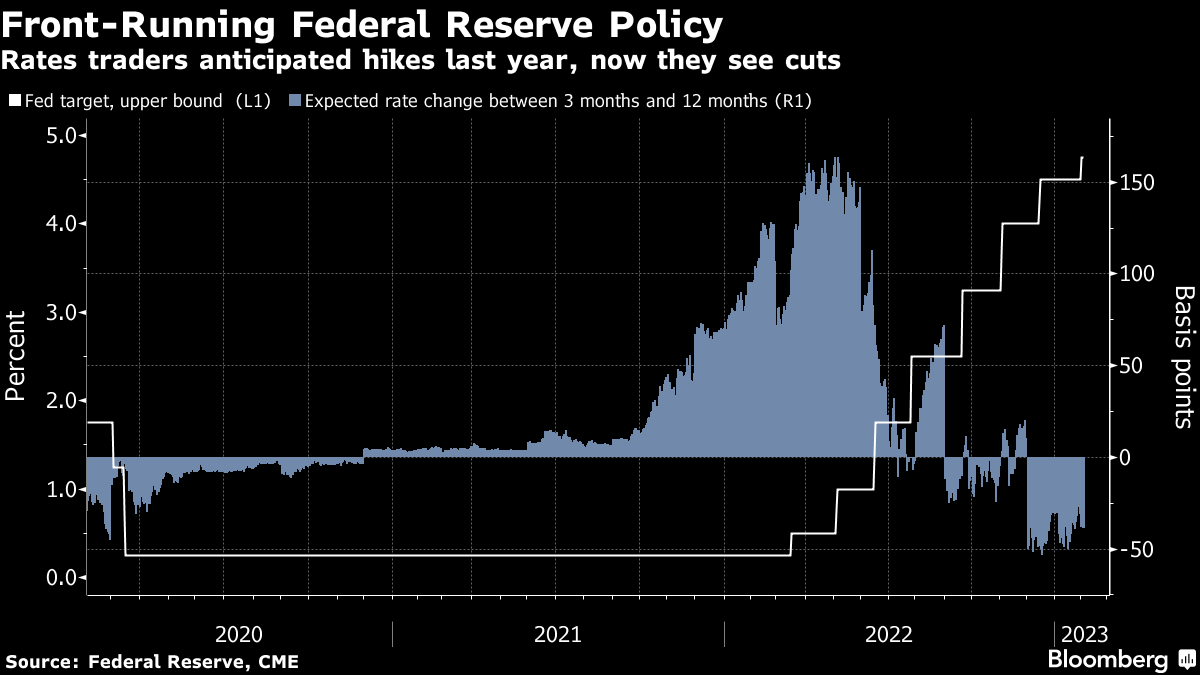

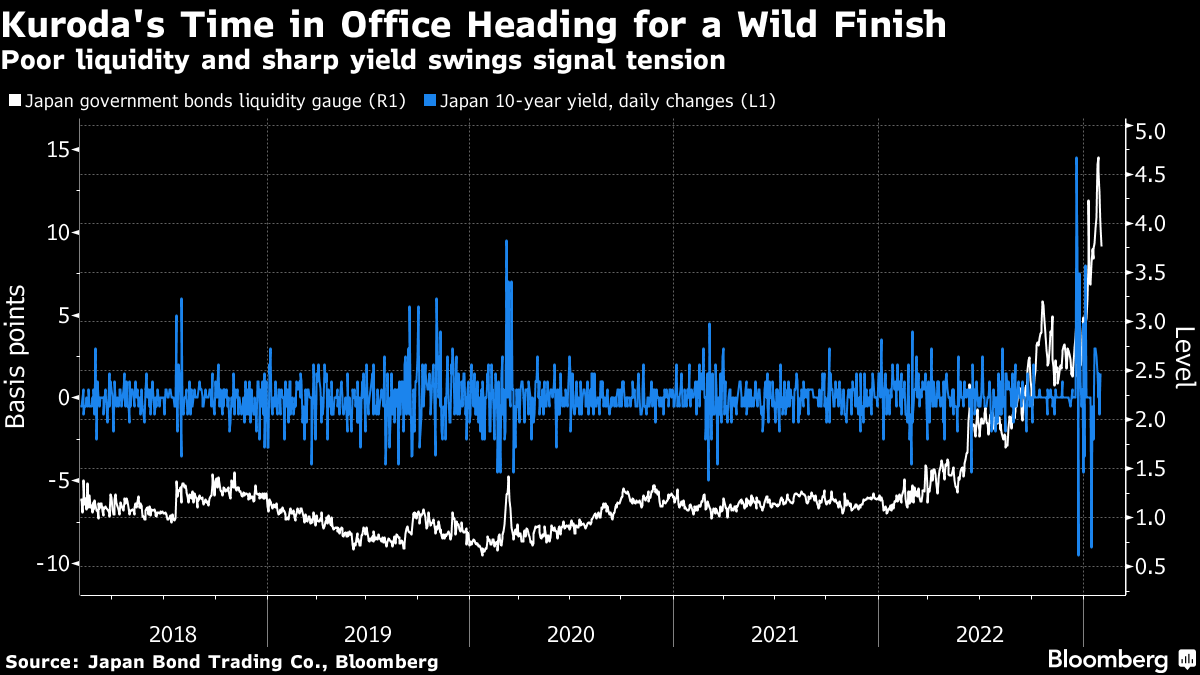

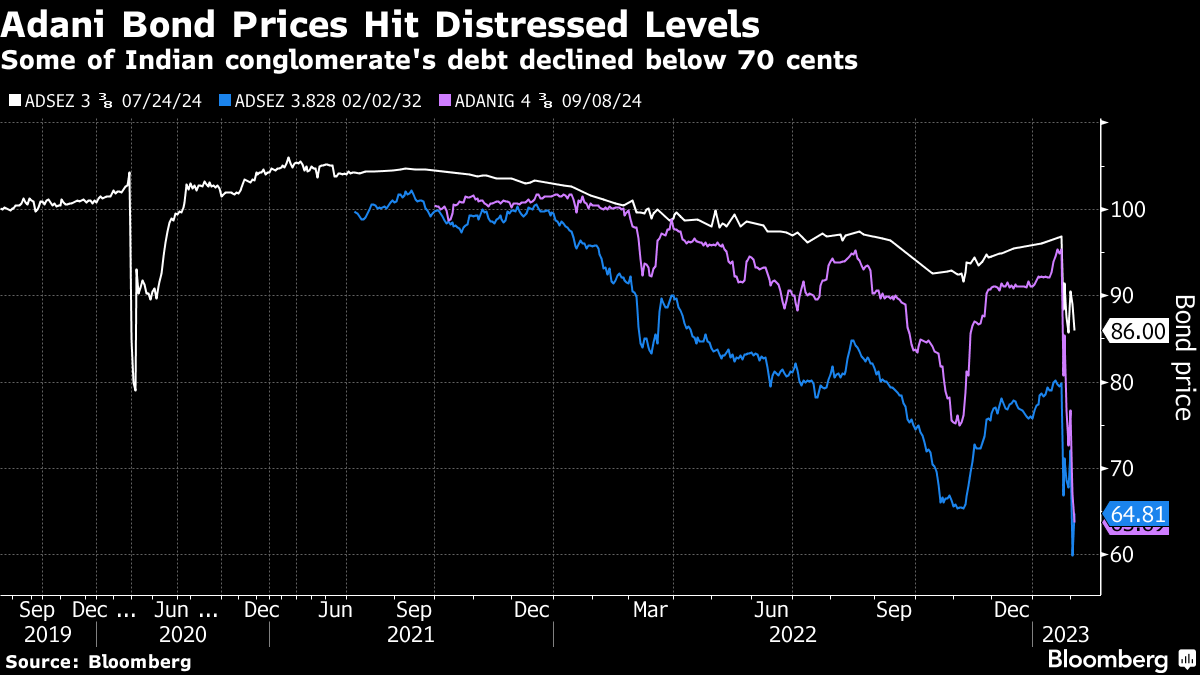

| Welcome to the Weekly Fix, the newsletter that knows what goes up must come down. I'm Bloomberg's chief rates correspondent, Garfield Reynolds. Central banks in the US, Europe and the UK all raised interest rates to fresh multi-year highs, while signaling there is more tightening to come plus a willingness to hold policy at restrictive levels for a long time. Bond investors responded by piling in to bets that policymakers will soon start cutting borrowing costs. The International Monetary Fund was among those warning the battle between markets and central banks could cause pain for both economies and investors by counteracting policymakers' efforts to restrain growth in order to curb cost pressures. Part of the problem is that the Federal Reserve is starting to sound less hawkish than before. Chair Jerome Powell's speech palpably failed to offer the pushback against the pivot narrative that heavyweight bond investor Jeffrey Gundlach for one was expecting. Ray Dalio of Bridgewater Associates, told markets to listen to Powell's warnings about higher rates even after the press conference, but few seemed to listen. Financial advisers felt the need to warn clients against Fed FOMO. It's also possible the record shorts hedge funds had placed against Treasuries could have helped boost this week's rallies. Given that background, even the European Central Bank's relatively hawkish moves — raising rates by half a point and making it clear another step-up would come next month — made barely a splash. Investors are becoming ever more convinced each hike is just bringing the world closer to the day when central banks will again act to ensure asset prices stay elevated. The fact similar bets last year on imminent rate cuts went awry is also being set to one side. One of last year's top-performing bond funds is again positioning for a sell-off in 2023, figuring other investors are wrong in their pivot optimism. There are also some investors for whom the pivot question is well and truly moot — US defined-benefit pension funds sitting on their biggest surplus for two decades. Emerging-market investors were simply relieved Powell seemed pleased with the progress made on inflation. A key driver for bond investors' conviction may be the growing signs of distress in the world's highly-leveraged housing markets — the sort of development that usually means a slowdown is coming for economies. Data in the coming days will offer plenty of tests for the pivot thesis, starting with Friday's US payrolls, and continuing with US January inflation and retail sales figures due in mid-February. Japan is the one central bank expected to tighten throughout this year and also the lone major economy that stuck with ultraloose policy. The battle there between policymakers and investors is set to get fresh spice in the coming weeks as the government decides on a successor to Governor Haruhiko Kuroda. His 10-year tenure saw an astonishing level of asset purchases — the Bank of Japan now owns more than half of the nation's government bonds — along with negative interest rates and yield curve control. This week we got a reminder of some of the distortions that's created with the wild yield gaps that have opened up between the current benchmark 10-year notes and the bond issues previously in that role. Traders are busy pondering whether the next BOJ head will be hawkish or dovish, and what that many mean for curve control and the yen. Hopes are high for a change, with contender Takatoshi Ito, a Kuroda ally, saying steps toward normalizing policy this year are possible. Another piece of the puzzle is whether Prime Minister Fumio Kishida ends up shutting women out of the bank's new leadership team, a decision that would reinforce the idea Japan isn't serious about addressing gender inequality. Indian bonds were hammered along with equities after short-seller Hindenburg Research issued a report accusing the giant Adani Group of stock manipulation and accounting fraud. The company has rebutted the claims. Even as stocks took front stage with a $108 billion meltdown, the group's debt structure was a key part of the action as its bonds traded at distressed levels. Famed emerging-market investor Mark Mobius said his firm didn't participate in Adani Enterprises Ltd.'s stock sale before it was pulled because of concerns about the group's debt. Some Adani companies saw yields soar on debt that was close to the interest payment date. And a key potential contagion path was underscored by revelations India's biggest bank is said to have made as much as $2.6 billion in loans to Adani companies. The nation's central bank is reportedly asking lenders to provide details of their exposure to the conglomerate. The decision by Credit Suisse Group AG to stop accepting bonds of Gautam Adani's group of companies as collateral for margin loans to its private banking clients also caused some alarm. - UK bonds are all the rage as the scars of last year's crisis fade

- The analyst who exposed Libor is now busy taking aim at its successor

- The EU risks missing a March target to agree on reforming its debt limits

|

No comments:

Post a Comment