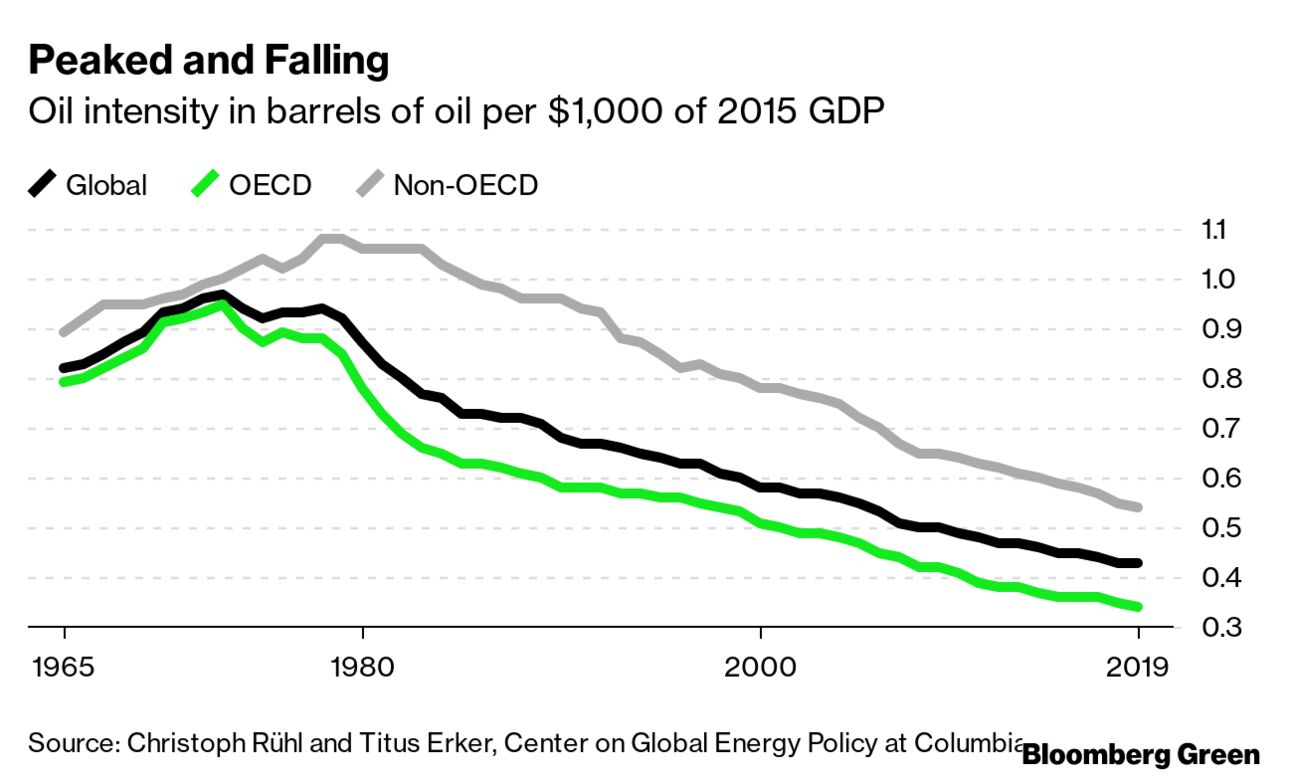

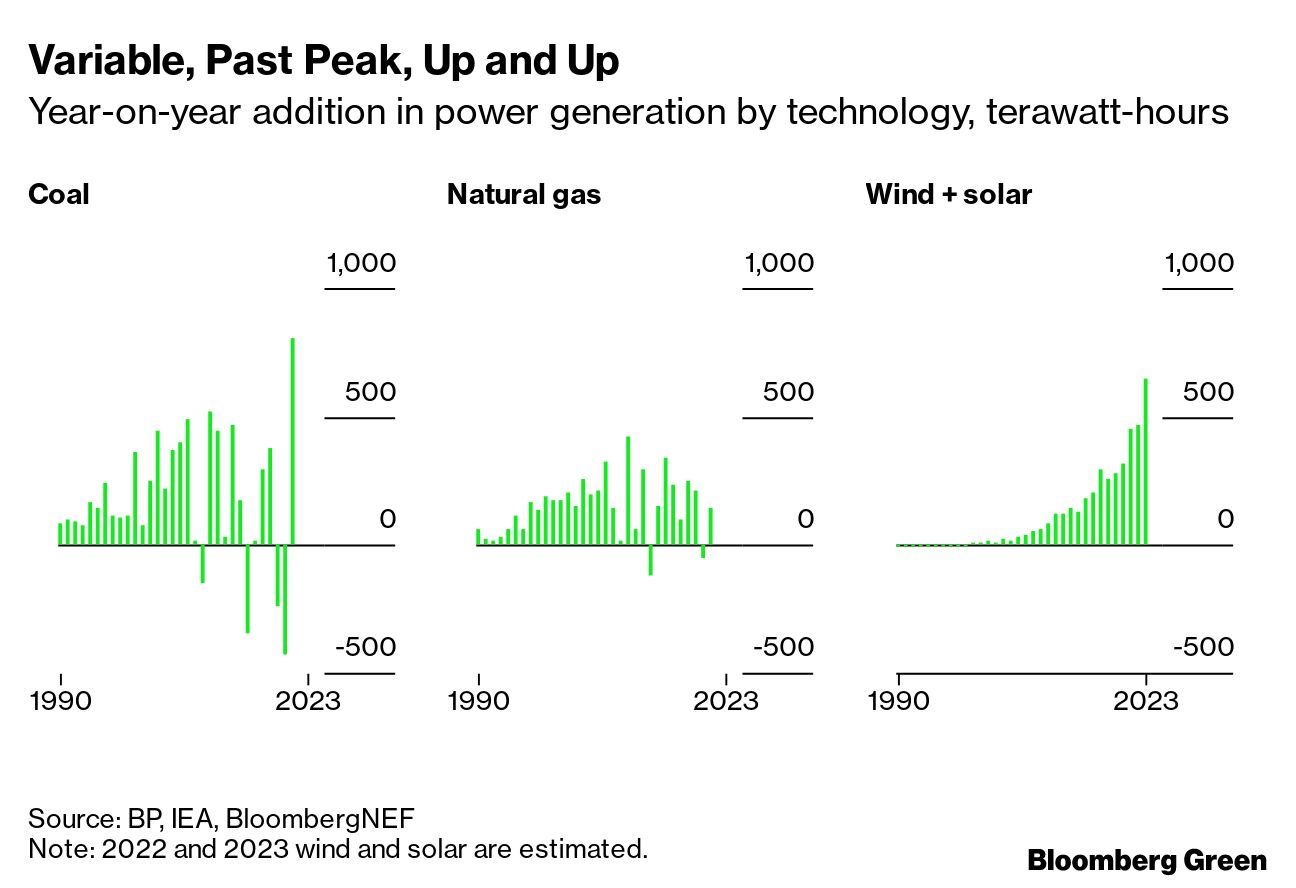

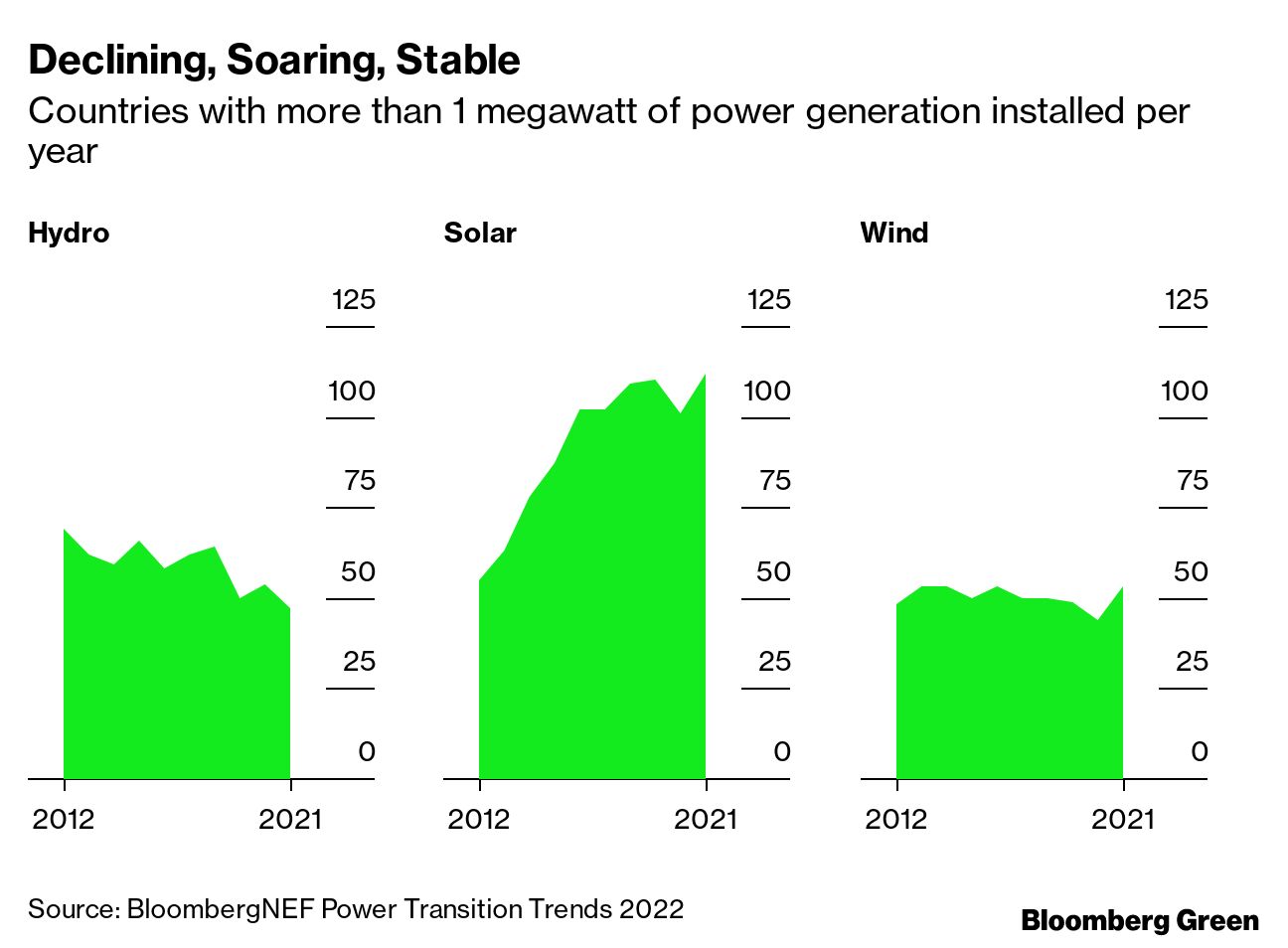

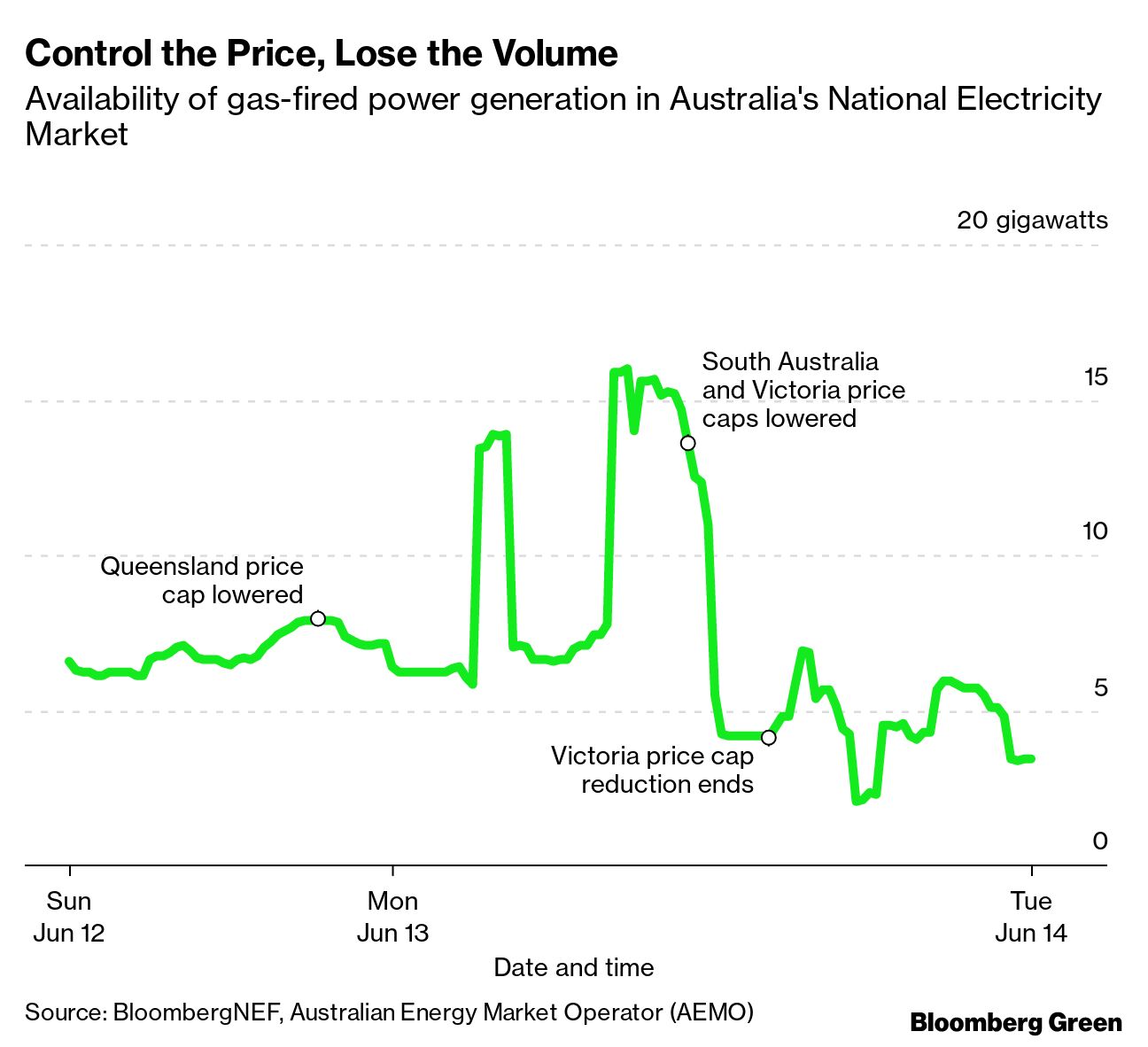

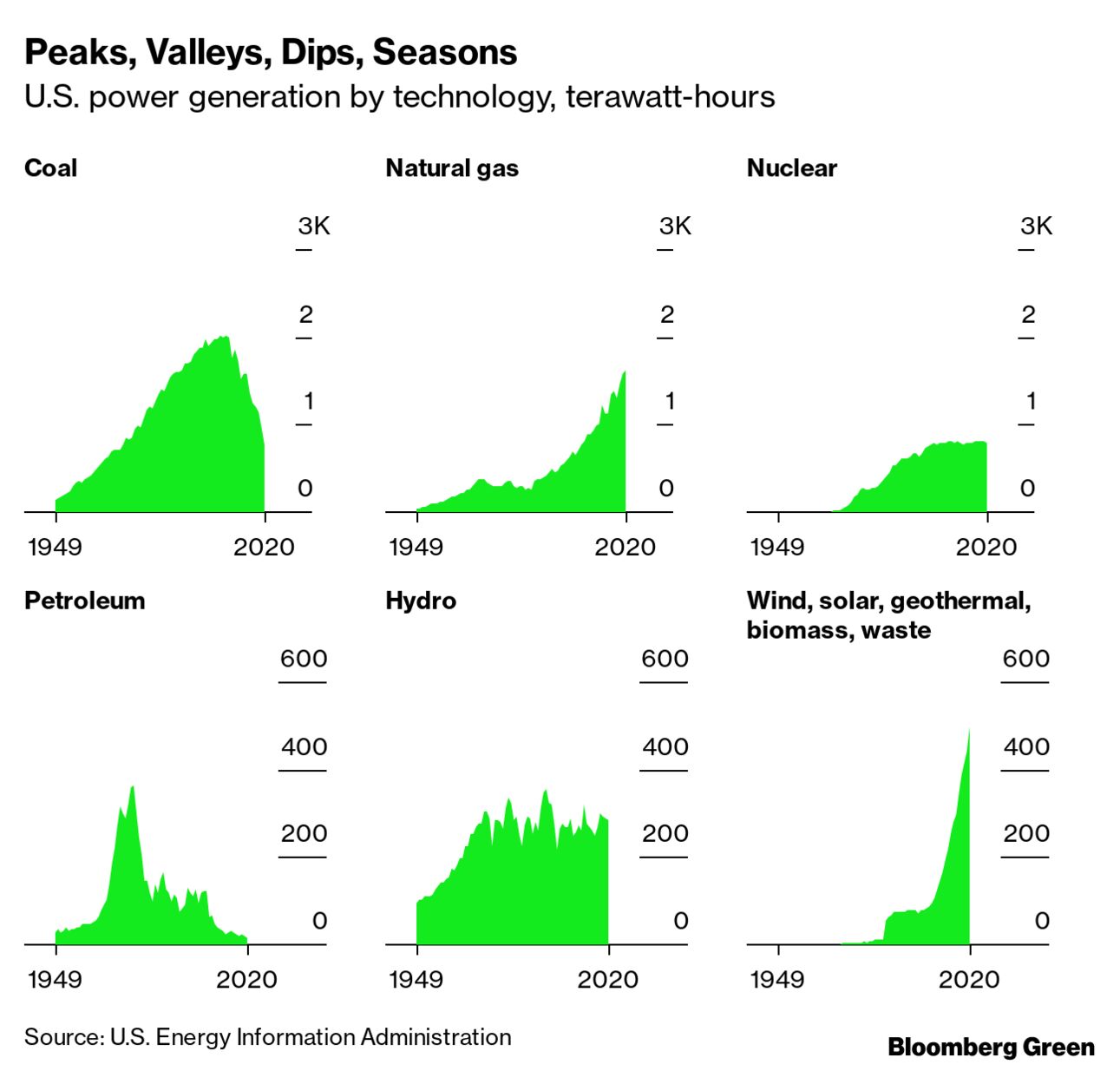

| For my final column of each year, I often look back on the data, stories and charts that told us the most about energy and climate. What a year 2022 has been. Recapping it with a handful of charts is challenging. But a few themes carry across the months. The shock of the old In March I wrote that Russia's invasion of Ukraine was a shock of the old that would be familiar to any historian of the 20th century. History reminds us that even global and seemingly ineradicable trends can change quickly during crises. The link between oil and GDP is a useful example. Prior to the 1973 oil price shock, the oil intensity of global GDP had been rising steadily — that is, economies needed more oil for each unit of economic output over time. Thanks to responses to that price shock, the oil intensity of GDP peaked that year in the OECD. In the rest of the world, it peaked only five years later. Change is difficult, but old shocks can give promise to new paths. Fossil peaks The International Energy Agency says we're in "the world's first global energy crisis," a set of shocks both deep and broad. It comes to a striking conclusion about what this means: Fossil fuel consumption is nearing a definitive peak. That peak is approaching even in the IEA's conservative scenario, which maintains prevailing policy settings across the global economy and does not factor for any technological breakthroughs. Look closely and you can see the trend leading to those peaks already — in particular in the power sector. Coal-fired power generation had its peak growth last decade (notwithstanding an exceptional post-Covid jump). Gas-fired power also peaked in growth during the same period. Wind and solar, on the other hand, just keep on growing. The IEA expects 460 terawatt-hours of new wind and solar power generation this year, about as much power as France consumed from all sources in 2019. Next year, the clean energy research firm BNEF expects about 650 terawatt-hours of new wind and solar — more power than all that Brazil consumed in 2019. High concentration Most growth in power generation is highly geographically concentrated, according to BNEF's annual Power Transition Trends report. So from 2012 to 2021, the top 10 markets for wind power accounted for 89% of all new capacity installed. Solar is only slightly more diffuse, with the top 10 markets in the same period getting 85% of all installations. But look at the data another way and solar is an expanding market: A decade ago, 55 countries were building solar projects in commercial volumes of more than 1 megawatt; last year, 112 countries were doing the same. Wind power, on the other hand, has not really stretched to touching more countries. Markets without a market I write about Australia often because it, like California, is a postcard from energy's future. The nation is making progress on deploying renewable power while remaining decidedly linked to global energy markets — despite not being physically connected to them (at least not yet). And in June of this year, Australia's electricity market stopped working. With demand for natural gas soaring, the national grid operator capped gas prices to protect consumers. Next it capped power prices (which had gone as high as A$15,000 per megawatt-hour in the spot market) at $300/MWh, a level at which many generators would lose money on every megawatt-hour sold. Then, with so many generators offline for economic reasons and insufficient supply to meet demand, the grid operator suspended all spot trading — leaving the country a market without a market. I asked BNEF's team in Sydney for ideas on how Australia (and any other market) should plan for a future with more, not less volatility of this sort. Their suggestions are worth reading in full. Yesterday's solutions I will close with another lesson from history. Since 1950, US power generation has expanded more than 12 times over, from 300 terawatt-hours a year to more than 4,000. Its key resources, however, have taken very different paths through those decades. Coal has peaked and fallen; nuclear rose and plateaued; petroleum has nearly vanished. Today, gas and renewables are both growing. Those trends are not just the market at work. Coal's rise came because oil-fired power was both quite polluting and then punitively expensive — and gas was seen as scarce and better suited to industrial uses. Coal was a solution to thorny problems in one decade, only to become a problem of its own decades later. It is possible that the system we build now could go the same way. A cautionary note, perhaps, but not necessarily a bad one. Solving the problem of overabundant zero-carbon power would create new solutions and new opportunities. Nat Bullard is a senior contributor to BloombergNEF and Bloomberg Green. He is a venture partner at Voyager, an early-stage climate technology investor. Like getting the Green Daily? Subscribe to Bloomberg.com for unlimited access to breaking news on climate and energy, data-driven reporting and graphics and Bloomberg Green magazine. Read and share this story on the web here. |

No comments:

Post a Comment