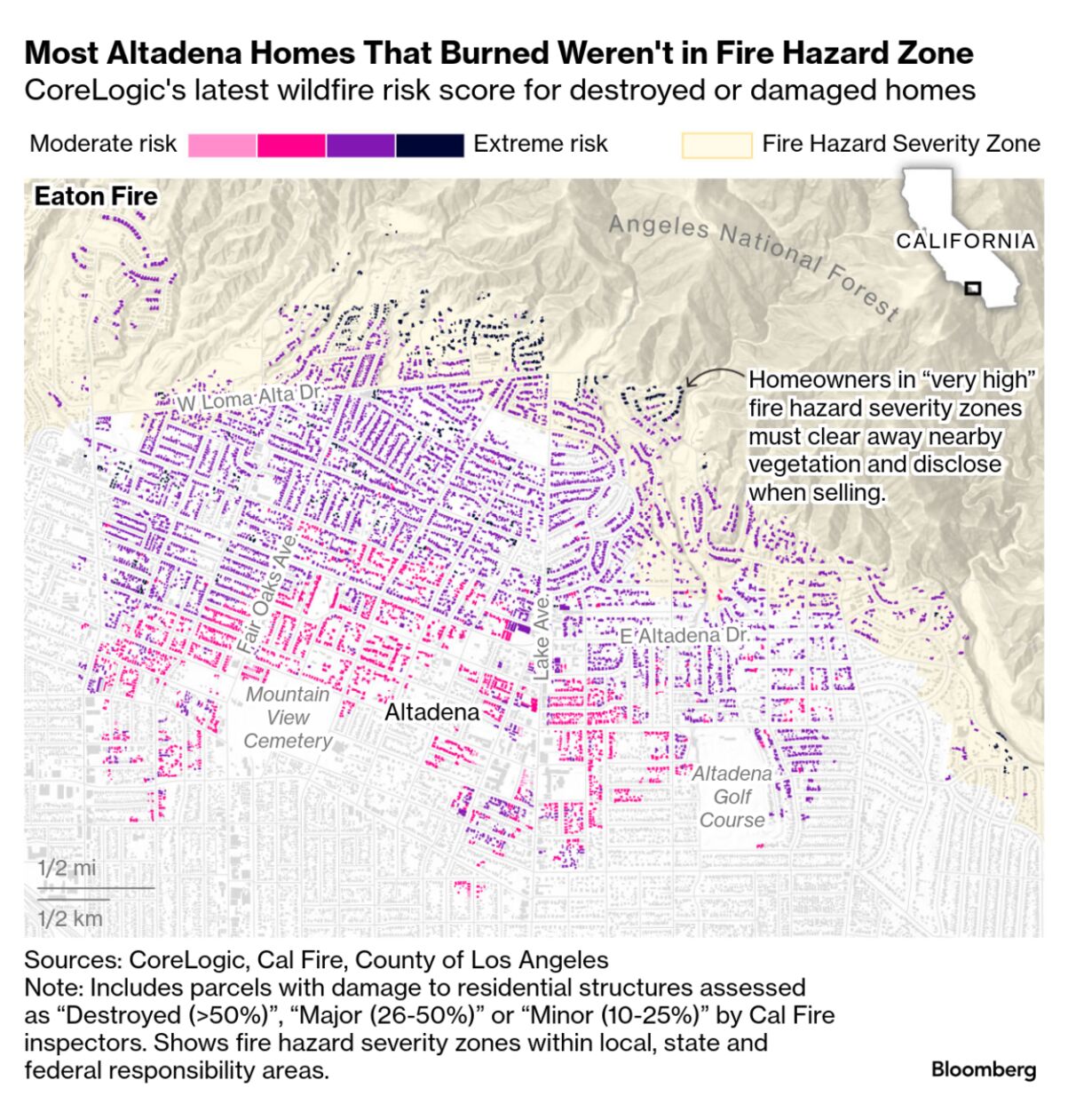

| By Leslie Kaufman, Andre Tartar, and Armand Emamdjomeh In the era of cutting-edge computer modeling, satellite data and AI, there has never been more abundant information on the danger that wildfire poses to homes in the Los Angeles area. But that didn't necessarily help thousands of homeowners correctly assess their personal risk. Many homes that burned in the Eaton Fire lay outside the boundaries of state- or local-designated "very high" fire hazard severity zones, Bloomberg Green found after analyzing inspection reports by the California Department of Forestry and Fire Protection, or Cal Fire, for more than 20,000 residential properties in areas affected by the recent wildfires.  Altadena's East Alta Loma Drive seen from above on Feb. 11, 2025. Photographer: Kyle Grillot/Bloomberg The fires last month destroyed more than 11,000 homes in total, and more than 40% of those had stood outside of the official fire-hazard zones. In Altadena, some 4,500 houses burned in locations beyond the zone boundaries. That means homeowners faced no fire-related disclosure requirements when purchasing a home, as would be the case for transactions inside the zones. Property owners inside the zone also face mandates for brush clearing and other steps to mitigate risk that didn't apply to nearby homes outside the boundary. Insurers had access to more finely tuned risk indicators, and knew how to interpret them. The neighborhoods that burned in LA "looked disproportionately high risk compared to the rest of the country, and insurers knew it," says Anand Srinivasan, head of research and development at CoreLogic Inc., a property information company. This gap points to a wider problem. As climate-driven perils such as wildfire and flooding become more frequent and more severe, many more Americans will try to assess their home's vulnerability. They'll face mixed signals and a disparity between what data is freely available and the fuller data that private companies can pay to access. The government fire hazard maps of LA are easily found online. Other, more precise information on fire risk in LA neighborhoods exists in the private sector. CoreLogic, which consults for government and insurers, among other clients, had rated the vast majority of homes in Altadena as having a "high" or "very high" risk of wildfire damage — even if they lay outside a hazard zone. But this data isn't available to the general public. It's sold business-to-business; CoreLogic made it available to Bloomberg for this story. There were other places homeowners worried about wildfire risk could find more information, if they were motivated. First Street Technology Inc. estimates climate risks at the property level and makes its risk scores available to the public for free. Its risk ratings appear in listings on the popular real estate sites Zillow and Redfin. About 95% of destroyed homes in Altadena had a fire risk level of at least 7 on a 10-point scale as assigned by First Street. Climate change made the LA fires significantly more likely to happen, scientists have concluded, and intensified last year's ferocious Hurricane Helene. Yet climate risk is also difficult to convey because it's lower in the very near term than over a lifetime, or the typical length of a mortgage. For example, what's often called the 100-year floodplain is not an area that floods roughly once a century, as is often assumed. It's an area where the risk of flooding is 1% a year, and over 30 years, that chance amounts to one in four. Complicating the picture further, current levels of climate risk aren't constant. They will rise as more greenhouse gases are pumped into the atmosphere. Risk modelers account for this in their projections. How much do homeowners know about their wildfire risk? Read the full story with models and risk scores for Southern California neighborhoods on Bloomberg.com. |

No comments:

Post a Comment