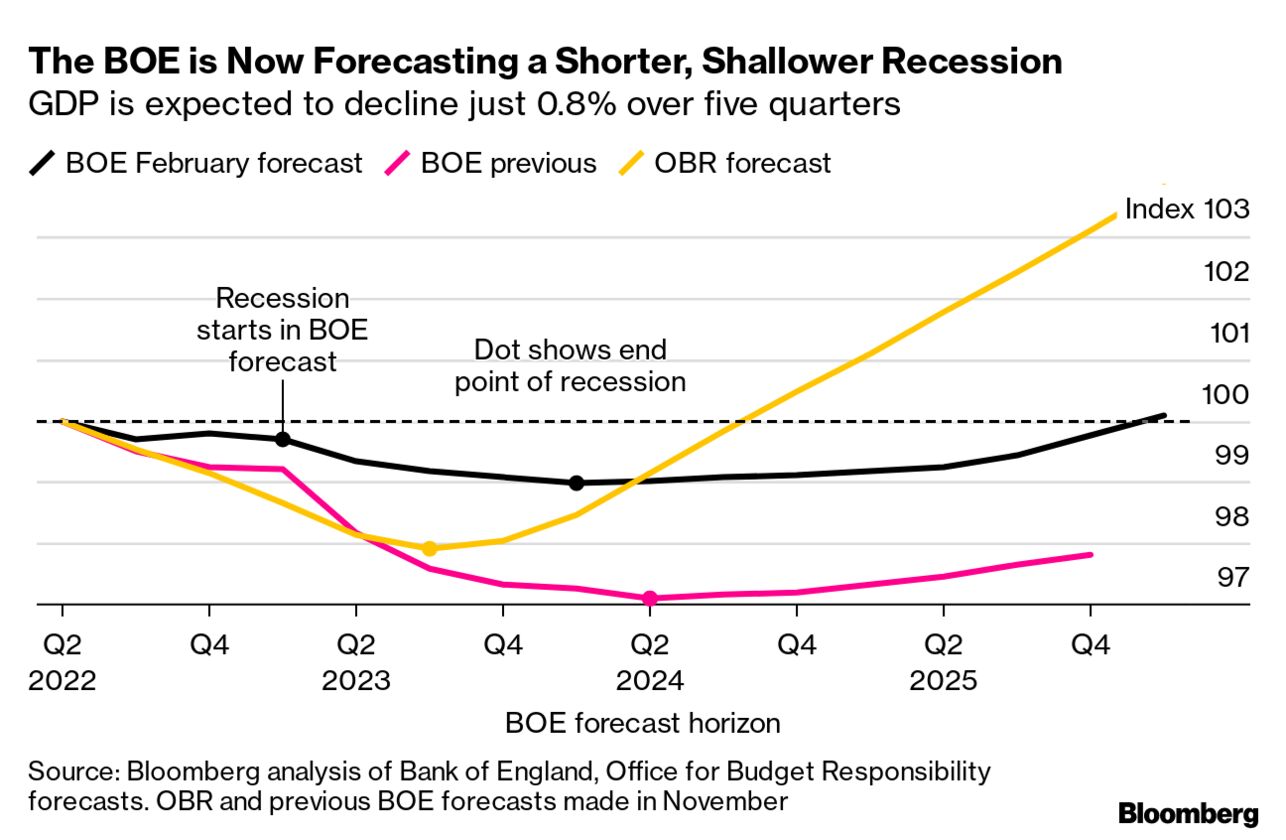

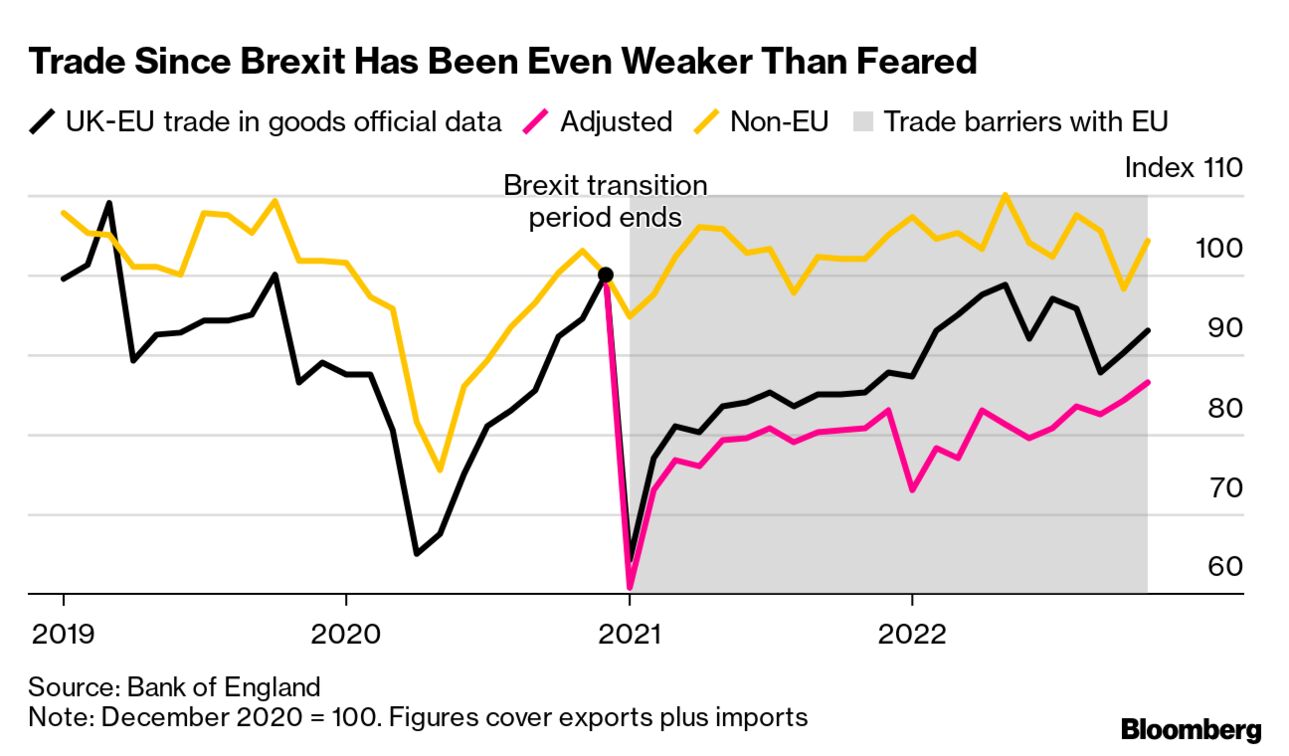

| Part of what will make the going so tough is the decision this morning by the Bank of England to hike interest rates — again. It wasn't a surprise, but it heaps pain upon already plentiful pain. The day began with the shocking revelation (but excellent journalism) that British Gas debt collectors break into customers's homes to fit prepayment metres. Swiftly on the heels of that, energy company Shell announced bumper profits while revealing it paid just £100m in windfall tax – part of what Bloomberg reporters called a "blowout year for big oil". "The companies have been criticized both for making too much money," Bloomberg's Will Mathis reports, "and for giving so much of it back to shareholders instead of investing more in new energy supplies." The possibility remains that Shell has misstepped: "With the Labour party leading opinion polls heading into the next general election, the company may become a campaign issue and eventually face higher windfall taxes as it sends more profits to shareholders," Will writes. (A rather overlooked story yesterday was energy company Octopus saying it had posted a loss — but that was because they had absorbed the higher costs of gas without passing it on to consumers). But it's on top of these cash-strapped households that the Bank of England nonetheless this morning imposed a 10th consecutive interest-rate hike. It did drop its warning it was prepared to act "forcefully," fueling the idea that the end of hikes is in sight. But that signal was quickly interpreted as too dovish — which meant the pound this afternoon fell against both the dollar and euro. The Bank once again forecast that the UK's recession may be shallower than earlier predicted, but it also reiterated its gloomy view it will be five quarters. This means the UK is only expected to return to health next spring — perhaps only half a year from a general election. Around this time, the Bank also expects unemployment to be 500,000 people higher. A prediction of more people out of work, and more people paying more on mortgages? In the real economy, and in the political economy, the medicine hurts. The economic damage done by Brexit is happening sooner than feared, the Bank of England warned. The central bank said the UK economy is being hindered by a sharper slump in trade with the European Union than implied by official statistics and "very subdued" business investment. Since the UK's new trading relationship with the EU began in January 2021, official data shows a 7% fall in trade. But the BOE's adjusted figure points to a 14% slump. Read more from Tom Rees and Andrew Atkinson. |

No comments:

Post a Comment