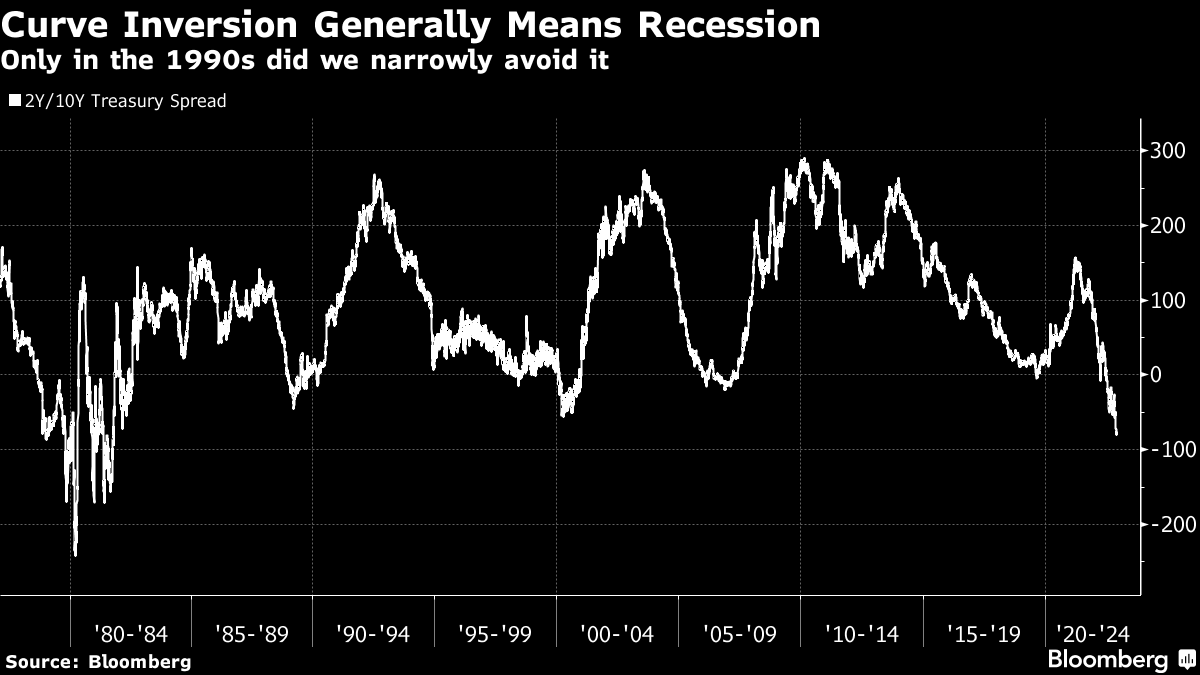

| What's common about the Fed, China and crypto? All of these seemingly separate narratives are dominating the global economy and they're all indicating that it's slouching toward a 2023 recession. The Federal Reserve has been leading the front until now with their jumbo rate hikes. But behind the scenes, China has been a big factor, too, by suppressing global demand and helping to create the very inflation the Fed is battling with the country's supply-chain busting zero Covid policies. China is now faced with a major policy dilemma as its policies are spurring unrest. And that's make or break for the global economy. Amid all this, crypto is rising as the poster child of what happens to riskiest of assets when easy money turns tight. The FTX bankruptcy, with all the hallmarks of fraud enveloping the firm, has ushered the industry's washout phase. That means we're closer to the end of the bust than the beginning. It's now the turn of other risk assets to come under pressure as corporate earnings start sagging along with the global economy. As for the economy, how do we know we're headed for recession? I'm looking at a number of indicators from oil prices to purchasing managers' indices to the yield curve — and they're all pointing to an economy that is starting to buckle. Nevertheless, there's no indication we have another Great Financial Crisis in the making. Household balance sheets look much better today than 15 years ago. That's a boon for long-dated investment-grade bonds. And with the Fed and other central banks committed to higher rates for the long-term, it will also benefit investors holding longer-maturity government bonds because of a lack of reinvestment risk. Let's start in China, where some are comparing the recent unrest to the 1989 protest movement in Tiananmen Square. Let's not get carried away yet. Still, fatigue over zero Covid policies is giving young Chinese enough of a taste of rebellion that protests are likely to continue and even escalate until President Xi forces a resolution. For many China watchers, this looks like a tipping point. In the short-term, Chinese universities have sent students home in order to quell the protests. And TV coverage of maskless fans at the 2022 Qatar World Cup has been heavily censored. But over the longer-term, the crisis resolution involves increased vaccination followed by an end to zero Covid. Before we get there though, how Xi Jinping responds is not only pivotal for China, it will also matter to the global economy. For example, oil prices have collapsed since midyear in anticipation of a slowing of demand due to future global economic weakness. Earlier this month, US oil futures contracts were already pointing to oversupply. An indefinite continuation of zero Covid will keep this structure in place. That may be good for the pocketbook but what zero Covid giveth, it taketh via supply chains. Companies dealing with China directly like Apple are once again suffering supply chain problems. They've cut their outlook due to the Chinese lockdowns (that are causing the protests) negatively impacting iPhone shipments. It's early days. But if the massive number of Chinese bots on Twitter trying to swamp protest news with spam and pornography is anything to go by, Xi is not going to relax Covid policies soon enough to quell the protests. If tensions continue to escalate, China will add another source of geopolitical risk, in addition to the war on European soil. Even if China does an about-face, it may still not avert a recession driven by rising energy costs that would climb further once its vast market reopens. Moreover, while we may have hit peak hawkishness, central bankers are still far from pausing rate hikes, let alone easing. For one, interest rates in the US are headed to 5%, if not higher. Two separate US bond market signals tell you where this is headed. The market favorite Treasury curve spread and the Fed's new preferred measure called the near-term forward spread are both sending bad signals about how far the Fed will go and the impact it will have economically. First, let's look at the Treasury curve because we have over four decades of data to work with. What we've seen is that when 10-year yields are lower than 2-year Treasury yields, as they are now, the economy lapses into recession soon after. The kicker here is that the 'curve inversion' is so extreme that we haven't seen anything like it since the early 1980s. That speaks both to a Fed that is going to keep raising rates and to an economy that will buckle under that pressure, forcing the Fed into retreat sometime after a recession. For its part, the Fed has said it doesn't think these longer maturity Treasury yields are the best predictive market signal. Fed Chair Jerome Powell has gone as far as to even say all of the explanatory power of the yield curve is in the near term. So they have come to see the difference between the 3-month Treasury bill and its expected yield in 18 months as a "cleaner" look into the future. Back in March, Powell said that when this near-term forward spread inverts (such that the expected value is lower than the present value), it's a strong signal the Fed is tightening into a recession. Well, the near-term forward spread has gone negative now. Normally the Fed would relent based on that signal. But with inflation so high, they feel forced to continue raising rates. And that, too, tells us the same thing the Treasury curve does - that the Fed is hiking into a recession. How severe, we don't know. |

No comments:

Post a Comment