| Ever the optimist, I'm still hoping the US economy avoids a recession — or at least a deep one. It does seem like a long shot. But I'm not the only one being optimistic. Last week stocks were rallying. And the best part of the rally came when Treasury yields rose across the board on Friday. That's a combination that points to some economic optimism. You wouldn't see that if stocks were rallying in anticipation of a recession inducing a Fed rate pause. So the big question in financial markets now is whether this brief change of tack is just a bear market rally — a temporary upturn in shares in a longer-term decline — or the beginning of a new bull market. The data show that — contrary to the myth of equity markets being forward looking — we should expect another leg down in shares if we have a recession. When it comes to whether this is just a bear-market rally or not, the real economy has the answers. It was interesting to pinpoint when bear markets began and when recessions began to get a sense of how important a recession call is in terms of investment losses. Here's what I found: - In 2020, the S&P 500 peaked in February, the same month the recession began

- In 2007, the market peaked in October, two months before the recession started in December

- In 2001, the recession began in March. But equities had already peaked a year earlier in March of 2000

- In 1990, the recession began in July, the same month the S&P 500 peaked

- The S&P 500 peaked in November of 1980, whereas you had to wait until July of 1981 for the second peak in the economy's double dip recession

That's five recessions in the last 40-odd years. And it's a mixed bag on how forward-looking markets actually were. You can give the S&P 500 a pass on its ability to get the impact of the pandemic right. But in 2007 and 1990, stocks were right up near the top when the economy rolled over. Effectively, you had no early warning signal. I've looked at several other recessions and equity declines — like 1980 when the market peaked a month after the recession had already begun — and you get no sense that markets were able to foretell a recession was coming. The same was also true when looking at when market declines came to a halt. There was a short, sharp decline in 2020 that was stemmed by the massive stimulus to cushion the economic blow. But the two recessions before that saw declines for 15-30 months. More often than not, the market was falling throughout most of the economic downturn — and sometimes even afterward. That means that once a recession sets in, more losses are likely to follow. Many people say we're in a recession right now. There is no evidence of this yet but it's particularly important since the gross domestic product declined in the first quarter of 2022. A decline this quarter would mean two quarters of GDP contraction, the definition of a recession. But the shorthand that people use of two quarters of falling GDP to signal a recession isn't quite accurate. That's certainly the way it worked in the recession that began in 1990. But in the following recession, real GDP actually rose 2.5% as the recession began. You had this sort of sawtooth pattern to the GDP data around the recession — not a plunge and a rise from the depths. And while a two-quarter contraction did occur in the recession that began in 2007, the 2020 pandemic downturn will end up being too short to qualify. So what is a recession, really? The official arbiter in the US is the National Bureau of Economic Research. And they say that: The NBER's definition emphasizes that a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months.

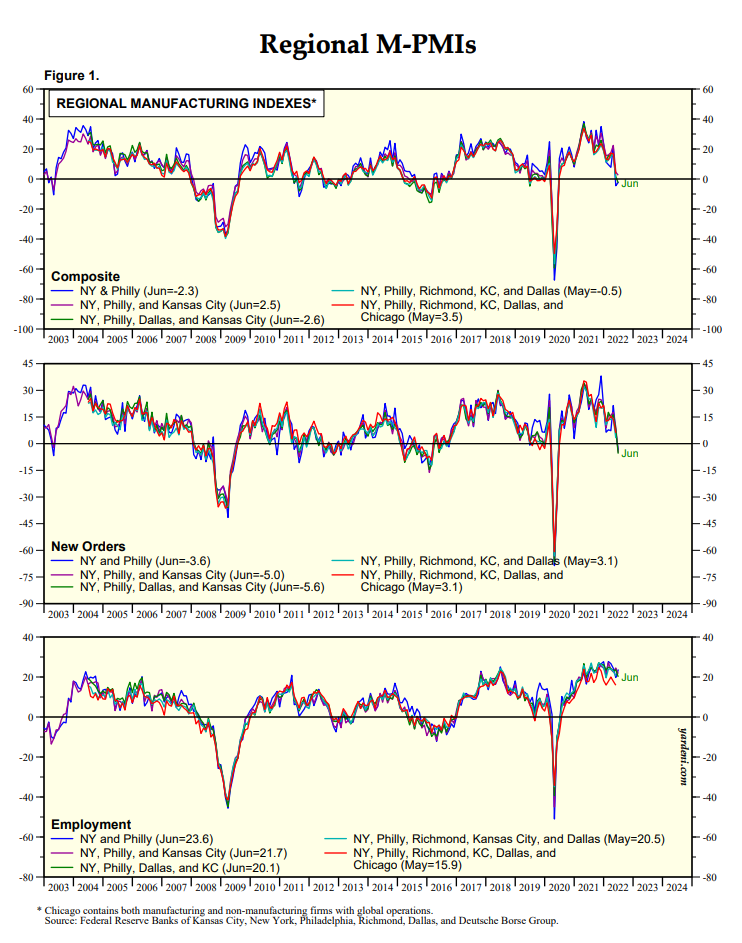

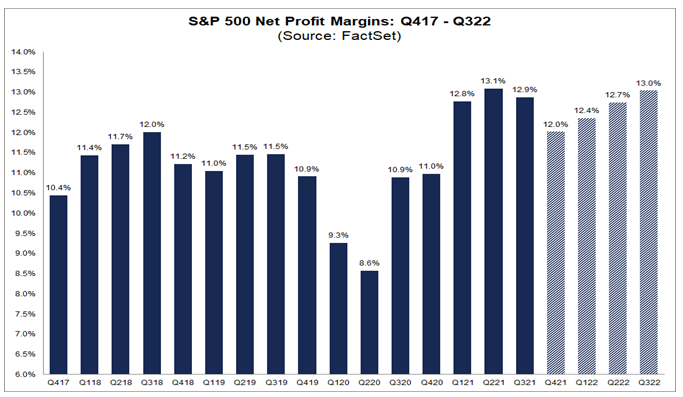

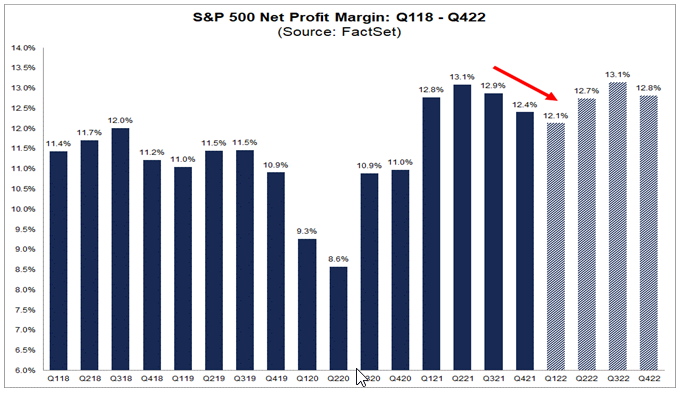

I would say that calling a recession is more an art, a qualified judgement, than an exact science like the two-quarter shorthand would imply. The NBER says it's all about "depth, diffusion, and duration". In effect, recessions are periods of economic weakness that are long enough, deep enough and broad enough to impact employment and spending, and therefore production and capital expenditure on an economy-wide basis. And usually that means equity markets having to recalibrate expectations lower as the level of economic distress sinks in — unlike during the pandemic when stimulus meant recalibrating higher. Some of this goes back to the risks outlined in my piece about margins declining. I would argue that the recent decline in stocks makes sense when understood as a reversion to the mean for margins. The Nirvana of permanently high margins was never sustainable. Inflation blew that myth off, taking stocks down a notch with it. But if rates rise enough to crash the economy, stocks will need to come down from here. So the question is how much higher interest rates do go, and how much the ratio of price to earnings compresses. Last week I mentioned jobless claims as a great real-time barometer which will tell us by November where the economy is heading. But there are also plenty of other recent data points showing the way too. The regional Fed indices are a good place to start as they offer a view into economic conditions in each of the 12 regional Fed areas. On that score, the data point to an expanding number of soft spots in the economy. In fact, the latest New York, Philly and Dallas Fed manufacturing numbers were all negative — meaning the manufacturing economy is contracting in those districts. The numbers are all pointing down, with employment still holding up, but also starting to crack too. The S&P Global Flash US Composite PMI — which tracks both services and manufacturing — reinforces that knife's edge growth aspect. It came out last week very close to the 50 threshold between expansion and contraction. Moreover, the services sector had the weakest reading in five months. And according to S&P, the manufacturing index "fell to a degree only exceeded twice in the 15-year history of the survey, at the height of the initial pandemic lockdowns in 2020 and the height of the global financial crisis in 2008." The result is that the Atlanta Fed's GDPNow model estimate for real GDP growth for the second quarter of 2022 is now a paltry 0.3%, up from zero on June 16. The U.S. economy is growing, but only just. |

No comments:

Post a Comment