to look at: The University of Michigan Consumer Sentiment Index. We've had four distinct periods in consumer sentiment since the pandemic started. First there was the cliff dive as we went into lockdowns in the Spring of 2020. Then there was a choppy recovery for a year until inflation started to really bite in the Spring of 2021. Sentiment fell off a cliff and reached its nadir last June as inflation was everywhere. But since then, sentiment has recovered but is at levels still below where it was when we went into lockdowns. None of this matches up with any economic data I looked at — not personal consumption, not GDP growth and not inflation. Even business sentiment in things like purchasing managers indices or the regional Fed indices has been consistently poorer than the hard data. And looking further back into the past, swings in sentiment readings are more pronounced than the change in hard data, with a huge dip in sentiment during the debt ceiling crisis to levels as low as during the Great Recession a few years earlier. When the summer of 2022 began, we were even lower. So the first thing to take away from soft data, from sentiment, is that it doesn't necessarily translate precisely into spending or economic growth. It can but it doesn't have to. What it can tell us is the direction of travel, whether GDP growth is generally headed up or down. You can see that when you overlay the year-over-year rolling change in GDP. That change in economic growth isn't as wild as sentiment and the sentiment can't predict a recession, but the two move mostly in the same direction. Rather than pull up a bunch of economic data charts on things like pending home sales, let me use one chart to sort of encapsulate everything — the Citi Economic Surprise Index. Zero is the dividing line between an economy with more upside surprises and one with more downside surprises. The higher the index is, the more upside economic surprises we see relative to expectations. What we see there is that for the first time since the fall, data are surprising to the upside. One way to look at the recession predictions, then, is as an extrapolation of the trends that bottomed in the early summer of 2022. With the Fed raising interest rates at a hefty ¾ of a percentage-point pace, extrapolating more downside made sense. But now that things have turned, does it make as much sense to extrapolate more upside? I don't think it does — simply because the Fed's medicine is still working its way through the system. Let the central banks pause first and then we'll see. Some people are talking about a "no landing" scenario like that's a good thing. But think of the Fed (and, therefore, the economy and asset markets) as being like Goldilocks. They don't like things too hot or too cold, and a no landing outcome — as good as it sounds — would almost certainly be too hot. A cold economy, or a hard landing, is where we get a deep recession like we had from late 2007 to early 2009. No one wants that — it's bad for employment and its bad for asset markets too. The Fed is actively trying to avoid that outcome. But "no landing" in 2023 is akin to a hard landing sometime later simply because inflation is too high to think we can just drift down. Plus the Fed won't relent in that situation with rate hikes when we are closing in on a 70-year low in unemployment. That's a case of the economy running too hot, overheating in a way that spills over into wild meme-stock speculation and inflation, which hurts those with the lowest incomes the most. The Fed has always said it would work against that scenario. What Fed Chair Powell is trying to do is find a middle ground between the policies of the 1970s and the crushing interest-rate hikes of Paul Volcker. His hope has been what he calls a "softish" landing. That likely includes a mild recession during which unemployment rises. And that's because, by definition, a "softish" landing has to be different than no landing. The unfortunate aspect of that so-called softish landing is that unemployment never just ticks up a tad, it always shoots up in a recession. So we'd go from 3.4% to 5% in no time if that's the outcome they're striving for. |

No comments:

Post a Comment