| Sam Bankman-Fried lands in the US to face charges, the Ukrainian president visits Washington and China plans to cut quarantine requirements. FTX co-founder Sam Bankman-Fried landed in the US late Wednesday to face a range of criminal charges. He is expected to make his first appearance in Manhattan federal court on Thursday. His lawyers may seek bail. Two of his associates, Caroline Ellison and Gary Wang, have pleaded guilty to criminal charges and have agreed to work with prosecutors. Meanwhile, it has emerged that FTX used a token it invented to fund its takeover of trading platform Blockfolio, according to financial statements obtained by Bloomberg News. In just half a day in Washington, Ukrainian President Volodymyr Zelenskiy garnered applause after a speech to US lawmakers and a promise from President Joe Biden for nearly $2 billion more in military aid and the long-sought delivery of a Patriot missile battery. In focus were the Ukrainian leader's interactions with members of the Republican party, who will have more sway over Washington's spending starting next month. Zelenskiy capped his speech by unfurling a blue and yellow Ukrainian flag signed by soldiers and saying, "We stand, we fight and we will win because we are united — Ukraine, America and the entire free world."  | China plans to cut quarantine requirements for overseas travelers in January, according to people familiar with the matter, as the country dismantles the last vestiges of its Covid Zero policy. Officials are considering a "0+3" policy, where the requirement to spend time in a quarantine hotel or isolation facility would be scrapped, and arrivals into the country instead subject to three days of monitoring, one of the people said. China is likely experiencing 1 million Covid infections and 5,000 virus deaths every day as it grapples with what is expected to be the biggest outbreak the world has ever seen, according to a new analysis. US equity futures were little changed as of 5:50 a.m. New York time, struggling to hold on to gains that saw the S&P 500 have its best daily advance in three weeks. The dollar pared some of its earlier declines, but still traded marginally lower on the day. In Europe, Stoxx 600 trimmed some of its earlier gains as autos, tech and consumer products underperformed. The yield on 10-year Treasuries declined about 2 basis points, trading within Wednesday's range. Oil rallied, while Bitcoin and gold were little changed. To catch up on the trading day in the UK and Europe, check out today's edition of City Latest. Today's US economic data include GDP, core PCE, personal consumption and initial jobless claims at 8:30 a.m., followed by the Conference Board leading index at 10 a.m. The US has a sale of 5-year TIPS reopening at 1 p.m. CarMax and Paychex report earnings.

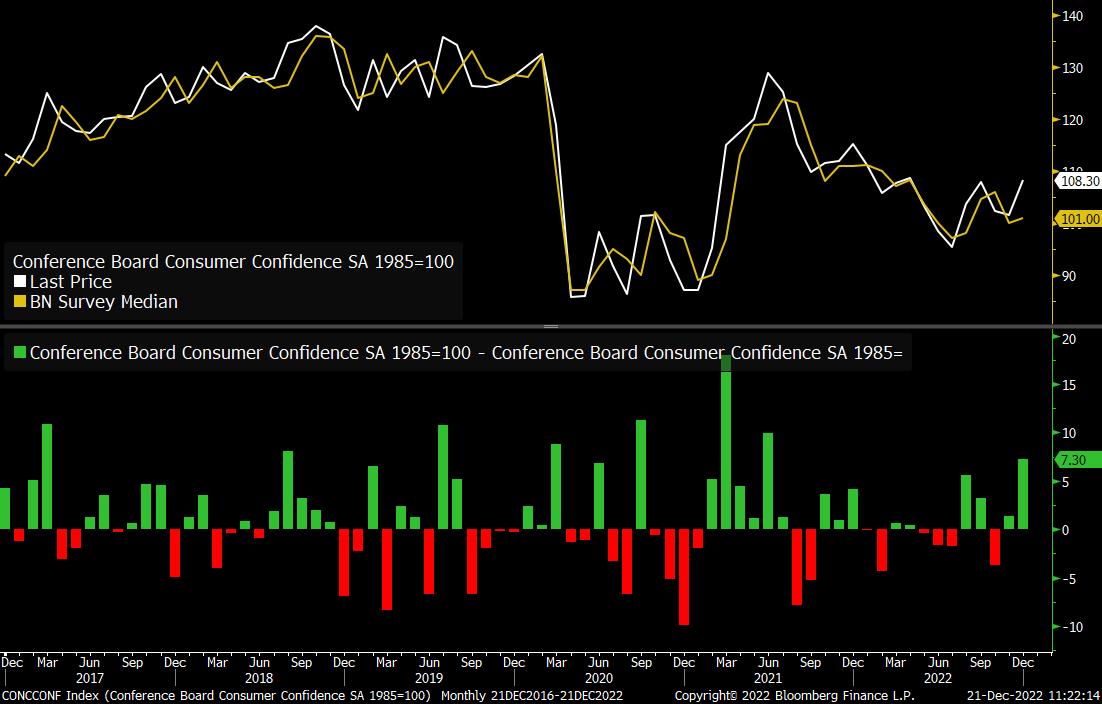

Which asset class will outperform next year? Where will the S&P 500, oil, and Bitcoin trade a year from now? And who will be the face of 2023? Share your views in our latest MLIV Pulse survey. Here's what caught our eye over the past 24 hours. Well this is my last paragraph in this spot for 2022. And I don't have some kind of grand takeaway about this year, or insight into what's coming in 2023. No predictions or surprises or contrarian thoughts from me. But here are two things that I'm thinking about at the moment. 1) A lot of the outlooks for next year seem to be of the variety that inflation risk is going to fade, and then it's recession time. And that seems reasonable enough. But the economy is not without its tailwinds. A big one is gasoline prices, which continue to plunge. And we may be seeing the fruits of falling gasoline prices in the consumer sentiment data, which is starting to turn higher. Here's a chart of the Conference Board Consumer Confidence survey over the last five years. Not only did we get a nice jump (as seen in the white line) it substantially beat the median expectations (the yellow line). In fact the size of the beat was the largest since the middle of 2021 (as seen in the second panel). There's other tailwinds out there as well. China seems to be opening up. Rate moderation may provide a cushion for housing. Supply chains are easing. So it's not all bad. 2) One of the things in 2022 was that basically every central bank was in hiking mode. You've seen all the charts. Everyone was rowing in the same direction. On Monday's Odd Lots, Jon Turek said something interesting though about how that could look different next year. We're going to be in this divergence period where there are central banks who are going to see very clear and obvious signs of growth deceleration, and there are going to be central banks that don't. And I would probably put the Fed in the 'don't' camp, where it's not obvious to me that, you know, GDP next year is on track to run it as the Fed thinks 0.5%. You know, I think as Joe was sort of cheekily alluding to earlier is that, you know, there's some pretty decent impulse for growth given that the composition shift is getting a lot more healthier in real terms. And if you can sort of get a little bit less financial market volatility, you can maintain some decent real income growth, which we have sort of seen now since July, then I think the economy can do pretty well. Whereas, you know, places like the UK, even Canada, places with very private debt levels relative to GDP and have a lot of floating rate mortgage exposure, you know, those places are going to feel growth in a very different way. And those central banks I think will be quicker to be like, 'Listen, we have to be a little bit more two-way in terms of how we approach the cycle.' So I think it's going to be, I think there are still north stars, but I think we're entering a period of pretty meaningful divergence where I think the economic performance is gonna be just very different across the world.

Jon also wrote about this theme in his Cheap Convexity newsletter yesterday. It's paywalled, but IMO worth subscribing to. Anyway, in conclusion, I guess you can kind of take the two thoughts together. The US has some tailwinds that may help out. Meanwhile other central banks, particularly in countries with high levels of variable rate debt, might start feeling the pinch sooner, setting up the possibility of policy divergence next year. Take care. See you in January. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart |

No comments:

Post a Comment