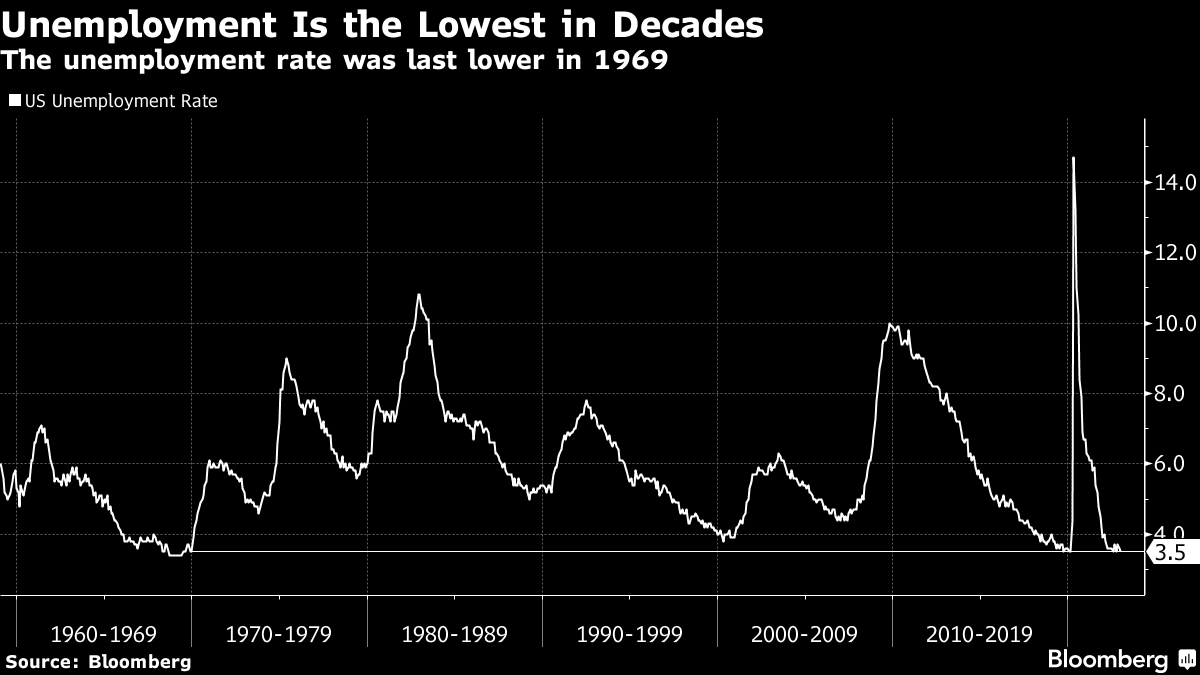

| I'd argue you can forget all about what Powell has to say Wednesday. It won't matter. Sure, it could have a minor short-term effect. But the market has proven impervious to previous hawkish Fedspeak. And, with the Fed likely to endorse the market view of a step-down despite easy financial conditions, why would that change? I think it changes over time. And the basis is through two highly uncertain variables — employment and inflation — which the Fed is watching to calibrate its policy. Right now, the employment picture looks good. The unemployment rate is at a five-decade low and initial jobless claims are running below a meager 200,000. But we get benchmark revisions to all the data from 2022 on Friday. That could change the picture. What's more, even though initial claims for unemployment insurance are low, bolstering the view of a strong employment picture, continuing claims have surged by 300,000 in the last three months. We could be on the cusp of a fading as the job cuts in the tech industry weaken the broader economy and seep into employment weakness elsewhere. On the inflation front, inflation is coming down, particularly in the price of goods and housing. But the Chinese re-opening should add additional price pressure on goods. And core services inflation outside of housing remains sticky. Bloomberg Chief US Economist Anna Wong recently noted that Powell watches core services excluding housing rents as the metric that tells him where inflation is headed. In a note on Dec. 27, Wong noted: It rose 0.3% in December (same as prior), corresponding to an annualized 4.1% pace. On an annualized 6-month basis, it has been steady at about 4% for the past 12 months, in comparison to an average of 2% before the pandemic.

That tells me inflation remains too high for the Fed's liking while employment looks pretty good. Unless that basic picture changes, the Fed is unlikely to lower interest rates. Instead, as officials have repeated ad nauseum, they will raise rates a few more times and hold to observe the impact of the large cumulative tightening. What moves the Fed from that view to the market's view? I don't think it's employment given how low the numbers are. To give us a sense of how much unemployment would have to rise, let's think about recessions. Outside of the Great Financial Crisis and the pandemic, the greatest six-month increase in unemployment was 1.6% in 1980, a deep recession. That would take us to 5.1%. But in the early 1990s and early 2000s, the rise maxed out at 1.2%. An equivalent rise would take us to 4.7% unemployment. I question if that is high enough to get the Fed to lower rates in the absence of declining inflation. As for inflation, we are running at a 4% annual pace on core services excluding housing. That's double the Fed's 2% target. Only a spate of deflation gets us to that target anytime soon. Say we had a recession and that number got down to 3% while the unemployment rate rose to 4.7%. Would the Fed cut with inflation well above target? I doubt it. Either the Fed has a lot lower inflation hurdle than I suspect or the market has gotten way ahead of itself. I expect the Fed to raise rates to 5 or 5.25% and then hold through 2023. And I expect the market to slowly come to that conclusion as the data come in, confirming core inflation remains too high. Let's remember that the penalty for the bond market's being wrong on rates is not severe. We're talking about a half percentage point here. That's a lot less than the rate hikes the market had to digest in 2022. The bigger question is for equity markets because of both earnings and discount rates. The S&P 500 began Tuesday just over 4,000. That's a level that will come under threat as margins erode due to still high inflation (think Caterpillar) and revenue growth challenges (think Microsoft and Intel). And then you have the marginally higher discount rate on top of it. Nothing about the Fed's policy announcement prevents the market from eking out a few gains in the coming weeks and months. But the easy gains were in January. Investors we polled actually expect the S&P 500 to retest lows under 3,600 later this year. Let's wait until 2024 for the all clear. ----- One more thing since I wrote you last week on tech. The sector's layoffs in the US have already topped 100,000. Do you agree with Bank of America analysts, who say that the sector is still bloated? What about the impact of AI, especially systems like ChatGPT — is that a threat to white-collar jobs, or a good investment opportunity? Share your views in our latest MLIV Pulse survey. |

No comments:

Post a Comment