| The Federal Reserve signals slower rate hikes, China starts to learn to live with Covid and FTX's missing billions remain a mystery. Fed Chair Jerome Powell last night signaled the central bank will slow the pace of interest-rate increases next month, while stressing borrowing costs will need to keep rising and remain restrictive for some time to beat inflation. While that sentiment was very much in line with expectations, the confirmation that a calmer pace of hikes is imminent sparked a rally in global stocks and pushed the dollar to a three-month low. As Sarah Hewin, senior economist at Standard Chartered, put it, the upshot is "there is no one-way bet any more on dollar strength.'' China is starting to chart a path towards rejoining the rest of the world in living with Covid. Beijing will allow some virus-infected people to isolate at home, starting with residents of its most-populous district, a significant shift that reflects the pressure officials are under from a record outbreak and public opposition to Covid Zero. On Wednesday, China's top official in charge of the fight against Covid said the country's efforts to combat the virus are entering a new phase, with the omicron variant weakening and more people getting vaccinated.  | Bankrupt crypto exchange FTX's missing billions are still a mystery after its disgraced founder Sam Bankman-Fried denied trying to perpetrate a fraud while admitting to grievous managerial errors. In his first major public appearance following the Nov. 11 implosion of FTX and sister trading house Alameda Research, Bankman-Fried said Wednesday by video link at the New York Times DealBook Summit that he "screwed up'' at the helm of the exchange and should have focused more on risk management, customer protection and links between FTX and Alameda. US equity futures were tepid this morning as stocks elsewhere caught up with the overnight Wall Street rally, with S&P 500 and Nasdaq 100 contracts slightly lower as of 5:33 a.m. in New York. The dollar traded near its weakest level since mid-August, giving most Group-of-10 currencies a boost. Treasuries were little changed following a rally on Wednesday. Oil and gold rose while Bitcoin was flat after rallying more than 5% in the past two days.

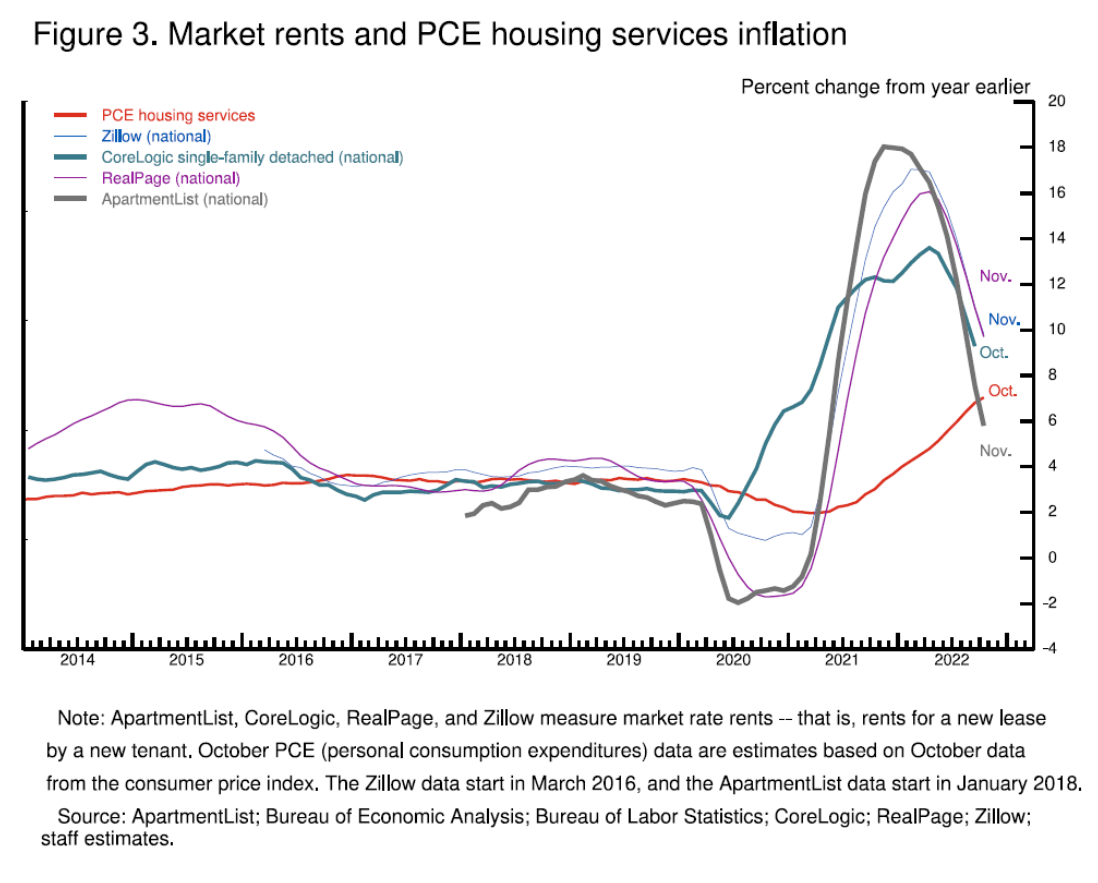

Catch up on all the market moves and news in the UK and Europe sessions via the City Latest blog. There's a glut of data out in the US today, as it reports personal spending and income data, the weekly initial jobless claims report and a pair of manufacturing gauges. The PCE deflator, the Fed's preferred inflation metric, is also due, which economists expecting it to show a more moderate rise year-on-year than in September. Meanwhile, French President Emmanuel Macron meets US President Joe Biden at the White House, where they are set to dine on lobster, caviar and an Oregon cheese named the best in the world. Here's what caught our eye over the past 24 hours: When it comes to the possibility of a "soft landing" there are a couple of important questions. One is, is a soft landing even possible? That is to say, can we see inflation significantly come down without a substantial increase in the unemployment rate? And the second question is, does the Fed believe that a soft landing is possible? This is important, because the whole discussion is kind of moot if the view of the Fed is basically "Unless we see the unemployment rate rise substantially, we will not be convinced that we've slayed the inflation dragon." Because if that were the case, then there definitely wouldn't be a soft landing, because the Fed would ensure a hard recession via rate hikes. Anyway. Markets soared yesterday after Powell's afternoon speech and Q&A session at the Brookings Institution. He definitely didn't declare victory or even pivot during the event, but he did offer glimmers of how victory could be achieved. So for example, he referenced this chart which compares the official PCE measure of housing services (the red line that has been steadily going up) vs other market based measures of new leases (that have rolled over very sharply in recent months. This is a popular #Fintwit chart that which suggests that because the government data lags the private sector data, that it's only a matter of time now before the official numbers start rolling over as well. Then during the Q&A he called a soft landing scenario "very plausible" and then he said "if we get good inflation data and we get evidence that -- of all the things that I talked about, if all those things start to swing the other way, then we could very much achieve this." This was generally the tone of the event, that the good outcome can't be totally ruled out. Obviously we can still have a hard landing. Inflation may remain higher for longer. The modest cooling that we've seen in the labor market, that I wrote about yesterday, could snowball into something more severe. But if things track towards a good outcome, the Fed won't necessarily get in the way. By the way, a good outcome would in some ways involve both the hawks and the doves proving wrong. Ideally, the hawks end up being wrong about a recession being necessary in order to bring down inflation. And ideally, the doves will be wrong about a rapid pace of Fed rate hikes turning into a disaster for workers. Follow Bloomberg's Joe Weisenthal on Twitter @TheStalwart |

No comments:

Post a Comment