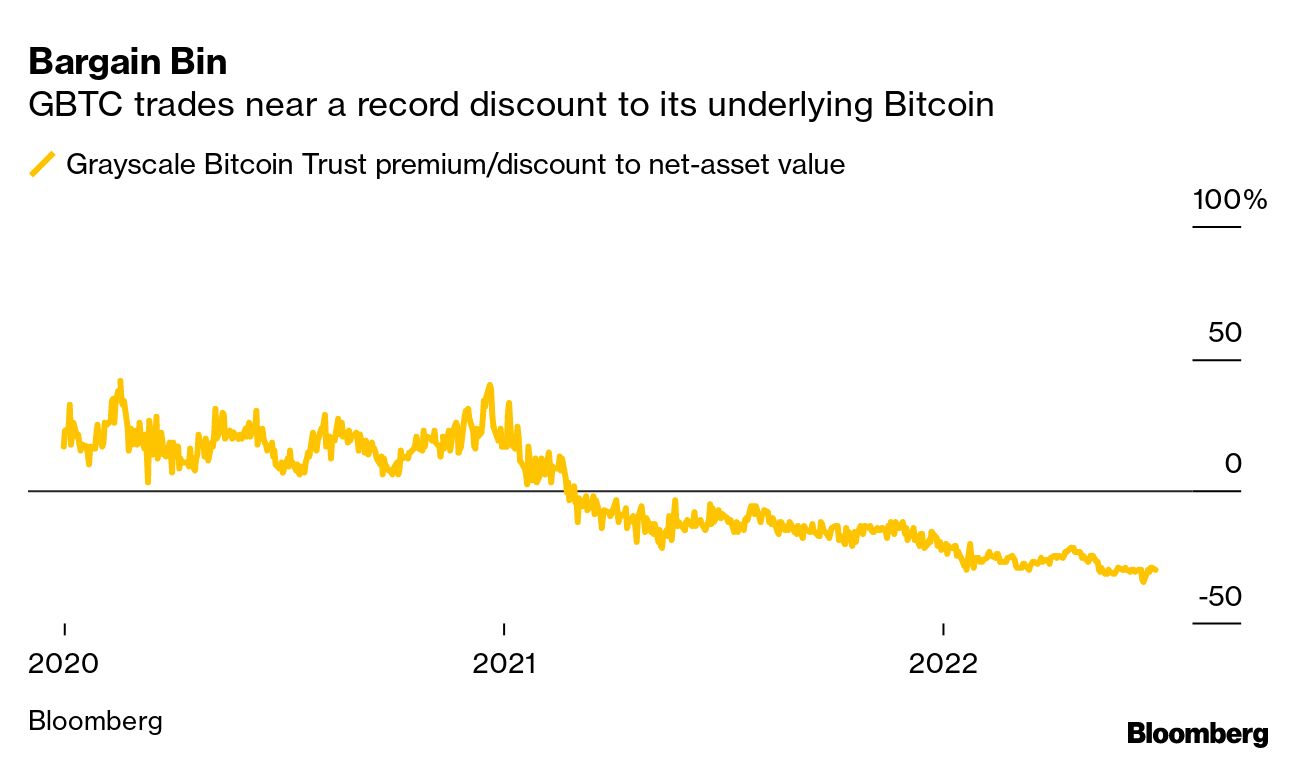

| The deadline for US regulators to rule on Grayscale Investments LLC's campaign to convert its Bitcoin trust into a spot ETF is just days away on July 6. No matter the outcome, Grayscale is going to lose. The first scenario is simple: the Securities and Exchange Commission flat out denies the application, citing the usual concerns of potential fraud and manipulation that it has trotted out in similar denials. This is what both the crypto contingent and the ETF industry expect will happen. The second scenario is a little more nuanced. In its current form, the Grayscale Bitcoin Trust (ticker GBTC) charges shareholders a 2% fee. While it has shed billions of dollars in market value over the past few months, it still has $13.3 billion in assets. That means Grayscale collects a tidy $233 million or so per year. A 2% fee would never fly in the ETF world, the land of low costs and never-ending fee wars. Take the ProShares Bitcoin Strategy ETF (BITO), which carries an expense ratio of 0.95%. That's relatively expensive for an ETF, and it's less than half of GBTC's fee. While GBTC would be the first physically-backed Bitcoin ETF to launch in the US, it's reasonable to think that other debuts would soon follow and the race to the bottom in costs would commence. So even if Grayscale's eight-month campaign to convert GBTC into an ETF is successful, that would mean saying goodbye to potentially hundreds of millions of dollars in revenue — a painful thing to do in the thick of crypto winter. Still, it's worth reflecting on why Grayscale has been so passionate and public about this bid. Unlike an ETF, the trust has no redemption mechanism, meaning that GBTC shares can't be created and destroyed as demand shifts. As a result, the fund's price is nearly 30% below the value of its underlying Bitcoin. That's a problem for Grayscale and for the entire industry. For most of its history, GBTC traded at an enormous premium to its net asset value. That created a popular arbitrage play among hedge funds such as now-disgraced Three Arrows Capital, which was one of the trust's biggest holders as of December 2020. It worked like this: An institutional investor would contribute Bitcoin in exchange for GBTC shares, which could then be sold at a markup after the lockup period expired. Of course, that arbitrage trade is long gone now. The play now is to buy heavily discounted GBTC in hopes that conversion in an ETF will vaporize the discount — but that's not looking like the best bet now either. |

No comments:

Post a Comment