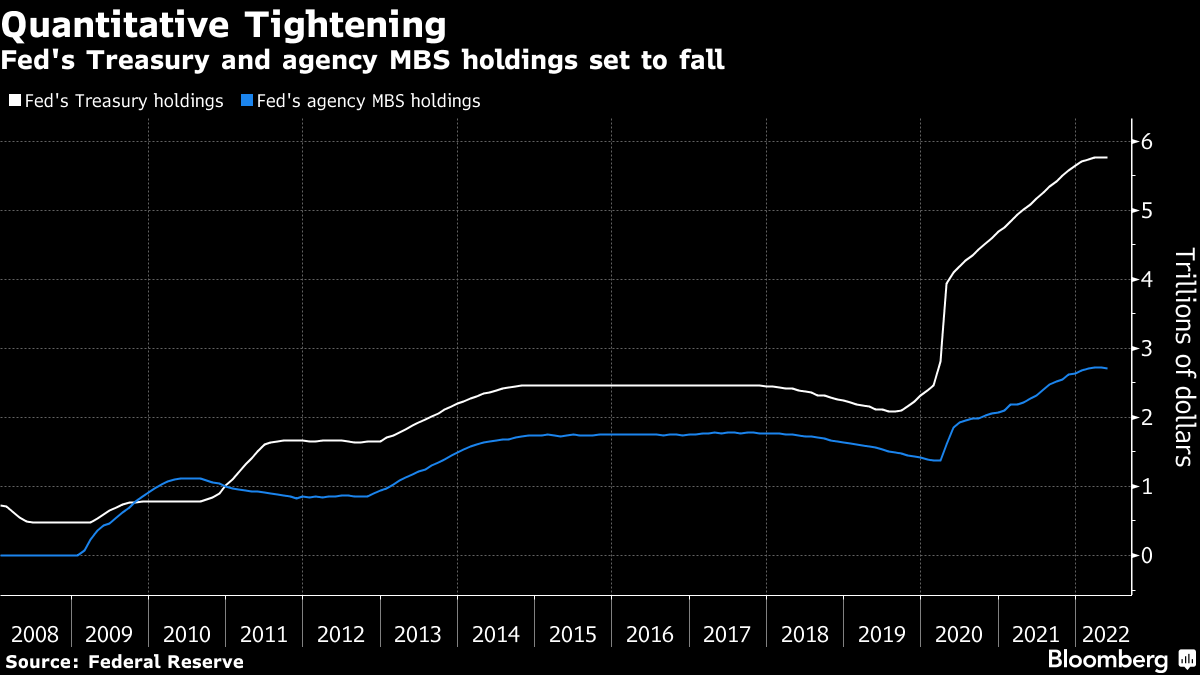

| Welcome to the Weekly Fix, where liquidity is ample and hedges are cheap. I'm cross-asset reporter Katie Greifeld. Wednesday marked the official start of the Federal Reserve's balance sheet shrinkage, with a $15 billion batch of Treasury securities set to mature -- without reinvestment -- on June 15. Given that this is the second time in modern history that the Fed has embarked on quantitative tightening, there are several enormous question marks. A big one is what the runoff will mean for the economy and fighting inflation (Fed Governor Christopher Waller: it's " highly uncertain"). Perhaps a harder question to answer is what shrinking the balance sheet will mean for already-fraught trading conditions in Treasuries. Liquidity in the $22 trillion market has deteriorated over the past few months, with the Bloomberg US Government Securities Liquidity Index -- a gauge of deviations in yields from a fair-value model -- hovering near the highest levels since March 2020. Fed officials are seemingly well-aware of the risk as the portfolio shrinks. The minutes from May's meeting showed that several policy makers "noted that the tightening of monetary policy could interact with vulnerabilities related to the liquidity of markets for Treasury securities." Layer in the fact that capital requirements have kept the big US banks from adding to market-making capacity in Treasuries over the past few years, and the outlook appears dicey. "Liquidity isn't great and financial conditions are already tightening before dealers even need to intermediate these Treasuries and mortgage-backed securities," said Deutsche Bank AG strategist Tim Wessel. That brings back nasty memories of late 2018. Fed chief Jerome Powell's remark that the balance-sheet unwind was running on "autopilot" sent the S&P 500 to the brink of a bear market -- a revolt that ultimately put an end to the Fed's hiking campaign. No such salvation is expected this time around, with Powell hell-bent on tightening financial conditions. The Fed's portfolio is projected to drop to $5.9 trillion by mid-2026, with the balance sheet shrinking by an average of $80 billion per month through 2024. Given that repeatedly expressed desire to tighten the economic reins, it's probably annoying for Powell and company that the exact opposite is happening. Financial conditions -- a gauge of market stresses across equities and credit -- have actually eased back to levels seen before the Fed's kickoff hike in March. A Bloomberg measure currently sits at -0.33, up from -1.21 reached in mid-May. That should theoretically be a headache for a central bank attempting to tamp down demand in an overheating economy while cooling the hottest inflation readings in four decades. In the eyes of 22V Research founder Dennis DeBusschere, the Fed will ultimately need to be more hawkish should price pressures continue to build and growth remain robust in the face of rate hikes. "The mechanism through which the Fed is impacting the real economy is through the financial conditions channel," DeBusschere said on Bloomberg Television last week. "If the data doesn't slow, financial conditions will need to tighten more." Dan Suzuki, deputy chief investment officer at Richard Bernstein Advisors, has a different take. If anything, the current dynamic is likely not too far from the Fed's "best-case scenario," he said. They've been clear that they would like to hike rates to neutral and then assess policy from there. Well, we're still quite a far way from neutral so this gives them room to raise rates further without the fear that they're going to cause credit markets to freeze up... So the Fed has raised the underlying cost of credit without causing markets to freeze up. And the financial markets that have been hit hardest are arguably the most frothy areas with the greatest systemic risk.

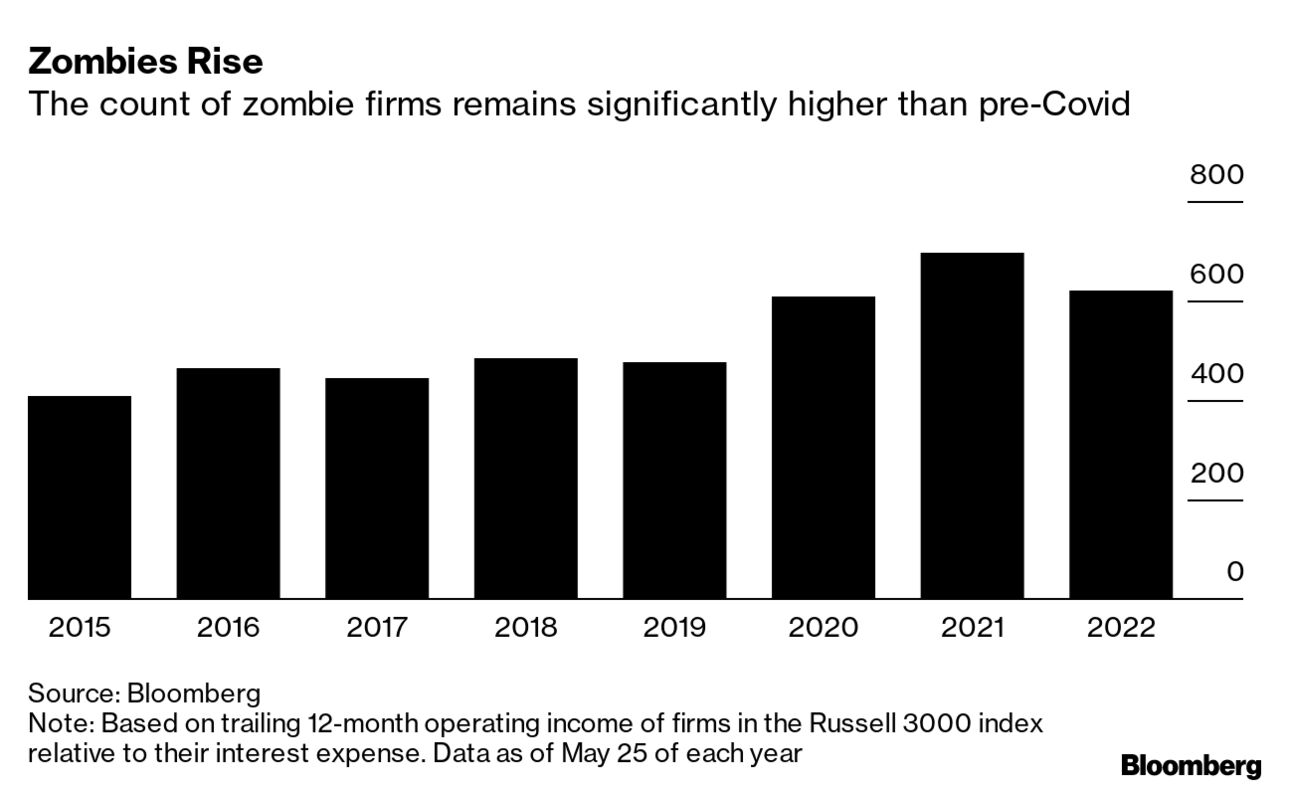

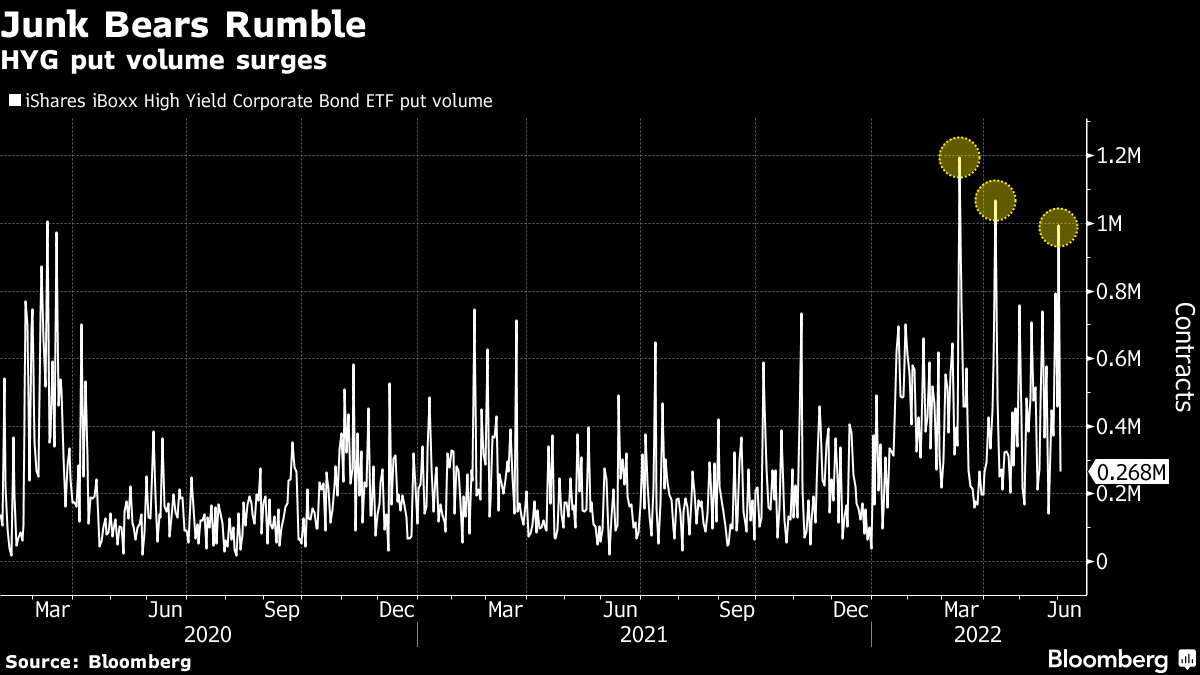

While borrowers have had to be more selective about when they tap the market, it's not anything close to an ice-out. While buyers demanded bigger concessions, a total of $14.3 billion in blue-chip bonds priced on Wednesday -- the most in more than two weeks, according to Bloomberg data. But even though the Fed's balance sheet runoff has only just officially begun and financial conditions are easing, the end of easy money is reshaping the corporate credit landscape. Corporate zombies -- companies that aren't earning enough to cover their interest expenses, let alone turn a profit -- have seen their ranks swell in recent years, as chronicled by Lisa Lee of Bloomberg News. Zombie firms now account for roughly a fifth of the country's 3,000 largest public companies, with some $900 billion of debt between them. That hasn't been much of a problem over the past few years, with primary markets wide-open. But with borrowing costs on the rise as inflation eats away at earnings, there's a sea change underway. Junk-rated companies have borrowed just $56 billion so far in 2022 -- a more than 75% decline from a year ago. "When interest rates are at or close to zero, it's very easy to get credit, and under those circumstances, the difference between a good company and a bad company is narrow," Komal Sri-Kumar, president of Sri-Kumar Global Strategies and former chief global strategist of TCW Group, told Bloomberg's Lee. "It's only when the tide runs out that you figure out who is swimming naked." One of the only ways to kill a zombie is through bankruptcy. But there's not necessarily a wave of defaults on the way. Zombie firms have raised hundreds of billions of dollars since the onset of the pandemic, building up cash buffers that could last months or years. And there have been zombies that have successfully come back to life. Take Exxon Mobil Corp.: surging oil prices and widening fuel margins drove a boom in profits, helping the energy giant pare down its debt to $48 billion from roughly $70 billion at the end of 2020. Even still, the tally of zombie companies is expected to stay near current levels or climb for some time. "The combination of interest-rate hikes and inflation will produce more zombies," said Noel Hebert, direct of credit research at Bloomberg Intelligence. "By year-end, we'll have more." Meanwhile, traders are reloading hedges on a move lower in the biggest US junk-bond exchange-traded fund. Nearly 994,000 put contracts on the $14.3 billion iShares iBoxx High Yield Corporate Bond ETF (ticker HYG) traded Wednesday, Bloomberg data show. That was the third-biggest daily volume since March 2020, and it followed the fund's best weekly rally since April 2020. The pile into HYG puts shows that traders are "slapping hedges back on" following last week's rally as pricing solidifies around a hawkish Fed, according to Charlie McElligott at Nomura Holdings. While markets last week had started to reflect the possibility the central bank could pause its rate-hiking campaign as soon as September, swaps show that traders are largely pricing in three back-to-back half-point hikes. Given that HYG's realized volatility is still relatively low, it's an inexpensive way to hedge the impact of tightening monetary policy on corporate credit, McElligott said. "There's still a sense of another shoe to drop -- the September pause is a total hoax," McElligott wrote in an email. "Hawkishness not only being reiterated here, but in Canada and Europe. Add in quantitative-tightening commencement and the perception of impact it can have on spread product like credit, it continues to be a preferred 'cheap' hedge." After surging nearly 5% last week, stoked by optimism that the Fed could lighten up on rate-hikes later this year, HYG is lower by roughly 1.2% this week. So far this year, HYG has dropped nearly 9% -- on track for the worst year since 2015. Once Drafted by the Boston Celtics, Now He's Leading a Quant Fund Firm Citi's Fat-Finger Trade Seen Costing Bank More Than $50 Million Winklevoss Twins Aren't Alone With 'Crypto-Winter' Job Cuts |

No comments:

Post a Comment