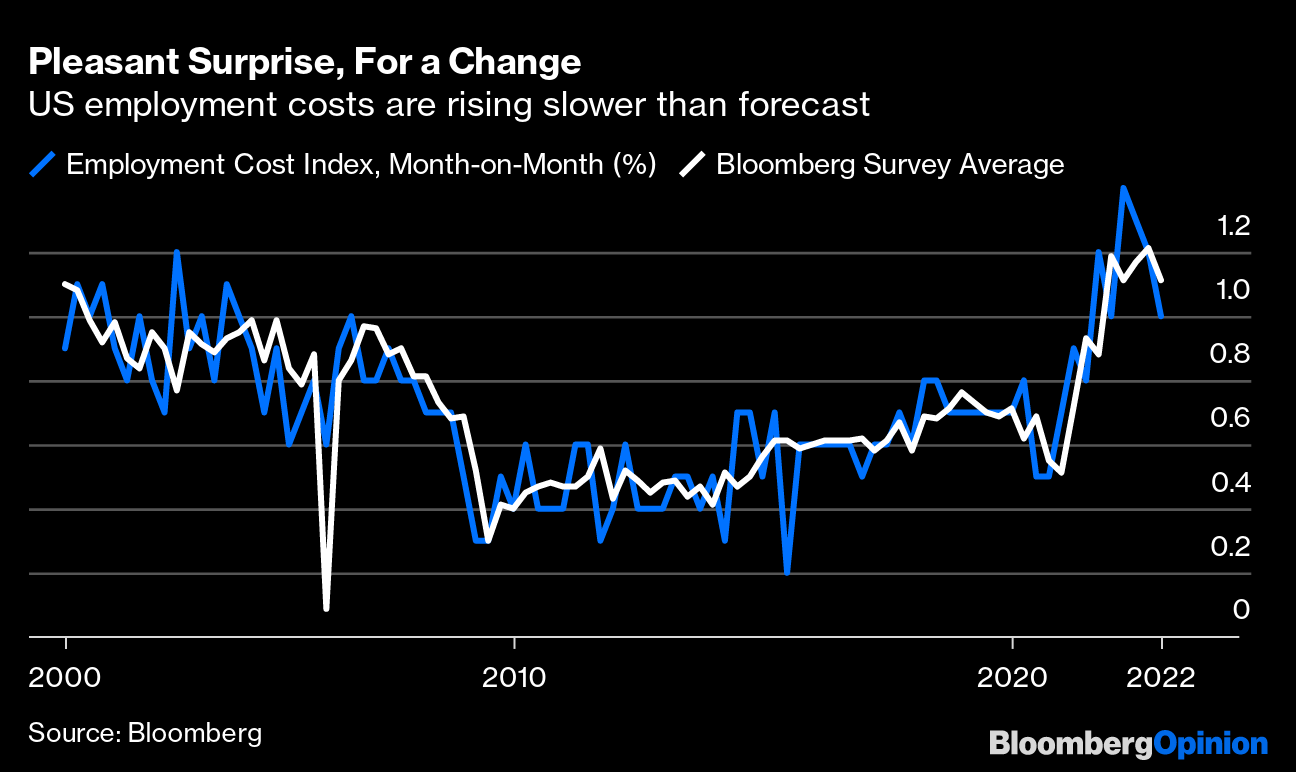

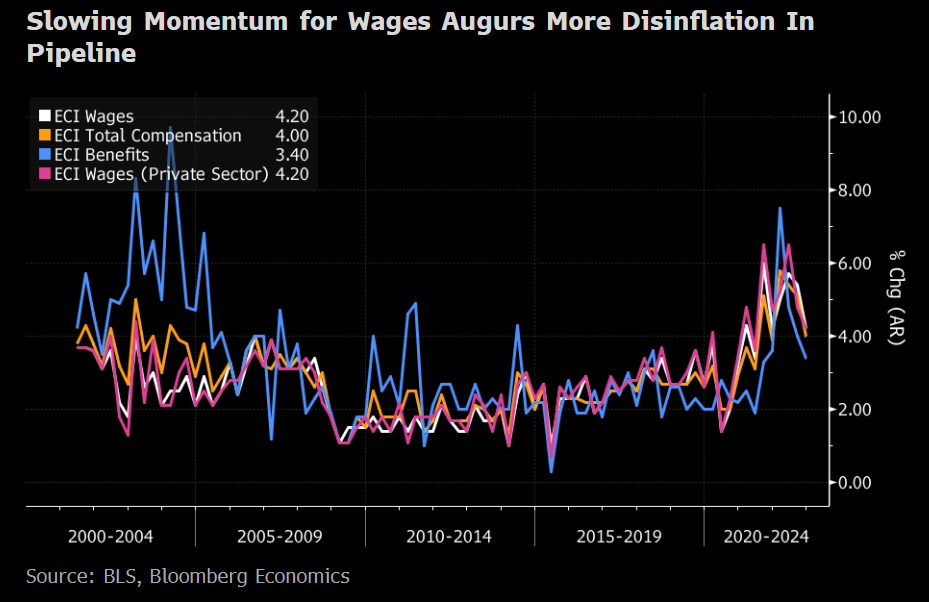

| For something that never used to attract much attention, the employment cost index is turning into a reliable star of the market. That's because the ECI, a broad gauge of wages and benefits, is the Federal Reserve's preferred measure of workers' pay, and it's thus become a key indicator of inflationary pressure. A nasty surprise from the index in the third quarter of 2021 shifted the Fed's thinking, and also knocked the market; and so Tuesday's news that the ECI increased only 1% in the fourth quarter at a slower-than-expected pace was a pleasant surprise for a change. It reinforced the stance of those who believe inflation is, indeed, moderating: Looking at the numbers in more detail, the quarter-on-quarter trend for employment cost growth to moderate is clear. However, year-on-year growth remains too high for the Fed's comfort: US stocks rallied on the news as it solidifies the narrative that the central bank will raise its target rate by only a quarter percentage point. Ed Hyman, founder of Evercore ISI, described the ECI as adding to "a compelling package that inflation is slowing significantly." This is exactly what was to be hoped. But it's not a time to get carried away. As Chris Low of FHN Financial puts it: Wage pressures are slowing faster than expected, though as the year-on-year chart makes clear, the progress is small so far, and to a rate still too fast to be consistent with 2% stable inflation. At the same time, wages are slowing with clear downward momentum, as is clear from the chart of quarterly changes. On balance, the Fed should be pleased things are heading in the right direction.

Getting into the weeds, what Wall Street investors cared about was the impact on the likely course of interest rates. On this point, it's far more dubious that the ECI is enough to change the Fed's plan for further rate hikes. Wages are overall rising too swiftly to be consistent with the official inflation target of 2%. Here's Bloomberg Economics' Anna Wong: The moderation in fourth-quarter ECI indicates more disinflation in the pipeline for core services. Slower wage growth likely bolsters Fed officials' confidence that they should slow the pace of rate hikes, but it won't stop them from taking rates to at least 5%.

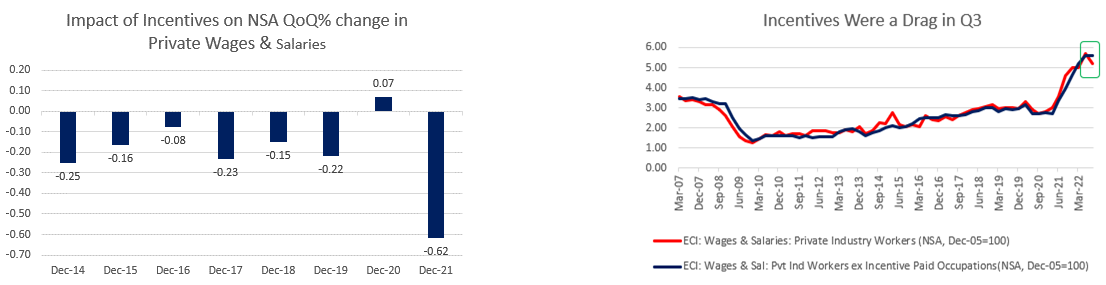

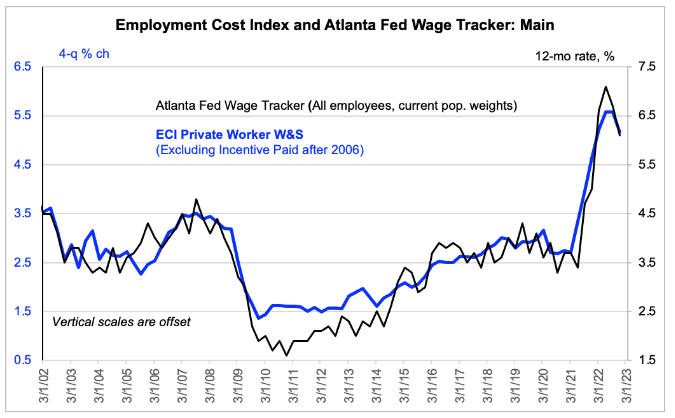

Are there any drawbacks? Omair Sharif of Inflation Insights LLC draws attention to "core" wage increases, excluding incentives. Once industries that pay significant amounts of their wages via bonuses are excluded, these core wages are still rising. In other words, companies with the flexibility to reduce pay by cutting bonuses have done so, and this has had a big impact on the overall data, but "underlying wages" are still increasing. As he shows, incentives had an unusually drastic and thoroughly negative impact in the fourth quarter: Gerard MacDonell of 22V Research makes a similar point, saying that the ECI release "was not a beat" at 0.9%, once benefit-paying occupations were excluded. This measure of wage inflation, he said, was "fully consistent with what the headline smoothed Atlanta Fed Wage Tracker implied." The Atlanta Fed's measure is based on census data and appears monthly: So there's a case that these numbers aren't quite as good as they look. Japan, where a far larger proportion of the workforce is paid via bonuses, has famously found it easier to keep inflation under control than others. Their system means there is less risk of a wage-price spiral. It's still not clear that the bulk of US companies can say the same. On balance, however, the Fed will likely still be satisfied that inflation is heading in the right direction. The personal consumption expenditure (PCE) index, the Fed's favorite inflation measure, came out last week with a slew of economic data supporting the notion that the central bank's aggressive tightening is already taking effect. This includes the cooling in US housing market, and the unexpected decrease in consumer confidence.

—Reporting by Isabelle Lee As you receive this, an "FOMC Day" is dawning. At this point, there is little point in speculating much more, but to those looking for more clues as to where stocks may be headed in the last two hours of trading, consider this. The S&P 500 has averaged a one-day gain of 0.28% on all Fed days since the Federal Open Market Committee began releasing its rate decisions on the same day as the meeting, which dates back to 1994, according to data compiled by Bespoke Investment Group. That gain is far better than the average 0.03% seen in all trading days since then. For all the work that goes into trying to predict the FOMC, then, it looks like the official announcements do contain real market-moving news. Bespoke's research also confirms what we might have expected, that Fed days that have seen rate cuts have outperformed those when rates have been hiked or held steady. Nobody is expecting the Fed to cut, and neither should they. But ECI still grabbed plenty of attention, because it directly supports a downshift in the tightening program to only a 25-basis-point hike. That is now a virtual certainty, and almost any other outcome would be a huge shock.

But while the chances are very slim that the recent data will alter the Fed's policy decision, it may profoundly impact rhetoric at the press conference. Chair Jerome Powell will need to decide what to guide about the next meeting, and whether to open the possibility that there will be no more hikes. Market pricing still suggests that investors find that unlikely; if you believe the fed funds futures market, the chances of a 25-basis-point hike in March are almost 90%. But it's obvious that many are hoping this is the end of the tightening cycle, and will jump on any excuse to act accordingly. The problem, as Points of Return has said many times, is that if markets preempt a Fed easing, or "pivot," then they make financial conditions easier and thus increase the need for the Fed to be more aggressive. That has led to widespread predictions that Powell will have to sound very hawkish to the press, just as he did at the Jackson Hole conference last August when he successfully squelched a previous premature market rally by talking tough. This is the comment of Win Thin, investment strategist at Brown Brothers & Harriman: The Fed should leave the door wide open for further rate hikes and Chair Powell should stress that the Fed is prepared to continue hiking rates beyond 5% and keep them there until 2024, as the December Dot Plots showed. With the Fed likely downshifting again to a smaller rate hike, markets may mistakenly take this as a sign of weakness in the Fed's resolve. The swaps market is pricing in a peak policy rate near 5.0%, which is lower than the latest Dot Plot. What's worse, the market is pricing in an easing cycle in H2 while the Dot Plots suggest this is a 2024 story. Expect the Fed to push back against this notion.

So strong is that expectation, however, that more or less any weakness or conditionality can be presented as a sign that the Fed is preparing an oncoming pivot. One investment banker offered the following summary of what could happen (with barnyard expletive deleted): There are two market outcomes from the Fed's latest rate hike tomorrow. The first is a generic sell the fact as we are already over our skis. The second is the wildest hurricane of Fed pivot **** you've ever seen. I expect the first but fear the latter.

Problematically for Powell, the words "Jackson Hole" are being bandied around widely. Nothing less than the kind of declaration of intent he offered in Wyoming will do. Powell has repeatedly pushed back against hopes of rate cuts later this year, and hasn't expressed the possibility of pausing rate hikes after the March meeting.  Nothing less than a Jackson Hole game face will do. Photograph: Bloomberg Rich Steinberg, chief market strategist at the Colony Group, described the ECI data as "more of a validating story that some believe that the Fed will pivot," but added, "my guess is, the bulls are trying to gather some kind of momentum." They are certainly doing a good job of building that momentum. On Tuesday, US stocks ended January with the S&P 500's best month since October and the tech-heavy Nasdaq 100's biggest rally since July. It's been a stellar start to the year after a horrible 2022 in which asset classes across the spectrum suffered record drops. But this has been helped by a surprising return of central bank liquidity, with both the Bank of Japan and the People's Bank of China unexpectedly making far more money available. And gains have generally been led by the greatest casualties from 2022. So could this be just a bear market rally? According to Steinberg: There's a psychological magnet for people to try to buy the busted stocks from the previous year. You've seen that in tech. You've seen emerging markets and international rip this month. But the market's trading at 18x earning. So, we would need to be in a Goldilocks environment of perfection for the market to really have any P/E expansion or upside from these levels in a significant way. What would get us to have P/E expansion? It would be no recession, margins stay strong, earnings get better, inflation abates. Every single box would have to be checked. And we just don't think we're there yet.

This is an eminently reasonable point of view. But markets have developed momentum, and there is money to be put to work again. Any excuse will be gratefully accepted to continue the rally. There is every reason to expect the historic pattern of eventful FOMC Days to continue. Meanwhile, when he appears before the press, Jay Powell had better be ready with his best hawk costume. —

—Reporting by Isabelle Lee  | OK, here's an FOMC playlist. There's When Doves Cry by Prince, The Wings of a Dove by Madness (or also Wings of a Dove by Bob Marley and the Wailers), "Beautiful Imbalance" by Thrashing Doves, Night Hawk by Coleman Hawkins, Night of the Hawk by Hawkwind, Tighter and Tighter by Soundgarden, or Take A Hike by Jiyeon. Or best of all, you could reprise the "pivot" scene from Friends, which in its entirety can be viewed as a great allegory for the Fed's current predicament. Here are the outtakes. For an idea of where they got their inspiration, try this classic (colorized) scene from Laurel and Hardy delivering a piano. Here's the whole movie. And let's hope I never have to call this one into service as an analogy after an FOMC meeting.

Like Bloomberg's Points of Return? Subscribe for unlimited access to trusted, data-based journalism in 120 countries around the world and gain expert analysis from exclusive daily newsletters, The Bloomberg Open and The Bloomberg Close.

More From Bloomberg Opinion: Want more from Bloomberg Opinion? {OPIN <GO>}. Web readers click here. |

No comments:

Post a Comment